Introduction

Third-party vendors are now one of the most consequential risk vectors in financial services. According to Verizon's 2025 Data Breach Investigations Report, third-party involvement was present in 30% of breaches analyzed — double the rate from the prior year. For fintech firms, banks, and crypto companies, that number should be alarming.

The average cost of a data breach in the financial sector reached $6.08 million in 2024, according to IBM's Cost of a Data Breach Report. When that breach originates with a vendor — a KYC provider, payment processor, or cloud host — your organization bears that cost regardless of who was at fault.

As financial institutions grow more dependent on third-party providers for core infrastructure, every new vendor relationship introduces potential compliance and security exposure. Organizations that manage this exposure consistently well share one thing: a structured vendor risk management program.

This guide covers the six types of vendor risk, the core components of an effective program, a step-by-step framework for building one, and the best practices that matter most for fintech and financial services companies.

Key Takeaways

- Third-party vendors were involved in 30% of 2025 data breaches — making VRM a frontline risk issue, not a back-office exercise

- Regulated financial institutions remain legally accountable for vendor-caused compliance failures

- Effective VRM programs cover six risk types: cybersecurity, compliance, financial, operational, reputational, and geopolitical

- Vendor tiering based on risk directs the greatest scrutiny to your highest-stakes relationships

- Fractional compliance leadership gives early-stage fintechs director-level VRM oversight without a full-time hire

What Is Vendor Risk Management (and Why It's Non-Negotiable)

Vendor risk management (VRM) is the systematic process of identifying, assessing, and mitigating risks introduced by third-party vendors across the entire vendor lifecycle — from initial onboarding through offboarding. It spans cybersecurity, compliance, financial, and operational risk.

VRM is often used interchangeably with third-party risk management (TPRM), though TPRM is technically broader, covering all external relationships including contractors, affiliates, and sub-processors. In regulated financial services, the distinction matters less than the underlying obligation: both programs are subject to regulatory examination.

Why Accountability Doesn't Transfer With Outsourcing

When you outsource a function to a vendor, you retain the risk. That's the part most firms discover too late.

The Federal Reserve, FDIC, and OCC stated it plainly in their 2023 Interagency Guidance on Third-Party Relationships: a banking organization's use of third parties does not diminish its responsibility to operate safely and soundly and comply with applicable laws and regulations. The FCA takes the same position: firms cannot delegate regulatory responsibility to an outsourced provider.

For fintech companies with sponsor bank relationships, this has direct consequences. Sponsor banks are accountable for their fintech partners' vendor programs — meaning your VRM posture directly affects those partnerships.

Regulators across jurisdictions now treat vendor oversight as a supervisory expectation:

- OCC — examines third-party risk programs as part of safety and soundness reviews

- FCA — requires firms to demonstrate ongoing oversight of material outsourcing arrangements

- OSFI — mandates third-party risk management under its B-10 guideline for federally regulated institutions

- DORA — imposes binding ICT third-party risk requirements on EU financial entities effective January 2025

The Six Types of Vendor Risk You Need to Manage

Not all vendor risk looks the same, and critical vendors often carry several types simultaneously.

Cybersecurity and Compliance Risk

Cybersecurity and data privacy risk is the most acute category. Vendors with weak access controls or poor security posture become direct entry points into your systems.

The 2023 Infosys McCamish Systems ransomware incident illustrates this precisely — a breach at an IT service provider exposed personally identifiable information for over 57,000 Bank of America customers. The bank had no control over the incident, but bore the reputational and legal exposure.

Compliance and regulatory risk runs a close second. Vendors who fail to meet BSA/AML, GDPR, PCI DSS, or DORA obligations can trigger regulatory action against the contracting organization.

The Federal Reserve's 2024 consent order against Evolve Bank & Trust makes this concrete. The Fed cited deficiencies in Evolve's fintech partner risk management — and the bank, not its fintech partners, faced direct regulatory consequences.

The Remaining Four Risk Types

| Risk Type | What It Looks Like |

|---|---|

| Financial | Vendor insolvency disrupting critical service delivery. Synapse Financial Technologies filed for Chapter 11 in 2024, leaving a reported $60–90M shortfall and freezing customer funds across partner platforms. |

| Operational | Service degradation, poor quality control, or delivery failures affecting your operations |

| Reputational | A vendor's misconduct or public controversy attaching to your brand |

| Geopolitical | Cross-border vendors subject to sanctions, data residency laws, or political instability |

The Synapse collapse illustrated something broader: financial and operational risk don't arrive separately. When vendor financial health goes unmonitored, both can surface at once.

Core Components of an Effective Vendor Risk Management Program

Vendor Assessment and Due Diligence

Before granting any vendor access to systems or data, organizations must complete structured due diligence. This means reviewing:

- Security certifications (SOC 2 Type II, ISO/IEC 27001)

- Compliance status against applicable frameworks

- Financial health and solvency indicators

- Incident history and breach disclosure records

- References from comparable clients

Inadequate initial review is one of the most common causes of downstream regulatory and security failures. This step carries extra weight for vendors who will handle customer PII or access core financial systems.

