Recent enforcement actions tell the story. Since early 2024, 25.6% of the FDIC's formal actions have targeted sponsor banks, and 80% of sponsor banks report that meeting embedded finance compliance requirements is challenging. High-profile breakdowns—like Synapse Financial's collapse, which left a $60-$90 million shortfall and locked consumers out of their funds—demonstrate what happens when compliance, oversight, and operational alignment fail. For fintechs, the stakes are clear: choosing the wrong bank partner or entering negotiations without compliance readiness can result in failed deals, regulatory exposure, or lost charter access.

This guide walks through the critical factors fintechs and banks must evaluate before formalizing a partnership—from partnership model alignment and regulatory obligations to third-party risk management and operational infrastructure.

Key Takeaways

- Bank-fintech partnerships let fintechs access banking licenses and regulated product rails without becoming banks themselves

- Your partnership model—BaaS, white-label, or embedded finance—must fit your product, customer base, and growth stage

- Regulatory scrutiny has intensified—fintechs must demonstrate compliance program maturity before most banks will engage

- Banks evaluate partners on BSA/AML readiness, consumer protection controls, third-party risk, and governance infrastructure

- Fraxtional provides fractional BSA officers and compliance leadership to help fintechs meet sponsor bank requirements

What Are Bank-Fintech Partnerships?

Bank-fintech partnerships are formal arrangements where a fintech leverages a bank's charter, infrastructure, and regulatory approvals to offer financial products, or where a bank adopts fintech technology to modernize its services. These arrangements let fintechs deliver deposit accounts, payment cards, lending products, and embedded finance solutions without holding a banking license.

Partnership Models

Understanding the partnership structure is critical because each model determines regulatory obligations, oversight expectations, and compliance infrastructure requirements:

- Banking-as-a-Service (BaaS): Banks provide core banking functions via APIs, enabling fintechs to embed financial services into their platforms

- White-Label/Sponsor Bank Arrangements: Fintechs act as program managers under the bank's license, handling marketing and customer relationships while the bank maintains regulatory responsibility

- Embedded Finance: Financial products (payments, lending, insurance) are integrated into non-financial platforms, with the bank providing backend infrastructure

- Referral/Lead-Gen Models: Fintechs refer customers to banks in exchange for fees, with minimal operational integration

- Fintech-as-Vendor: Fintechs sell technology solutions directly to banks to modernize legacy systems

Model selection determines who holds compliance obligations, how revenue flows, and which regulatory frameworks apply.

Why Both Sides Enter These Partnerships

Fintech motivations:

- Access to regulated banking rails without the 15-18 month timeline and $2 million cost of direct bank integration

- FDIC insurance pass-through for deposit products

- Payment network access (Visa, Mastercard, ACH)

- Lower cost of capital through bank partnerships

Bank motivations:

- Innovation and digital capability without internal development costs

- Revenue diversification through fintech program fees

- Deposit growth—over half of sponsor banks' revenue (51.3%) and deposit income (51.4%) now comes from embedded finance partnerships

- Expanded customer reach into segments banks struggle to serve directly

As of Q3 2025, 156 U.S. sponsor banks were actively engaged in fintech partnerships — a number that signals how competitive sponsor bank selection has become for fintechs entering this space.

What to Consider When Forming a Bank-Fintech Partnership

With regulatory scrutiny rising and enforcement actions increasing, selecting the right bank and structuring the right arrangement requires careful evaluation across business strategy, compliance readiness, technology, and legal governance. These considerations apply whether you're a seed-stage startup approaching a community bank or a Series B company negotiating with a larger institution.

Partnership Model and Business Model Alignment

The partnership structure must match your product type, customer segment, and licensing strategy. A payments company needs different rails than a lending platform or a crypto custodian. Misalignment between business model and partnership model is one of the most common causes of partnership breakdown.

Key questions to ask:

- Who holds the customer relationship—the bank or the fintech?

- Who handles compliance obligations (AML monitoring, SAR filing, consumer complaints)?

- How does revenue flow between the bank and fintech?

- What product changes require bank approval before launch?

A fintech offering high-velocity payment processing needs a bank comfortable with that transaction volume and risk profile. A lending platform requires a bank with appetite for credit risk and regulatory experience in fair lending. If the bank's risk tolerance doesn't match your growth projections or product roadmap, the partnership will become a bottleneck.

Regulatory and Licensing Requirements

Different partnership models trigger different regulatory obligations. In July 2024, the OCC, FDIC, and Federal Reserve issued joint guidance on banks' arrangements with third parties to deliver deposit products and services, formalizing expectations that had previously been scattered across agency guidance. This marks a shift: regulatory expectations are now clearly documented, and fintechs must demonstrate alignment from day one.

