Introduction

Crypto-related financial crime has reached unprecedented scale heading into 2026. Illicit crypto flows hit a record $158 billion in 2025, while an estimated $17 billion was stolen through cryptocurrency scams and fraud that same year. Regulators across the US, EU, and UK are responding with historic enforcement actions—Binance's $4 billion penalty in late 2023 marked the largest in US Treasury history, and BitMEX followed with a $100 million fine in 2025 for willfully failing to maintain adequate AML programs.

For virtual asset service providers (VASPs) and crypto businesses, the regulatory perimeter is tightening faster than most firms expected. The cost of falling behind is real: penalties, lost licenses, and severed banking relationships have become routine outcomes for unprepared operators.

This article covers the enforcement trends, emerging criminal typologies, and regulatory shifts — from Travel Rule compliance and MiCA implementation to AI-driven transaction monitoring — that crypto firms need to anticipate heading into 2026.

Key Takeaways

- Crypto firms need defensive AI tools now — fraudsters are automating attacks faster than manual compliance can catch them

- MiCA enforcement, updated FATF guidance, and US stablecoin rules all take effect in 2026, creating a multi-jurisdictional compliance crunch

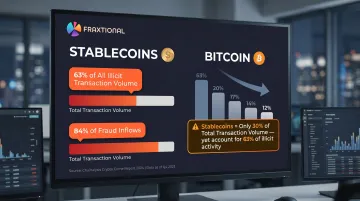

- Stablecoins now represent 63% of all illicit transaction volume, surpassing Bitcoin

- Travel Rule compliance is shifting from checkbox obligation to actively enforced requirement across 73% of FATF jurisdictions

- Growing crypto firms face mounting pressure to maintain director-level compliance oversight or risk significant penalties

Key Crypto AML Compliance Trends in 2026

Trend 1: AI as Both a Criminal Tool and a Compliance Enabler

Criminals are weaponizing AI to bypass traditional KYC controls. Impersonation scams surged by more than 1400% year-over-year in 2025, driven largely by deepfake technology and synthetic identity fraud. AI-enabled crypto scams now extract an average of $3.2 million per operation, 4.5 times more profitable than traditional methods.

FinCEN's November 2024 alert explicitly warned that criminals use generative AI to create falsified documents, photographs, and videos to defeat customer identification and verification processes.

Legacy rules-based AML systems cannot keep pace. Compliance teams are responding by deploying:

- AI-powered transaction monitoring and dynamic risk scoring

- Behavioral analytics that surface laundering patterns invisible to rules-based systems

- Real-time detection tools capable of tracking cross-chain movements

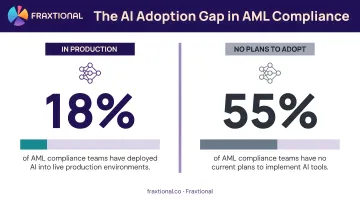

Defensive adoption, however, lags badly. An ACAMS/SAS survey found only 18% of AML professionals have AI/ML solutions in production, with 55% having no plans to adopt GenAI. VASPs that fail to upgrade onboarding flows with advanced biometric liveness checks and deepfake detection software remain vulnerable to synthetic identity infiltration at scale.

Trend 2: A Rapidly Expanding Regulatory Perimeter

The EU and US have fundamentally closed regulatory gaps around stablecoins and crypto-asset service providers, transitioning from guidance to strict, enforceable law.

EU MiCA and TFR Enforcement

The EU's Markets in Crypto-Assets Regulation (MiCA) entered full application for crypto-asset service providers (CASPs) on December 30, 2024. The Transfer of Funds Regulation (TFR), which mandates Travel Rule compliance, took full effect the same day. The EBA's Travel Rule Guidelines are now actively enforced across member states.

US GENIUS Act and FinCEN Rulemaking

The Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) passed in July 2025. In April 2026, FinCEN and OFAC issued joint proposed rulemaking to explicitly classify Permitted Payment Stablecoin Issuers (PPSIs) as financial institutions under the Bank Secrecy Act, requiring full AML/CFT and sanctions compliance programs.

FATF's Updated Guidance

The FATF's 2025 Targeted Update reports that 73% of jurisdictions (85 of 117) have now passed legislation implementing the Travel Rule, with enforcement now rapidly moving from legislation to active supervision.

The Cross-Border Compliance Burden

Crypto firms operating across the US, Canada, UK, and EU must now manage layered obligations across multiple jurisdictions simultaneously. Regulators increasingly share intelligence and coordinate enforcement, making jurisdiction-shopping strategies obsolete. Firms that cannot demonstrate robust, multi-jurisdictional AML programs face escalating penalties and potential loss of operating licenses.

Trend 3: Stablecoins and DeFi Face Heightened Scrutiny

Stablecoins now account for 63% of all illicit transaction volume, displacing Bitcoin as the asset of choice for criminals. TRM Labs data shows that while stablecoins represented just 30% of transaction volume between January and July 2025, they captured approximately 84% of fraud inflows during the same period.