Risk Categorization and Vendor Tiering

A flat approach to vendor oversight doesn't work. Tier your vendors based on data sensitivity and operational criticality:

- High tier: Payment processors, core banking integrations, cloud providers, KYC/AML platforms — maximum rigor, most frequent monitoring

- Medium tier: Supporting operational tools with moderate data access

- Low tier: Limited-access or low-impact relationships — lighter-touch oversight

This tiering model concentrates your team's effort where the consequences of failure are largest.

Contract Governance

Vendor contracts must go well beyond standard commercial terms. According to the 2023 Interagency Guidance, contracts supporting third-party relationships should address:

- Data protection obligations and permitted use

- Audit rights allowing verification of compliance at any time

- Incident notification timelines aligned with applicable regulations

- SLA requirements with compliance-linked performance measures

- Liability allocation in the event of a breach

- Defined offboarding and data return/deletion procedures

Weak contract governance is a frequent finding in regulatory examinations. Missing audit rights and breach notification clauses are the two gaps examiners flag most often.

Continuous Monitoring

Vendor risk doesn't freeze after onboarding. A vendor's security posture, financial stability, or compliance status can shift materially. Effective monitoring programs include:

- Periodic formal reassessments scaled to the vendor's risk tier

- Real-time breach alerting and adverse media monitoring

- Compliance review triggers tied to regulatory changes

- Automated risk scoring updates via compliance monitoring tools

Fraxtional's compliance engagements treat vendor oversight as an ongoing operational function, integrated alongside AML monitoring and sanctions screening rather than scheduled as a standalone annual review.

Incident Response Planning

When a vendor experiences a breach or compliance failure, your organization needs a documented response framework. This should specify:

- Escalation paths and defined roles

- Evidence preservation and investigation procedures

- Regulatory notification obligations and timelines

- Communication procedures for sponsor banks, customers, and regulators

A response plan without regulatory notification timelines is incomplete. The OCC's Spring 2024 Semiannual Risk Perspective explicitly expects financial institutions to map third-party interdependencies, include critical vendors in business continuity testing, and set clear remediation certification expectations.

How to Build a Vendor Risk Management Strategy: A Step-by-Step Framework

Step 1 — Inventory and Classify Your Vendor Ecosystem

You cannot manage what you haven't mapped. Start with a complete, maintained vendor register that captures:

- Every active vendor relationship

- Type of data or system access each vendor holds

- Criticality to core operations

- Regulatory relevance of the relationship

Without this foundation, risk prioritization is guesswork — and examiners are trained to find exactly those gaps.

Step 2 — Define Your Risk Appetite and Assessment Criteria

Establish formal thresholds before the next vendor conversation happens. This means deciding:

- What level of vendor-introduced risk is acceptable

- What risk findings require remediation before approval

- What vendor categories are ineligible regardless of commercial value

Documented risk appetite standards prevent reactive vendor approvals driven by business urgency rather than risk judgment.

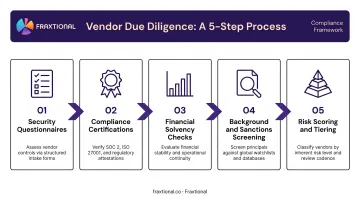

Step 3 — Build a Structured Onboarding and Due Diligence Process

Every new vendor relationship should go through the same documented workflow before access to systems or data is granted:

- Distribute security questionnaires — assess controls, access management, and incident history

- Review compliance certifications — confirm SOC 2, ISO 27001, or relevant framework status

- Run financial solvency checks — review financials or public indicators for stability

- Conduct background screening — regulatory history, sanctions screening, references

- Assign a risk score and tier — determine oversight level before contract execution

Inconsistency here is a real liability. Regulators treat selective due diligence as a program gap, not a judgment call.

Step 4 — Embed Security and Compliance Requirements in Contracts

Contracts should operationalize the risk findings from due diligence. At minimum, include:

- Specific security controls required of the vendor

- Evidence of certifications on a recurring basis

- Breach notification timelines consistent with applicable law:

- UK GDPR (ICO): notification required within 72 hours

- NY DFS (23 NYCRR Part 500): same 72-hour window applies

- Audit rights that allow examination at any time

- Data handling obligations and offboarding procedures

Missing contractual requirements surface at the worst possible moment — during a breach response or regulatory exam, when there's no time to negotiate.

Step 5 — Establish Governance, Accountability, and Ongoing Review Cadences

VRM doesn't belong to one team. It requires defined ownership across procurement, legal, IT/security, and compliance — with a clear escalation path to senior leadership.

- Assign a named owner for each vendor relationship

- Set periodic formal reassessments based on risk tier (quarterly for high-tier, annually for low-tier)

- Review the overall VRM program annually, or whenever material regulatory changes occur

- Ensure the compliance or risk function has visibility and sign-off authority on new vendor approvals

For fintechs without a full-time CCO or CRO, this governance structure is exactly what fractional compliance leadership can provide, delivering director-level ownership of the program without a permanent hire.