Key federal frameworks fintechs must understand:

- BSA/AML: Bank Secrecy Act and Anti-Money Laundering requirements (31 U.S.C. § 5311)

- UDAAP: Unfair, Deceptive, or Abusive Acts or Practices under the Consumer Financial Protection Bureau

- Reg E: Electronic Fund Transfer Act requirements for error resolution, disclosure, and consumer protections

- FDIC Deposit Insurance: 12 CFR Parts 328 and 330 govern pass-through insurance and disclosure requirements

The joint guidance makes clear: a bank's use of third parties does not diminish its responsibility to comply with all applicable laws. Banks must conduct due diligence, enter contracts that clearly define roles, and establish policies to ensure compliance with consumer protection and AML requirements.

The practical implication for fintechs: you must demonstrate the infrastructure to support these obligations before banks will engage.

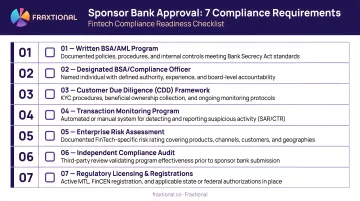

Your Compliance Program Readiness

Banks—especially sponsor banks—conduct detailed due diligence on the fintech's compliance management system (CMS) before agreeing to partner. A fintech without a functioning BSA/AML program, written policies, a designated compliance officer, and consumer protection controls will struggle to pass this review.

What "compliance readiness" looks like in practice:

- Named BSA Officer or Chief Compliance Officer

- Documented AML/KYC procedures aligned with bank and regulatory expectations

- Risk assessment framework identifying customer, product, and geographic risks

- Transaction monitoring policies and suspicious activity reporting (SAR) workflows

- Complaint handling processes and consumer protection controls

- Compliance training programs for staff and management

- Board-approved policies and procedures

Fintechs often underestimate this requirement until partnership discussions stall. Banks won't move forward without confidence that the fintech can maintain compliance standards that protect the bank's charter.

Fraxtional helps fintechs build and demonstrate this readiness through fractional CCO, BSA Officer, CAMLO, and MLRO placements — giving sponsor banks the confidence they need without the timeline or cost of a full-time executive hire.

Third-Party Risk Management Expectations

Banks are required by regulators to impose rigorous third-party risk management (TPRM) over their fintech partners. The June 2023 Interagency Guidance on Third-Party Relationships formalized these expectations, outlining due diligence, contract requirements, and ongoing monitoring obligations.

Fintechs should expect:

- Detailed due diligence questionnaires covering financial condition, risk management, information security, and compliance infrastructure

- SOC reports, penetration tests, and vulnerability assessments

- Contractual compliance obligations including audit rights, performance reporting, and incident escalation protocols

- Ongoing monitoring reviews on a quarterly or annual basis

Fintechs must proactively understand what TPRM obligations the bank will impose—data access requirements, reporting cadences, incident escalation expectations—and evaluate whether they have the internal infrastructure to meet them before entering negotiations.

Technology and Operational Alignment

API compatibility, data architecture, and core banking integration readiness determine whether a partnership launches on time and stays compliant. Mismatches in technology infrastructure lead to delayed launches, compliance monitoring gaps, and operational failures that can put the partnership at risk.

Key operational questions:

- Does the bank support open APIs or cloud-based core systems?

- What are the data-sharing and reconciliation requirements?

- How are transaction monitoring and fraud detection responsibilities divided between the fintech and the bank?

- Who manages customer data, and how is it shared for regulatory reporting?

- What are the uptime, latency, and disaster recovery expectations?

According to Cornerstone Advisors research, working directly with a bank typically requires 15-18 months and roughly $2 million to launch, whereas working with BaaS platform providers can reduce implementation time to less than two months and initial costs to $50,000. However, platform providers add a layer of complexity and cost over time, so fintechs must weigh speed-to-market against long-term control and economics.

Partner Bank Due Diligence

Fintechs must also evaluate the bank—not just the other way around. Four factors deserve close scrutiny:

- Regulatory standing: Research outstanding enforcement actions or consent orders. Banks under active scrutiny face heightened oversight of new fintech partnerships, which can delay or derail your deal.

- Fintech partnership experience: How many programs does the bank manage, and in which verticals? Speaking with other program managers reveals responsiveness, flexibility, and actual risk appetite better than any sales conversation.

- Business model fit: Does the bank have appetite for your specific model—high-risk verticals, crypto, cross-border payments, lending? A bank uncomfortable with your product launch pace or customer acquisition strategy will become a bottleneck.

