This guide is written for fintech founders, payment companies, crypto businesses, and compliance teams preparing to enter or currently operating in Connecticut. We'll cover licensing requirements, the application process, ongoing obligations, and critical 2024-2025 regulatory updates that expanded the law to explicitly cover virtual currency kiosks and digital wallet providers.

Key Takeaways

- A Connecticut Money Transmitter License is mandatory for businesses receiving, transmitting, or issuing payment instruments or stored value in the state

- Applications go through NMLS and require surety bonds ($300K–$1M), net worth of $500K–$1M, background checks, and a business plan

- Virtual currency kiosk operators became subject to licensure October 1, 2024, and digital wallet providers face expanded requirements as of October 1, 2025

- Once licensed, expect annual renewal by December 31, BSA/AML program maintenance, five-year recordkeeping, and one-business-day event reporting

What Is the Connecticut Money Transmitter License and Who Needs It?

The Connecticut Money Transmitter License is the state authorization required to engage in the business of money transmission under Conn. Gen. Stat. § 36a-597. If your business handles payments, stored value, or virtual currency in any form, Connecticut likely considers you a money transmitter. Covered activities include:

- Issuing or selling payment instruments

- Receiving or transmitting money or monetary value

- Selling stored value

- Operating virtual currency kiosks

- Providing digital wallet services

You Don't Need a Connecticut Office to Need a License

Connecticut's jurisdictional reach extends far beyond physical presence. Under Conn. Gen. Stat. § 36a-597(a), you're "acting in this state" if you:

- Have a place of business located in Connecticut

- Receive money or monetary value from a person located in Connecticut

- Transmit money to or from Connecticut

- Issue stored value sold in Connecticut

- Sell stored value in Connecticut

- Own, operate, solicit, market, advertise, or facilitate virtual currency kiosks physically located in Connecticut

For example, a San Francisco-based fintech with zero Connecticut employees still needs a license if Connecticut residents use its services.

State License vs. Federal FinCEN Registration

Both are required, but they serve different purposes.

The Connecticut license is a consumer protection instrument. It:

- Governs consumer protection standards

- Sets bonding and net worth requirements

- Establishes operational oversight at the state level

- Requires annual renewal and reporting

Federal FinCEN MSB Registration operates separately, covering AML/BSA obligations at the national level. It is required for all money services businesses, and applicants must enter their FinCEN Registration Confirmation Number into NMLS during the Connecticut application. Holding federal registration does not exempt you from state licensure — both are required and enforced independently.

Connecticut Money Transmitter License Requirements

Connecticut imposes tiered financial requirements based on business activity type and transaction volume.

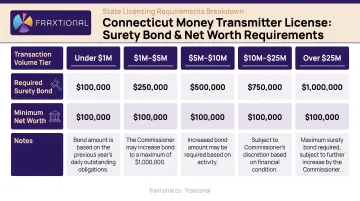

Surety Bond Requirements

Connecticut requires an Electronic Surety Bond (ESB) filed through NMLS. Bond amounts scale with activity:

| Average Weekly CT Transmissions | Minimum Bond Amount |

|---|---|

| Under $300,000 | $300,000 |

| $300,000 to $500,000 | $500,000 |

| $500,000 or more | $1,000,000 |

| Virtual currency transmission | $1,000,000 (as determined by Commissioner) |

Virtual currency operators face the highest baseline bond requirement at $1,000,000. The bond must be issued by a surety company authorized to conduct business in Connecticut.

Tangible Net Worth Requirements

Net worth requirements vary by activity type:

| Activity Type | Minimum Net Worth |

|---|---|

| General money transmission | $500,000 |

| Checks, drafts, or money orders | $100,000 |

| Traveler's checks or electronic payment instruments | $1,000,000 |

| Stored value | $1,000,000 (or higher per Commissioner) |

| Virtual currency activities | $1,000,000 |

Audited financial statements (GAAP-compliant) must document net worth. This isn't a one-time threshold — you must maintain it continuously while licensed.

