Introduction

When a fintech platform processes payroll or an embedded finance provider manages client funds, the client's auditors need documented evidence that those external processes are actually controlled. That's the problem SOC 1 compliance solves.

Despite appearing regularly in enterprise procurement and bank partnership conversations, SOC 1 remains one of the most misunderstood compliance frameworks.

Many service organizations have been asked for a SOC 1 report without being clear on what it actually requires — or what they stand to gain beyond checking a box.

This article breaks down SOC 1 compliance in practical terms: the requirements, who genuinely needs it, and the business case for pursuing it — particularly for fintech companies, embedded finance providers, and SaaS platforms in regulated sectors.

Key Takeaways

- SOC 1 is an independently audited attestation that your internal controls protect the integrity of your clients' financial reporting.

- Applies to any organization whose services touch clients' financial statements — payment processors, fintech platforms, loan servicers, and payroll providers.

- Type 1 reviews control design at a point in time; Type 2 tests operating effectiveness over 6–12 months and carries far more weight with enterprise clients.

- SOC 1 isn't legally required, but enterprise clients and financial institutions routinely make it a condition of doing business.

- The primary payoffs: unlocking enterprise deals, reducing audit burden on clients, and demonstrating the control discipline investors expect.

What Is SOC 1 Compliance?

SOC 1 is defined by the AICPA as an examination of controls at a service organization that are likely to be relevant to user entities' internal control over financial reporting (ICFR). The standard governing these audits is SSAE No. 18. The report itself is issued by a CPA following an independent examination — not a self-certification or internal review.

Who Does SOC 1 Apply To?

SOC 1 is relevant to any organization whose services touch clients' financial data in a way that could affect the accuracy of their financial statements. Common examples:

- Payment processors and money transmitters

- Payroll platforms and HR technology providers

- Loan servicing and origination systems

- Embedded finance and Banking-as-a-Service (BaaS) providers

- SaaS platforms with access to client financial records

- Data centers hosting financial applications

If an error, breach, or control failure in your system could cause a material misstatement in a client's financial statement, SOC 1 applies to you.

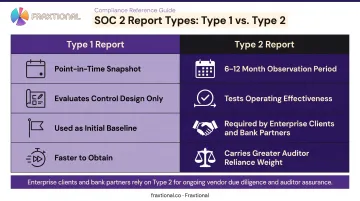

Type 1 vs. Type 2: Why It Matters

SOC 1 reports come in two forms, and the difference is significant in practice:

| Report Type | What It Covers | When to Use It |

|---|---|---|

| Type 1 | Whether controls are suitably designed at a specific date | Initial baseline; first-time SOC 1 |

| Type 2 | Whether controls operated effectively over 6–12 months | Enterprise clients, bank partners, ongoing assurance |

A Type 1 report demonstrates intent. A Type 2 report demonstrates proof. According to PCAOB AS 2601, to reduce control risk below the maximum, user auditors need evidence of operating effectiveness — which only a Type 2 report provides. For most enterprise relationships, Type 2 is the standard that actually matters.

Beyond the audit itself, a SOC 1 report lets enterprise clients and bank partners rely on your controls directly — skipping their own audit procedures against you. For FinTechs navigating sponsor bank due diligence or enterprise sales cycles, that distinction can accelerate a deal or remove a blocker entirely.

Key Benefits of SOC 1 Compliance

The benefits of SOC 1 compound when it's maintained consistently rather than pursued reactively when a client first asks for it.

Client Trust and Enterprise Deal Enablement

A SOC 1 report acts as pre-validated assurance for enterprise clients, bank partners, and their auditors. Instead of bespoke vendor review procedures (questionnaires, site visits, security interviews), procurement teams receive a standardized, third-party-validated document they already know how to evaluate.

In financial services, counterparties carry fiduciary obligations around third-party risk. The 2024 Federal Reserve, FDIC, and OCC community bank guide specifically identifies SOC reports, alongside independent assessments and industry certifications, as tools banks use to assess a third party's operational risk management and internal controls.