The EU's TFR now requires CASPs to verify ownership of self-hosted addresses when transfer amounts exceed €1,000. This closes a critical AML visibility gap: once assets leave a regulated exchange into an unhosted wallet, traditional controls lose traceability.

DeFi protocols are squarely in regulators' crosshairs. OFAC sanctioned Tornado Cash in 2022 for laundering over $7 billion, including funds stolen by North Korea's Lazarus Group, and designated Sinbad.io in November 2023 as a key money-laundering tool. The US Treasury's 2023 Illicit Finance Risk Assessment of Decentralized Finance explicitly identified non-compliant DeFi services as the most significant current illicit finance risk in this domain.

Legislative proposals are accelerating. The CODE Act of 2025 (H.R.4394) proposes requiring decentralized finance services to implement risk-based AML programs meeting Bank Secrecy Act requirements.

Trend 4: Travel Rule Enforcement Tightens Globally

The FATF Travel Rule has moved from theoretical guidance to active enforcement across major jurisdictions. 85 jurisdictions have now passed Travel Rule legislation, with regulators urging rapid operationalization through effective supervision and enforcement.

Japan expanded its crypto Travel Rule framework in April 2025 to include 58 jurisdictions. Japanese VASPs must now gather, verify, and transmit originator and beneficiary data for qualifying transfers to counterparties in those countries.

The practical compliance gap is significant. Firms without automated Travel Rule solutions face escalating enforcement risk, and regulators are scrutinizing whether counterparty VASP due diligence is genuinely performed, not just documented on paper. Manual processes cannot scale, leaving non-compliant firms exposed to penalties and loss of banking relationships.

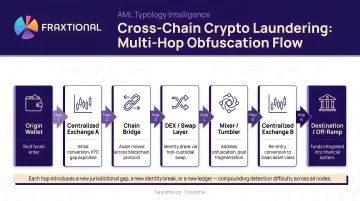

Trend 5: Cross-Chain Laundering and Advanced Obfuscation Tactics

Cross-chain criminal activity has exceeded $21.8 billion, with over $2.7 billion — around 12% — attributed to North Korean crypto hacks. To break the traceability that single-chain monitoring provides, criminals now routinely combine:

- Cross-chain bridges and decentralized exchanges

- Mixers and privacy coins

- Rapid wallet cycling across multiple networks

This multi-hop, cross-chain laundering is now the standard criminal playbook, specifically designed to evade detection. FinCEN's October 2023 NPRM on Convertible Virtual Currency Mixing highlighted "chain hopping" as a core obfuscation technique. The EU's TFR explicitly notes that EBA guidelines should include enhanced due diligence measures, including the use of distributed ledger technology (DLT) analytic tools, to detect the origin or destination of crypto-assets.

Regulators expect firms to demonstrate they can follow the money even when bad actors work to obscure it. Programs relying solely on single-chain exposure scores will fail this test — firms need cross-chain tracing tools and behavioral pattern detection capable of reconstructing layered transaction flows across ecosystems.

What's Driving These Crypto AML Trends

Five converging forces are reshaping what crypto AML compliance looks like in practice — and how fast firms need to move.

AI as a dual-use tool: Criminals are adopting AI to evade detection at the same pace regulators are requiring it for monitoring. Two-thirds of banks and insurers now use AI or machine learning primarily for fraud detection and AML — firms without it are already behind the curve.

Broader crypto adoption, bigger AML surface area: Stablecoins, tokenized assets, and institutional custody have pulled crypto into mainstream finance. That expansion draws regulatory scrutiny in proportion to its scale, and regulators are actively closing gaps before illicit activity can scale with them.

Mounting losses driving political pressure: The $158 billion in illicit crypto flows and $17 billion in fraud losses recorded during 2025 have made inaction politically untenable. Enforcement actions like Binance's $4 billion penalty and BitMEX's $100 million fine make clear that regulators now treat AML failures as a serious liability, not a paperwork problem.

Regulatory competition with global coordination: Governments want crypto business, but they're also coordinating through FATF to prevent firms from jurisdiction-shopping. For any firm operating across the US, UK, or EU, this means parallel obligations that are converging — not simplifying.

Compliance capacity gaps at growth-stage firms: Seed through Series B crypto firms rarely have the internal infrastructure to cover BSA/AML, Travel Rule, UDAAP, and cross-border requirements simultaneously. Building that capacity in-house takes time most early-stage firms don't have, which is why fractional compliance leadership has become a practical alternative rather than a workaround.

