Introduction

Crypto's integration into mainstream finance has made compliance more complex and higher-stakes than ever. Enforcement actions are accelerating globally, with regulators imposing multimillion-dollar penalties and criminal liability against firms caught with deficient programs.

In December 2025, OFAC levied a $3.1 million penalty against Exodus Movement for sanctions violations stemming from third-party exchange integrations — demonstrating that even non-custodial platforms face direct regulatory accountability.

This guide is for compliance officers, founders, and risk teams at crypto firms, fintech startups, and money transmitters operating across the US, Canada, UK, and EU. Regulatory ambiguity is not a shield—agencies are enforcing existing financial crime laws against crypto companies without waiting for industry-specific statutes. Your firm will face scrutiny. The only variable is whether your compliance infrastructure is ready for it.

Key Takeaways

- Crypto compliance risks span AML/CFT failures, sanctions violations, asset classification disputes, and weak third-party due diligence — each carrying real fines and criminal exposure

- US, EU, UK, and Canadian regulators enforce against crypto firms regardless of statutory clarity

- Defensible programs require audit trails, transaction monitoring, sanctions screening, Travel Rule protocols, and embedded compliance in product design

- Early-stage crypto firms can access director-level compliance leadership without the cost of a full-time executive hire

Why Crypto Compliance Is Uniquely Challenging

The Structural Mismatch

Crypto's defining features—pseudonymity, decentralization, cross-border operability, and programmability—directly conflict with traditional compliance frameworks. Concepts like "customer identity," "jurisdiction," and "beneficial ownership" don't map cleanly onto blockchain infrastructure. A wallet address reveals transaction history but conceals the natural person or entity behind it.

Smart contracts execute autonomously across jurisdictions without geographic anchors. This structural tension forces crypto firms to apply traditional compliance controls onto blockchain infrastructure they were never designed to govern.

The Regulatory Vacuum Problem

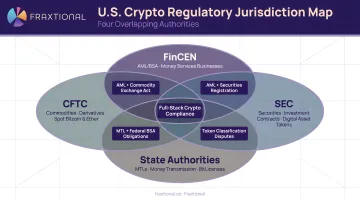

Unlike banks operating under clear statutory mandates, crypto companies navigate overlapping jurisdiction without clear delineation. In the US alone:

- FinCEN treats many crypto firms as Money Services Businesses (MSBs) subject to Bank Secrecy Act obligations

- SEC asserts securities jurisdiction over tokens meeting the Howey test

- CFTC claims commodity oversight for Bitcoin and derivative products

- State regulators impose money transmission licensing requirements independently

The UK's FCA, EU member states implementing MiCA, and Canada's FINTRAC each apply distinct frameworks. No single regulator owns the full compliance picture—and the gaps between them don't protect companies from enforcement.

Enforcement Outpacing Regulation

Agencies are bringing actions under existing financial laws without crypto-specific statutes. The Bittrex enforcement resulted in over $53 million in combined penalties for BSA and sanctions violations—applying decades-old rules to a 2014-founded exchange. Regulators don't pause enforcement while clarity develops. The expectation is that firms identify their obligations and build programs accordingly—ambiguity is not a defense.

The Top Cryptocurrency Compliance Risks

Risk 1: AML/CFT Exposure

Regulators treat crypto's pseudonymous structure as high-risk for money laundering and terrorist financing. The Bank Secrecy Act applies to crypto firms classified as MSBs, requiring:

- Customer Identification Program (CIP) with identity verification

- Transaction monitoring tuned to crypto-specific risks

- Suspicious Activity Report (SAR) filing for unusual patterns

- Independent testing and designated BSA Officer

Enforcement reality: In 2022, BitMEX founders faced criminal prosecution under BSA for operating without an adequate AML program. The exchange processed billions in transactions while willfully failing to implement basic KYC. Bittrex paid $24 million to OFAC and $29 million to FinCEN for sanctions and BSA violations spanning 2014-2018.

Regulators scrutinize whether your monitoring detects:

- Cross-chain transactions obscuring fund origins

- Interaction with mixing services or tumblers

- High-risk wallet addresses tied to darknet markets

- Structured transactions below reporting thresholds

Risk 2: Sanctions Compliance Failures

AML failures rarely exist in isolation — sanctions exposure compounds them. Crypto firms must screen wallets and transactions against OFAC's Specially Designated Nationals (SDN) list, HM Treasury's consolidated list, and EU sanctions. Blockchain's pseudonymity doesn't reduce those obligations; it makes them significantly harder to meet.

Critical compliance tools now expected:

- IP geolocation to block sanctioned jurisdictions

- On-chain analytics to trace wallet ownership

- Real-time screening against updated SDN lists

- Enhanced due diligence for high-risk counterparties

The Exodus case demonstrates accountability follows the entire service chain. When Exodus's third-party exchange partner blocked Iranian users, Exodus customer service actively recommended VPNs to circumvent controls, facilitating sanctions violations. Even as a non-custodial wallet provider, Exodus paid $3.1 million.