Vendor Risk Management Best Practices for Fintech and Financial Services

Align VRM with Regulatory Requirements

The regulatory landscape for vendor oversight has clarified considerably in recent years:

- US: OCC Bulletin 2013-29 was rescinded in 2023. The current standard is the joint Interagency Guidance on Third-Party Relationships from the Fed, FDIC, and OCC — requiring risk-based programs across the full vendor lifecycle

- UK: FCA PS21/3 requires firms to map third-party dependencies as part of operational resilience, with full implementation expected by March 31, 2025

- EU: DORA has applied since January 17, 2025, requiring financial entities to manage ICT third-party risk within their formal risk frameworks and maintain a register of all ICT third-party arrangements

- Canada: OSFI Guideline B-10 (updated April 2023) sets enhanced expectations for federally regulated institutions managing third-party risk

A documented, risk-based vendor program isn't just good practice in these jurisdictions — it's a condition for maintaining operating licenses, passing examinations, and sustaining sponsor bank relationships.

Prioritize Fourth-Party Risk Visibility

Your critical vendors have their own vendors. Core banking platforms, cloud providers, and payment rails rely on sub-processor chains that can introduce concentration risk your due diligence never touched.

Practical steps:

- Contractually require critical vendors to disclose significant subcontractors

- Monitor for vendor ecosystem concentration risk (for example, multiple critical vendors relying on the same cloud infrastructure)

- Review the UK's PS16/24 framework for context on how regulators now approach critical third-party designation

Use Automation and Technology to Scale Monitoring

Manual, spreadsheet-based VRM reaches its limits quickly. Deloitte's 2023 global TPRM survey found that only about half of organizations formally segmented third parties by risk — and 32% didn't segment at all.

Purpose-built VRM tools or GRC platforms can handle questionnaire distribution, risk score updates, compliance tracking, and breach alerting automatically, freeing compliance teams for higher-judgment work. Fraxtional helps early-stage fintech clients evaluate and implement the right tools for their vendor volume and risk profile as part of its broader AML and compliance advisory engagements.

Leverage Fractional Compliance Leadership to Oversee VRM

For seed, Series A, and Series B fintechs, funding a full-time CRO or CCO to own the VRM function often isn't feasible. Fractional compliance leadership fills that gap directly.

Fraxtional's Fractional Advisory model provides a dedicated Director who holds the CCO, CRO, or BSA Officer title and takes accountable ownership of compliance programs, including vendor oversight, policy development, and regulatory representation. A growing fintech gets director-level VRM governance without the cost or timeline of a full-time executive search.

For discrete VRM projects such as a vendor program build, policy development, or independent audit, Fraxtional's On Demand Advisory model delivers the same director-level expertise on a project basis.

Treat Offboarding as a Risk Control

Vendor offboarding is one of the most commonly skipped elements of VRM. When a relationship ends, confirm:

- Formal revocation of all system and data access

- Certified deletion or secure transfer of shared data

- Settlement of outstanding compliance documentation

- A final risk review confirming no residual exposure

Former vendors with lingering access or data retention are latent security and compliance liabilities. Offboarding should be documented, tracked, and signed off by the same compliance function that approved the original onboarding.

Frequently Asked Questions

What does vendor risk management do?

VRM identifies, assesses, and mitigates the financial, cybersecurity, compliance, and operational risks introduced by third-party vendors. Its core function is ensuring organizations maintain control over their risk exposure even as they outsource critical processes to external providers.

What do risk management consultants do?

Risk management consultants (including fractional compliance leaders) help organizations design, implement, and oversee risk management programs. They bring specialized expertise in regulatory requirements, risk assessment methodology, and governance structures that many companies, particularly early-stage fintechs, haven't yet built internally.

What are the most common types of vendor risk?

The six key categories are cybersecurity/data privacy, compliance/regulatory, financial, operational, reputational, and geopolitical. Critical vendors in financial services — payment processors, core banking platforms, cloud providers — routinely carry multiple risk types at once.

What is the difference between VRM and TPRM?

The terms are often used interchangeably. TPRM is the broader discipline covering all external relationships — contractors, partners, affiliates, sub-processors. VRM is sometimes used specifically for supplier and service-provider relationships. In regulated financial services, both describe programs that are subject to direct regulatory examination.

How do you assess vendor risk in fintech and financial services?

Vendor risk assessment typically involves security questionnaires, compliance certification reviews, financial solvency checks, regulatory screening, and risk tiering based on data access and business criticality. Assessment depth scales with the vendor's tier — high-tier vendors face the most rigorous review.

What are the biggest challenges in building a vendor risk management program?

The most common obstacles are: incomplete vendor inventory, inconsistent contract governance, resource constraints at early-stage companies, vendor risk profiles that change post-onboarding, and difficulty keeping pace with evolving regulatory requirements.