For service organizations without a SOC 1 report, the practical consequence is deal friction. Procurement teams stall, compliance reviewers escalate, and deals that should close in weeks drag on for months — or get screened out entirely. This risk is highest for:

- Fintech companies pursuing sponsor bank approval

- Series A/B companies selling into regulated financial institutions

- Embedded finance providers requiring bank partnership agreements

Risk Mitigation and Operational Protection

SOC 1 compliance forces organizations to formalize controls around the riskiest points in their financial data handling. The audit process examines whether controls are actually operating, not just written down.

KPMG's 2024 controls assurance benchmarking report identifies where failures concentrate: System Access controls accounted for 17% of exceptions, Authorization controls 15%, and manual controls represented 89% of operating-effectiveness exceptions versus just 11% for automated controls.

Organizations going through their first SOC 1 audit frequently surface problems they didn't know they had:

- Access rights that weren't properly scoped or revoked

- Transaction authorization workflows that existed informally rather than by policy

- Segregation of duties gaps that created single points of failure

- Reconciliation processes that depended on one person's judgment

Catching these gaps before an auditor does is the difference between a clean report and a qualified opinion.

Operational Improvement and Scalable Infrastructure

The discipline of scoping, designing, and documenting controls for SOC 1 replaces informal practices with repeatable processes. This matters less when a company has 15 people and far more when it has 150, when undocumented processes become expensive to untangle.

Type 2 reports reinforce this discipline: controls are tested over a sustained period, so organizations must maintain them, not just design them once. That shifts compliance from a one-time sprint to an ongoing practice that scales with headcount, transaction volume, and client complexity.

Key metrics that typically improve after consistent SOC 1 programs are in place:

- Reduced audit preparation time in subsequent years

- Fewer control exceptions and operational errors

- Faster enterprise client onboarding (standardized documentation replaces ad hoc vendor reviews)

SOC 1 Compliance Requirements: What Controls Are Needed

Unlike SOC 2, SOC 1 doesn't have a universal fixed set of criteria. Control objectives are customized to the services provided, and organizations work with a CPA auditor to define which control areas are relevant to their ICFR risk. That said, most SOC 1 reports address a consistent set of control categories drawn from PCAOB AS 2601.

Control Environment

The foundation. Organizations must establish clear policies, defined accountability structures, and management's demonstrated commitment to internal control, including formal segregation of duties and documented role assignments. Every other control category depends on this layer being solid.

Risk Assessment Process

Organizations must implement formal, documented processes for identifying financial reporting risks: unauthorized access, system failures, and processing errors among them. Risk assessments must be repeated following material organizational changes — they're not a one-time exercise.

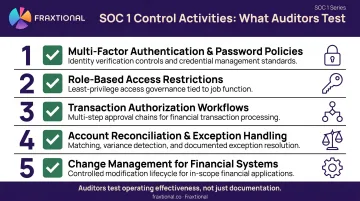

Control Activities

The practical protective measures auditors will actually test. These include:

- Multi-factor authentication and password policies for financial systems

- Access restrictions scoped to role and business need

- Transaction authorization workflows with documented approval chains

- Account reconciliation procedures and exception handling

- Change management processes for financial systems

Auditors test whether these controls are actually operating — documented controls that aren't functioning in practice will still produce findings.

Information, Communication, and Monitoring

SOC 1 requires evidence that financial data is accurately collected, reliably processed, and communicated appropriately within the organization. Exception reports and internal review logs are key evidence here.

Organizations must also maintain ongoing monitoring of control effectiveness, with documented remediation when deficiencies are identified. A gap without a documented response is a finding waiting to happen.

Documentation Requirements

Auditors require complete, organized evidence — not just policy documents. Specifically:

- Written policies and procedures

- Control execution logs and evidence

- Risk assessment records

- Data flow diagrams

- Organizational charts with role definitions

Inadequate documentation is one of the most common reasons organizations receive qualified opinions. KPMG's 2024 benchmarking found approximately 20% of reports across sectors were qualified, with qualifications typically stemming from General IT Controls — particularly logical access and change management. Organizations that address documentation gaps before fieldwork begins consistently avoid the most preventable qualification triggers.