Risk 3: Regulatory Classification Risk

Whether a crypto asset is a security, commodity, or currency determines:

- Which regulator has jurisdiction

- Registration and disclosure requirements

- Permissible distribution channels

- Ongoing reporting obligations

The SEC vs. CFTC jurisdictional debate remains unsettled. Companies that misclassify products face retroactive enforcement — tokens sold as utilities may be deemed securities years later, triggering registration violations and investor rescission rights. Regulatory ambiguity shifts risk onto firms, not away from them.

Risk 4: Third-Party and Counterparty Risk

Regulators hold crypto companies accountable for their partners' compliance. The June 2023 Interagency Guidance on Third-Party Relationships applies explicitly to fintech and crypto partnerships, requiring:

- Due diligence before engagement

- Ongoing monitoring of third-party controls

- Contractual accountability for compliance obligations

- Documentation of risk assessments

Weak counterparty vetting creates direct liability. If your liquidity provider lacks sanctions screening or your API partner serves prohibited jurisdictions, your firm inherits the compliance failure.

The Federal Reserve, FDIC, and OCC have confirmed they will pursue enforcement "when necessary to address violations of laws and regulations or unsafe or unsound banking practices by the banking organization or its third party."

Risk 5: Data Security and Cybersecurity Risk

Crypto firms hold sensitive customer financial data and often private key infrastructure, making them high-value targets. Unlike traditional finance where fraudulent transfers can be reversed, stolen crypto is largely unrecoverable.

Examiners now expect documented controls across every layer of the stack:

- Multi-factor authentication for customer access

- Cold storage for customer assets

- Incident response plans with notification protocols

- Regular penetration testing and vulnerability assessments

- Data retention policies covering trading records, communications, and audit logs

Cybersecurity failures that result in customer asset loss trigger regulatory scrutiny beyond the breach itself — examiners investigate whether the firm maintained adequate controls and whether governance failures enabled the incident.

Navigating Multi-Jurisdictional Regulatory Obligations

EU: MiCA Framework

The Markets in Crypto-Assets Regulation establishes the most detailed single-jurisdiction crypto regulatory framework currently in force. MiCA requires:

- Authorization: Crypto Asset Service Providers (CASPs) must obtain licenses to operate in or into EU member states

- Stablecoin reserves: Issuers must maintain 1:1 reserves with segregated custody

- Consumer protection: Disclosure requirements, complaint handling, and conflict-of-interest management

- Market integrity: Transaction reporting and market manipulation prohibitions

MiCA creates regulatory clarity, but it demands significant infrastructure investment. Companies must classify their activities correctly before operating — unauthorized CASPs face severe financial and operational penalties.

US: Regulatory Patchwork

The US requires navigating four regulatory layers simultaneously:

Federal level:

- FinCEN: MSB registration, BSA/AML program, SAR filing, recordkeeping

- SEC: Securities registration if tokens are securities

- CFTC: Derivatives registration for commodity-based products

State level:

- Money transmission licenses in each operating state (often 40+ separate applications)

- Varying net worth and bonding requirements

- State-specific examination cycles

Pending legislation like FIT21 and the Stablecoin Transparency Act may reshape this landscape. That shift could be years away — firms operating today must build compliance programs under current law, not anticipated law.

UK and Canada: Registration and AML Obligations

United Kingdom:

- FCA registration required under Money Laundering Regulations

- Travel Rule compliance for transfers above thresholds

- Cryptoasset promotions must be approved by authorized firms

Canada:

- FINTRAC registration as virtual asset service providers (VASPs)

- PCMLTFA obligations including transaction reporting

- Provincial securities requirements for token offerings

The Travel Rule Imperative

One obligation applies regardless of which jurisdictions you operate in. The FATF Recommendation 16 requires VASPs to collect and transmit originator and beneficiary information for transfers above specified thresholds (typically $1,000/€1,000). This includes:

- Full name of originator and beneficiary

- Account numbers or wallet addresses

- Physical addresses

- National identity numbers where applicable

Enforcement is tightening globally. Firms transacting with higher-risk exchanges or unhosted wallets without compliant Travel Rule protocols face growing regulatory exposure.

The FATF notes that "counterparty due diligence ensures VASPs avoid dealing with illicit or sanctioned actors." In practice, that means vetting every counterparty VASP before sending or receiving transfers — not just at onboarding, but on an ongoing basis as risk profiles change.

Building a Resilient Crypto Compliance Program

Core Program Components

A defensible program includes:

KYC/KYB onboarding:

- Identity verification using government-issued documents

- Biometric authentication where feasible

- Beneficial ownership disclosure for entities

- Enhanced due diligence for high-risk customers

Transaction monitoring:

- Rules tuned to crypto-specific patterns (mixing services, cross-chain activity, high-risk wallet interactions)

- Velocity checks detecting unusual transaction volumes

- Geo-blocking for sanctioned jurisdictions

- Alert workflows with documented case decisions

Sanctions screening:

- Real-time checks against OFAC SDN, HMT, and EU consolidated lists

- Ongoing screening (not just onboarding)

- Fuzzy logic to catch name variations and aliases

- IP and on-chain analytics integration

SAR/STR filing workflows:

- Clear escalation paths from alerts to investigations to filings

- Quality assurance review before submission

- Documentation of investigative steps and conclusions

- Tracking to meet filing deadlines

Data retention:

- Five-year minimum for transaction records, communications, and customer information

- Audit logs demonstrating system access and controls

- Retrievable format for examiner requests

Audit Trails and Documentation Culture

Regulators evaluate whether compliance is embedded in organizational culture, not just present in policies. In the FTX enforcement, absent or inadequate documentation served as evidence of bad intent.