Permissible Investments (Ongoing Capital Requirement)

Licensees must maintain permissible investments with a value at least equal to the aggregate amount of outstanding money transmissions in Connecticut. This is an ongoing capital adequacy standard that changes as your transaction volume fluctuates.

Qualifying permissible investments include:

- Cash in US currency and cash equivalents (ACH items in transit, AAA-rated money market funds)

- Time deposits or debt instruments of a bank

- Prime quality commercial paper and eligible bills of exchange

- Interest-bearing obligations issued or guaranteed by the US or any state

- Receivables due from authorized delegates (not past due)

- Gold

You must maintain a list of permissible investments and update it as part of annual renewal filings.

These financial requirements cover capital adequacy — but Connecticut also scrutinizes the people behind the business.

Background Check and Control Person Requirements

All owners, directors, executive officers, and qualifying individuals must:

- Submit Individual Forms (MU2) through NMLS

- Provide fingerprints for FBI criminal background checks

- Consent to credit reports and financial background investigations

- Disclose personal history including prior financial crimes, bankruptcies, or regulatory actions

Prior financial crimes or regulatory actions can result in outright application denial — criminal history checks are mandatory, not discretionary.

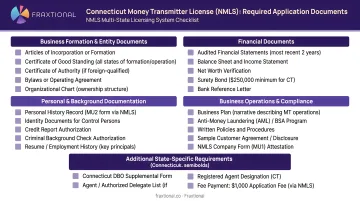

Required Application Documentation

The NMLS Phase 2 Checklist for Connecticut requires:

- Certificate of formation or incorporation

- Business plan describing money transmission activities in detail

- Written AML/BSA compliance program

- Sample authorized delegate contract template

- Audited financial statements (GAAP-compliant)

- List of permissible investments

- Details of pending litigation or regulatory actions

- Virtual currency disclosure questions (if applicable)

Incomplete documentation is the most common cause of application delays. Gather all documents before beginning the NMLS filing process.

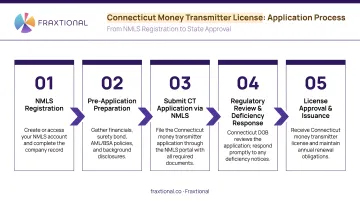

How to Apply for a Connecticut Money Transmitter License

All Connecticut money transmitter license applications are submitted through the Nationwide Multistate Licensing System (NMLS). The process follows five distinct stages.

Step 1: Register on NMLS and Complete Company Record

Create an NMLS company account and complete the Company Form (MU1). This includes:

- Uploading organizational documents (articles of incorporation, operating agreements)

- Documenting ownership structure and organizational chart

- Adding all control persons with Individual Forms (MU2)

- Entering your FinCEN MSB Registration Confirmation Number

Each control person must create their own NMLS account and authorize the company to access their information.

Step 2: Prepare and Attach Required Documents

Document preparation is time-intensive — plan 4-8 weeks to gather everything.

Key documents to prepare:

- Audited financial statements (last fiscal year)

- AML/BSA compliance program documentation with named BSA Officer

- Detailed business plan covering customer types, transaction flows, revenue model, and risk mitigation

- Sample authorized delegate contract (if using agents)

- Surety bond from an approved carrier

Early-stage fintechs without in-house compliance staff often engage a fractional BSA Officer or CCO — Fraxtional places experienced compliance leaders in exactly this role — to meet the documentation standards banks and examiners require.

Step 3: Pay the Application Fee and Submit

Connecticut application fees are nonrefundable:

| Fee Type | Amount |

|---|---|

| CT License Application Fee | $1,875 |

| NMLS Company (MU1) Setup Fee | $120 |

| NMLS Individual (MU2) Setup Fee | $35 per person |

| NMLS Branch (MU3) Setup Fee | $25 per location |

| Criminal Background Check | $36.25 per person |

Note: Credit card payments through NMLS incur an additional 2.5% service fee. Budget accordingly — a typical application with three control persons costs approximately $2,100 plus payment processing fees.