What Happens When SOC 1 Compliance Is Ignored

Commercial risk surfaces first. Banks and regulated financial institutions use SOC reports as a standard component of third-party risk evaluation. Service organizations that can't produce one force counterparties to either skip that step — which fiduciary obligations often prohibit — or conduct direct audit procedures themselves, a far more invasive alternative.

Operational exposure builds quietly. Without the control structure SOC 1 requires, organizations accumulate undocumented processes, inconsistent access controls, and unresolved exceptions. At small scale, this is manageable. At scale, these gaps surface during client audits, regulatory examinations, or breach incidents — at the worst possible moment.

Reactive compliance costs more. Organizations that pursue SOC 1 only after a client mandates it — under a tight deadline — face higher remediation costs, internal disruption, and a real risk of receiving a qualified report on the first attempt. Building controls proactively is almost always cheaper than emergency remediation before a deal closes.

How to Approach SOC 1 Compliance Successfully

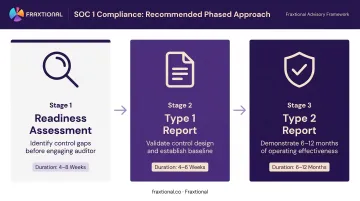

SOC 1 works best as a phased program rather than a single event. Most organizations benefit from this sequence:

- Readiness assessment — Identify control gaps before engaging a CPA auditor. Surprises during the audit are expensive.

- Type 1 report — Establish a documented baseline and validate control design.

- Type 2 report — Demonstrate operating effectiveness over a 6–12 month period. This is what enterprise clients and bank partners actually rely on.

The most common failure point isn't designing the wrong controls — it's failing to maintain them consistently and collect evidence throughout the year. Organizations that treat SOC 1 as a once-a-year scramble see more exceptions, higher remediation costs, and less credibility with clients.

For fintech startups, embedded finance companies, and Series A/B businesses without an in-house compliance function, working with experienced compliance leadership closes the gap between knowing controls are needed and knowing how to scope, build, and sustain them. Fraxtional's fractional compliance model — including CCO, CRO, and BSA Officer engagements — provides that structure without the overhead of a full-time executive hire.

For companies preparing for a SOC 1 audit while also managing AML obligations, sponsor bank reviews, or investor due diligence, having a named compliance leader who owns the process means fewer exceptions, faster audit cycles, and a cleaner report for the clients who are asking to see it.

Frequently Asked Questions

What is a SOC 1 report?

A SOC 1 report is an independently audited attestation document issued by a CPA that evaluates whether a service organization's internal controls adequately protect its clients' financial reporting integrity. It covers both business process controls and IT general controls relevant to financial data handling.

Who needs a SOC 1 report?

Any organization whose services can affect clients' financial statements typically needs one — including payroll processors, payment processors, fintech platforms, loan servicers, embedded finance providers, and SaaS companies with access to client financial data.

What are SOC Type 1, Type 2, and SOC 3 reports?

SOC 1 Type 1 reviews whether controls are suitably designed at a specific point in time. SOC 1 Type 2 tests whether those controls actually operated effectively over a 6–12 month period. SOC 3 is a separate, public-facing report tied to SOC 2's trust service criteria (security, availability, privacy, etc.) — not a variant of SOC 1.

What is the difference between SOC 1 and SOC 2?

SOC 1 focuses on controls relevant to clients' financial reporting integrity (ICFR). SOC 2 focuses on information security controls protecting customer data across five trust service categories: security, availability, processing integrity, confidentiality, and privacy. Organizations that handle both financial data and sensitive customer information often require both reports.

Are SOC 1 reports mandatory?

SOC 1 is not a legal requirement in most jurisdictions, but it is commonly required by enterprise clients, financial institutions, and investors as a condition of doing business.

How long does it take to achieve SOC 1 compliance?

A Type 1 report typically takes 2–4 months for an organization that has completed readiness preparation. A Type 2 report adds a 6–12 month observation period; organizations with significant control gaps should budget extra time for infrastructure work before an auditor can begin.