Every material compliance decision should leave a paper trail. That includes:

- Compliance decisions with documented rationale

- Third-party due diligence reports and ongoing monitoring

- Internal and external audit findings with remediation tracking

- Board or executive reporting demonstrating oversight

Engineering and Compliance Integration

Strong documentation culture only holds if the underlying systems support it. That means compliance must be embedded in product design from day one — data auditability, transaction traceability, and access controls cannot be retrofitted successfully.

Technical requirements:

- Immutable transaction logs

- Role-based access controls limiting data exposure

- Automated sanctions screening integrated at transaction initiation

- APIs supporting Travel Rule data exchange

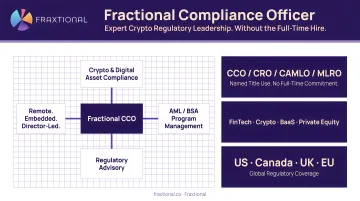

Fractional Compliance Leadership

Most crypto startups and growth-stage companies cannot budget for a full-time Chief Compliance Officer or BSA Officer. In this enforcement environment, that's a real problem — director-level expertise is a practical necessity, not a nice-to-have.

Fractional compliance models fill that gap. Firms like Fraxtional, a T100 Finance Award honoree for compliance leadership, provide experienced CCOs, BSA Officers, and MLROs across the US, Canada, UK, and EU without the full-time commitment. This model delivers:

- Immediate deployment without 6-12 month hiring cycles

- Cost efficiency at 50-70% less than full-time positions ($25,000+/month)

- Scalability matching funding stage and transaction volume

- Named officer status in regulatory filings and banking relationships

Where Crypto Companies Most Often Fall Short

Treating Compliance as an Afterthought at Launch

The most common compliance failure is treating compliance as a post-product problem. Startups onboard users without adequate KYC, transaction monitoring, or sanctions screening. By the time regulators examine the firm, it has operated with a deficient program for months or years. Retroactive remediation is far harder and more expensive than building correctly from the start.

Insufficient Due Diligence on Partners and Counterparties

Many crypto firms conduct minimal due diligence on liquidity providers, custodians, payment processors, or exchange partners. Given that regulatory accountability follows the entire chain, one non-compliant partner exposes an otherwise compliant company to serious risk. The Exodus case demonstrates this liability clearly: facilitating a partner's sanctions control circumvention triggered a $3.1 million penalty.

Inconsistent Recordkeeping That Can't Withstand Scrutiny

Without express statutory requirements like those in traditional finance, many crypto companies either don't maintain records or maintain them inconsistently. Regulators treat poor recordkeeping as evidence of a deeper compliance culture problem. The absence of records makes defending against enforcement inquiries nearly impossible—even when no wrongdoing occurred.

The practical takeaway across all three gaps: compliance weaknesses are rarely isolated. Deficient onboarding, weak partner diligence, and missing records tend to cluster together—and regulators notice the pattern.

Frequently Asked Questions

Frequently Asked Questions

What are the regulatory risks of crypto?

Primary risks include AML/BSA non-compliance, sanctions violations, asset misclassification, and failure to meet multi-jurisdictional licensing requirements. Enforcement actions have reached into the billions — Binance's 2023 settlement hit $4.3B — and executives face personal criminal liability.

What is the Travel Rule in crypto compliance?

The Travel Rule (FATF Recommendation 16) requires VASPs to collect and transmit originator and beneficiary information for crypto transfers above specified thresholds. Enforcement is tightening globally across the US, UK, EU, and Canada.

What happens if a crypto company fails to comply with AML requirements?

Failures trigger civil penalties from FinCEN and OFAC, criminal prosecution under the BSA, and loss of banking relationships. Individual enforcement actions have reached hundreds of millions to billions of dollars, with executives facing personal prosecution.

Do crypto companies need to register with FinCEN?

Yes — firms that exchange, transmit, or administer virtual currencies generally qualify as MSBs under FinCEN rules. Registration is mandatory, along with a BSA/AML program, SAR filing obligations, and record-keeping requirements.

How does MiCA regulation affect crypto companies operating in the EU?

MiCA requires crypto asset service providers operating in or into EU member states to obtain authorization, meet reserve and disclosure requirements for stablecoins, and comply with consumer protection obligations — establishing the EU's first unified crypto regulatory framework.

What is a fractional compliance officer and does a crypto startup need one?

A fractional compliance officer is an experienced CCO, BSA Officer, or MLRO who provides director-level oversight on a part-time or project basis. For early-stage crypto companies, it's a practical way to meet regulatory obligations without the cost of a full-time executive hire.