- Charter type and geographic scope: Some banks operate under charter types or state regulations that limit product offerings or service areas — a constraint that may not surface until late in negotiations.

Vet the bank as rigorously as it vets you. A partner without demonstrated capability in your vertical will cost you time you don't have.

Common Risks and Pitfalls to Avoid

Recent enforcement actions highlight the most common failure points in bank-fintech arrangements:

BSA/AML program deficiencies — Evolve Bank & Trust faced a Federal Reserve enforcement action in June 2024 for AML, risk management, and consumer compliance failures tied to fintech partners. Key findings: inadequate transaction monitoring, weak suspicious activity reporting, and insufficient due diligence.

Board and management oversight gaps — Regulators expect active, documented oversight of fintech programs. Generic risk assessments and infrequent reviews won't pass scrutiny.

Insufficient third-party monitoring — Banks that fail to track fintech partners' compliance performance face enforcement exposure. This means regularly reviewing transaction data, SAR filings, customer complaints, and operational metrics.

FDIC deposit insurance misrepresentation — Under 12 CFR Part 328, fintechs must clearly disclose that FDIC insurance covers bank failure only — not fintech failure. Omitting that distinction is itself a misrepresentation.

Fragmented operations and recordkeeping failures — The CFPB filed a complaint against Synapse Financial Technologies in 2025 after it failed to maintain adequate consumer fund records and reconcile accounts with partner banks. The result was a $60–90 million shortfall and consumers locked out of their accounts — a direct consequence of unclear recordkeeping responsibilities.

Change management friction — Without formal escalation protocols, change management agreements, and defined contract roles, product updates and regulatory changes create compliance gaps on both sides. Speed mismatches between partners need structure, not assumptions.

Single-bank concentration risk — Over-reliance on one sponsor bank creates real vulnerability. The partnership contract should clearly define exit provisions, data portability rights, and continuity obligations before the relationship starts — not after it strains.

How Fraxtional Can Help

Fraxtional is a fractional compliance leadership firm that helps fintechs, crypto companies, and embedded finance businesses build the compliance infrastructure that sponsor banks and regulators require. With a director-led model, every client receives direct oversight from experienced compliance professionals—not junior consultants.

Fraxtional brings an established network of sponsor bank relationships and a track record of securing successful partnerships across the US, Canada, UK, and EU. The firm has been recognized as a Leader in Compliance (T100 Finance Award).

Key services relevant to bank-fintech partnerships:

- Fractional CCO, BSA Officer, CAMLO, and MLRO roles

- BSA/AML program development aligned with bank and regulatory expectations

- Regulatory readiness assessments covering BSA/AML, UDAAP, Reg E, and FDIC rules

- Third-party risk documentation and due diligence support

- Consumer compliance program design (UDAAP, Reg E)

- Pre-deal compliance reviews trusted by banks and investors

If you're preparing for a sponsor bank conversation, Fraxtional's pre-deal compliance reviews give banks the documentation and program evidence they need to move forward with confidence.

Frequently Asked Questions

What are bank fintech partnerships?

Bank-fintech partnerships are formal arrangements where fintechs access a bank's charter, infrastructure, and regulatory approvals to deliver financial products—or where banks adopt fintech technology to improve their services. They take many forms, from BaaS to white-label sponsor arrangements.

What is an example of a fintech partnership?

Chime, a financial technology company, offers debit cards and deposit accounts by partnering with The Bancorp Bank and Stride Bank as sponsor banks. Chime acts as the program manager while the banks hold the charter and provide FDIC insurance.

What do banks look for in a fintech partner?

Banks evaluate a mature compliance management system, a functioning BSA/AML program, consumer protection controls, a credible management team, and a business model that fits within the bank's risk appetite and regulatory posture.

What are the main compliance risks in bank-fintech partnerships?

BSA/AML program deficiencies, UDAAP and consumer protection violations, third-party oversight failures, and misrepresentation of FDIC deposit insurance were the most cited areas in 2024 regulatory enforcement actions against bank-fintech arrangements.

What is a sponsor bank relationship?

A sponsor bank relationship is a specific type of bank-fintech partnership where the bank provides its charter and regulatory licenses to a fintech acting as program manager. This structure lets the fintech offer regulated financial products without holding its own banking license.

How long does it take to form a bank-fintech partnership?

Timelines range from a few months to over a year, depending on the fintech's compliance readiness, the bank's due diligence process, contract negotiations, and any required regulatory approvals. Fintechs with strong compliance programs already in place tend to close partnerships faster.