Step 4: Respond to Deficiency Notices

The Connecticut Department of Banking will review your application and typically issues deficiency notices requesting additional information or clarification. Nearly all applications receive at least one — treat it as a standard part of the process, not a setback.

Respond completely and promptly. Delayed or incomplete responses directly extend your total wait time. The Department does not provide formal processing timeframes, so any delay on your end adds directly to your total wait time.

Step 5: Receive Approval and Maintain License

Once approved, your license will be issued through NMLS. Post-approval requirements include:

- Display license information as required by Connecticut law

- Notify the Department of Banking of material changes within one business day (new control persons, changes in business activities, criminal charges)

- Track annual renewal deadlines (December 31)

- Maintain ongoing compliance with net worth, bond, and permissible investment requirements

Approval is the starting line, not the finish. Ongoing obligations — reporting changes, maintaining permissible investments, renewing annually — activate the day your license issues.

Ongoing Compliance Obligations After Licensing

Licensing approval doesn't end your regulatory obligations — it starts them. Connecticut's ongoing requirements cover renewals, AML programs, delegate oversight, and event reporting, each with hard deadlines and real penalties for gaps.

Annual Renewal Requirement

Connecticut money transmitter licenses must be renewed annually through NMLS between November 1 and December 31. The current renewal fee is $1,125.

Renewal requires:

- Updated audited financial statements (within 90 days of fiscal year end)

- Confirmation of continued surety bond coverage

- Updated list of permissible investments

- Updated MU2 forms for any new control persons

- Payment of renewal fee

Critical: Connecticut does not offer a grace period for expired licenses. Operating after expiration exposes your business to the same penalties as operating without a license—including criminal liability.

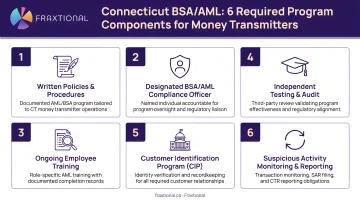

BSA/AML Program Maintenance Obligation

Licensees must maintain a written BSA/AML compliance program that includes:

- Written policies and procedures tailored to your specific business model

- Designated compliance officer (named and responsible)

- Employee training program (initial and ongoing)

- Independent testing (annual audit of AML program effectiveness)

- Customer identification program (CIP)

- Suspicious activity monitoring and SAR filing processes

Connecticut treats a federal BSA violation as a state violation — meaning a single compliance failure can trigger both federal penalties and state enforcement action simultaneously.

For early-stage fintechs without dedicated compliance staff, keeping a BSA/AML program current across both regulatory layers is one of the more operationally demanding requirements. Fraxtional places experienced BSA Officers and fractional CCOs directly with fintech teams, handling program management and regulator-facing obligations without the cost of a full-time hire.

Authorized Delegate Oversight Obligation

If you conduct business through authorized delegates (agents), you must:

- Execute written contracts obligating delegates to comply with the Act

- Conduct due diligence on delegates before engagement

- Monitor delegate activity on an ongoing basis

- Maintain liability for delegate violations and losses

You are legally liable for losses caused by your authorized delegates' failure to forward proceeds. Delegate oversight isn't a best practice — it's a statutory requirement with direct financial and legal exposure attached.

Recordkeeping and Reporting Requirements

Connecticut requires licensees to maintain records for at least five years, including:

- Records of each payment instrument sold

- General ledgers and bank statements

- Records of outstanding money transmissions

- Authorized delegate agreements and monitoring records

- SAR filings and supporting documentation

Material event reporting: You must provide written notice to the Commissioner no later than one business day after having reason to know of:

- Bankruptcy or receivership petitions

- License revocation or suspension proceedings in another state

- Cancellation or impairment of surety bond

- Felony indictments or convictions of the licensee, control persons, or authorized delegates

The one-business-day deadline is strict. Build internal processes to identify and report material events immediately.