How These Trends Are Impacting Crypto Businesses

Operational Impact

Compliance workflows are becoming significantly more complex and expensive. Firms must now manage:

- Automated transaction monitoring with AI-powered behavioral analytics

- Travel Rule data exchanges with counterparty VASPs across dozens of jurisdictions

- Cross-chain blockchain analytics to trace multi-hop laundering

- Ongoing risk assessments tied to evolving regulatory guidance

- Enhanced due diligence for unhosted wallet transfers above threshold amounts

Manual processes are no longer viable at scale. The compliance infrastructure required to meet 2026 obligations demands technology, expertise, and continuous monitoring—creating operational overhead that strains lean teams and budgets.

Business Impact

Compliance has shifted from a back-office function to a board-level priority. Investors, sponsor banks, and regulators all require evidence of robust AML programs before partnerships or licensing approvals proceed. Firms without named compliance leadership—Chief Compliance Officers, BSA Officers, CAMLOs, or MLROs—face delays in securing banking relationships, investor diligence, and regulatory approvals.

This pressure is most acute for crypto firms scaling quickly. Sponsor banks increasingly require director-level compliance oversight as a condition of onboarding, and regulatory examiners expect named accountability for AML programs—not responsibility spread across junior staff.

Workforce Impact

The compliance talent gap in crypto is widening. Roles like BSA Officer, CAMLO, MLRO, and CCO with crypto-specific experience are in short supply. Full-time executives with digital asset expertise come with premium salaries, long hiring timelines, and equity expectations that many early-stage firms simply can't absorb.

Companies that cannot hire full-time compliance leadership are turning to fractional models to access director-level expertise without the cost and commitment of permanent hires. This approach provides immediate regulatory credibility, direct program oversight, and the flexibility to scale involvement as the business grows—so firms stay ahead of obligations without over-committing on headcount.

Future Signals for Crypto AML Compliance

Watch for these early indicators of materially higher compliance expectations within the next 1–3 years:

Real-time FIU data sharing across jurisdictions: Financial intelligence units are expanding cross-border intelligence sharing, enabling coordinated enforcement against VASPs operating in multiple regions. Firms that haven't harmonized AML programs across jurisdictions will face heightened scrutiny.

Expanded scope for DeFi and unhosted wallets: Legislative proposals like the CODE Act signal intent to extend AML obligations directly to decentralized finance protocols. Stablecoin-specific AML requirements are expected to enter legislation in the US and EU within 12–18 months.

On-chain AML compliance scoring: The Bank for International Settlements' Project Aurora proposes an "AML compliance score" based on the likelihood that a particular crypto-asset unit is tied to illicit activity, assessed each time it intersects with the banking system. If adopted, this would reshape how exchanges and banks assess transaction risk.

Smart contract-level compliance controls: Programmable compliance logic embedded directly into smart contracts enables real-time sanctions screening and transaction monitoring at the protocol level. Regulators may begin requiring these controls as a condition of licensing.

AI-driven behavioral profiling: Advanced behavioral analytics can detect illicit patterns before funds move off-chain, enabling preemptive freezing of suspicious transactions. Regulators are moving toward requiring proactive detection, not just reactive reporting.

These signals share a common thread: regulators are shrinking the window between a rule's proposal and its enforcement. Firms that have mapped their exposure to each of these areas — DeFi touchpoints, cross-border transaction flows, unhosted wallet activity — will spend less time scrambling when the requirements land. Those that haven't will face enforcement timelines that don't account for preparation gaps.

Frequently Asked Questions

What is crypto AML compliance?

Crypto AML compliance refers to the policies, procedures, and controls that virtual asset service providers and crypto businesses must implement to prevent money laundering and financial crimes—including KYC, transaction monitoring, risk assessments, and suspicious activity reporting.

What are the steps to AML compliance for crypto businesses?

Core steps include: conduct a risk assessment, implement a KYC/CDD program, appoint a compliance officer (MLRO/BSA Officer), establish transaction monitoring and SAR/STR reporting processes, maintain records, and conduct periodic audits of program effectiveness.

What are the new AML regulations affecting crypto in 2025 and 2026?

Key developments include MiCA's full enforcement in the EU extending AML obligations to all CASPs, the EU TFR Regulation mandating Travel Rule compliance, updated FATF guidance on VASPs, and ongoing US stablecoin and digital asset legislation expanding FinCEN obligations.

How often should a crypto AML risk assessment be updated?

Regulators typically require risk assessments to be reviewed at least annually, and more frequently when there are material changes in business model, product offerings, customer base, or regulatory environment.

Can law enforcement trace cryptocurrency transactions?

Yes. Blockchain analytics tools allow investigators to trace on-chain transactions. While mixers and privacy coins reduce traceability, cross-chain forensics and behavioral analysis have significantly advanced law enforcement's ability to follow illicit funds—as seen in high-profile seizures across the US and UK, including recoveries worth billions of dollars.

What are the latest crypto fraud trends compliance teams should watch?

Key current trends include: AI-generated deepfakes used to defeat KYC, synthetic identity fraud, pig butchering scams, ransomware payments in stablecoins, and cross-chain layering. All of these require behavioral monitoring that goes beyond simple transaction thresholds.