Exemptions and Recent Regulatory Updates

Exemptions from Licensing

The following entities are exempt from Connecticut money transmitter licensure under Conn. Gen. Stat. § 36a-609:

- Federally insured banks and credit unions (state and federal)

- Connecticut innovation banks

- The United States Postal Service and its contractors

- Persons whose activity is limited to electronic funds transfer of governmental benefits for federal, state, or quasi-governmental agencies

Note: Authorized delegates of licensed money transmitters do not require their own separate license, provided they operate under a compliant written contract with the licensee.

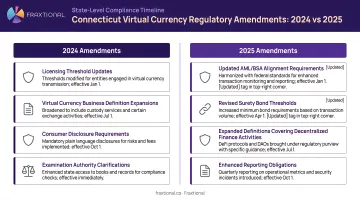

2024 Amendment: Virtual Currency Kiosk Operators

Public Act 24-146, effective October 1, 2024, explicitly brought virtual currency kiosk operators under the licensing regime.

Key requirements for kiosk operators:

- Must hold a Connecticut money transmitter license

- Must provide specific fraud warnings at kiosks

- Must issue detailed receipts for all transactions

- Must allow new customers to cancel and receive full refunds for fraudulent transactions within 72 hours (if reported to law enforcement within 30 days)

Before this amendment, crypto ATM operators had no clear licensing obligation under Connecticut law — that gap is now closed.

2025 Amendment: Digital Wallet Providers and Enhanced Virtual Currency Standards

Public Act 25-66, effective October 1, 2025, introduces sweeping changes for digital assets:

- Digital wallet providers are now explicitly included in the definition of money transmission, ending ambiguity about whether custodial wallet services require licensure.

- Licensees holding virtual currency must maintain the same type and amount owed to each customer — and cannot sell, lend, pledge, or otherwise encumber customer virtual currency without the customer's direction.

- Disclosure and receipt requirements now extend to all virtual currency transmitters, not just kiosk operators.

- FDIC advertising restrictions prohibit licensees from implying that non-deposit products, virtual currency, or digital assets are FDIC-insured.

- Sponsoring a money-sharing app account for a minor now requires notarized attestation of guardianship and ID verification, with a 30-business-day right for minors and parents to delete accounts and data.

Taken together, these two amendments mean that crypto firms, digital wallet providers, and fintech companies with any Connecticut nexus need to assess whether their current operations — or planned products — now fall under the state's licensing requirements.

Frequently Asked Questions

How do I renew my CT license?

Connecticut money transmitter licenses are renewed annually through NMLS between November 1 and December 31. Renewal requires updated financial statements, confirmation of surety bond and permissible investments, and payment of the $1,125 renewal fee.

What is the grace period for expired CT licenses?

Connecticut does not offer a formal grace period for expired licenses. Operating after expiration without a valid license exposes the business to the same penalties as operating without a license, including criminal liability under Conn. Gen. Stat. § 36a-597(b).

What is the penalty for operating as a money transmitter in Connecticut without a license?

Under Conn. Gen. Stat. § 36a-597(b), knowingly engaging in money transmission in Connecticut without a license is a Class D felony. Each transaction in violation constitutes a separate offense, meaning penalties multiply with transaction volume.

Do virtual currency businesses need a Connecticut money transmitter license?

Yes. Virtual currency kiosk operators have been required to hold a Connecticut money transmitter license since October 1, 2024. Digital wallet providers and virtual currency transmitters became subject to expanded licensing and compliance requirements as of October 1, 2025.

What is an "authorized delegate" under Connecticut's Money Transmission Act?

An authorized delegate is a person designated by a licensed money transmitter to provide money transmission services on its behalf. Authorized delegates of licensed entities do not need their own license but must operate under a written compliance contract with the licensee.

How long does it take to get a Connecticut money transmitter license?

The Connecticut Department of Banking does not publish official processing timeframes. Plan for 4-6 months minimum from submission to approval—incomplete applications or delayed responses to deficiency notices can add months to that timeline.