This article serves two audiences: crypto users wondering why exchanges demand personal data, and crypto firms navigating compliance obligations. We'll cover what KYC is, how verification works, why it's legally required, and what it takes to build a compliant program that satisfies both regulators and sponsor banks.

Key Takeaways

- KYC verifies user identities through three stages: customer identification, due diligence, and ongoing monitoring

- Required under AML law in most jurisdictions, including the U.S. Bank Secrecy Act and EU directives

- Only custodial wallets and regulated exchanges must enforce KYC—DEXs and non-custodial wallets generally are not

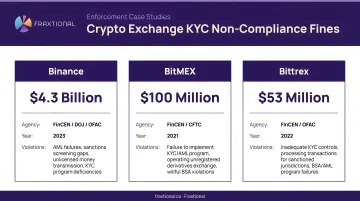

- Non-compliance carries billions in fines, as seen in recent enforcement against Binance ($4.3B), BitMEX, and Bittrex

- Firms without a structured KYC program risk regulatory penalties, banking access, and market credibility

What Is KYC in Crypto?

KYC (Know Your Customer) is the process of verifying a customer's identity before granting access to financial services. In crypto, this applies to exchanges, custodial wallet providers, and Virtual Asset Service Providers (VASPs) that handle transactions on behalf of users.

KYC serves as the first layer of AML (anti-money laundering) due diligence. Its primary purpose: prevent bad actors from using crypto platforms to launder money, finance terrorism, or commit fraud. Crypto's pseudonymous nature makes these checks especially critical—while transactions are publicly visible on-chain, linking those transactions to real-world identities requires deliberate verification.

The Liberty Reserve Wake-Up Call

The 2013 Liberty Reserve case was the event that forced crypto KYC onto regulators' agenda. The platform operated an underground cyber-banking system, processing over 78 million transactions worth more than $8 billion with minimal oversight. Founder Arthur Budovsky pleaded guilty in 2016 to laundering more than $250 million in criminal proceeds.

The coordinated shutdown—involving the U.S. Attorney's Office, Secret Service, IRS-Criminal Investigation, and Homeland Security—established a clear precedent: digital currency platforms operating without identity controls would face federal prosecution.

KYC Doesn't Mean Giving Up Privacy

KYC is not about eliminating privacy. There's a clear distinction between privacy (the right to control your personal data) and anonymity (hiding identity for potentially malicious purposes). KYC-compliant platforms protect user privacy through data encryption, limited disclosure, and strict access controls—while still satisfying their legal obligations.

Who Needs KYC?

Required:

- Centralized exchanges (CEXs) like Kraken, Coinbase

- Custodial wallet providers holding user private keys

- Fiat-to-crypto on-ramps and off-ramps

Not required:

- Decentralized exchanges (DEXs) operating without custody

- Non-custodial wallets where users control their own keys

How KYC Works on Crypto Exchanges: The Verification Process

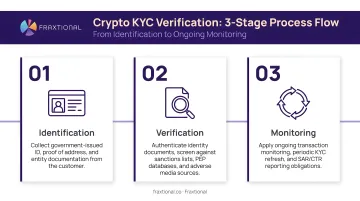

A compliant KYC program is built around three sequential layers: Customer Identification Program (CIP), Customer Due Diligence (CDD), and Ongoing Monitoring. Together, they form the framework that prevents exchanges from becoming conduits for illicit funds.

Customer Identification Program (CIP)

During onboarding, exchanges collect:

- Full legal name

- Date of birth

- Residential address

- National ID number

- Government-issued photo ID (passport or driver's license)

- Proof of address (utility bill or bank statement)

- Selfie or liveness check to confirm the document belongs to the submitter

FinCEN's CDD Rule requires written policies to identify customers, verify beneficial owners of legal entities (individuals owning 25% or more), understand the nature of customer relationships, and conduct ongoing monitoring.

Customer Due Diligence (CDD)

After collecting documents, exchanges verify them against authoritative databases and screen users against:

- Sanctions lists (OFAC, UN, EU)

- Politically Exposed Persons (PEPs) watchlists

- Adverse media sources

Higher-risk users trigger Enhanced Due Diligence (EDD), which typically includes source of funds verification and beneficial ownership checks for business accounts.

Each user also receives a risk score based on identity data, transaction behavior, jurisdiction, and account history. That score directly determines transaction limits, withdrawal privileges, and whether additional review is required.

Ongoing Transaction Monitoring

Once a risk profile is assigned, surveillance begins. Exchanges continuously review account activity for patterns that don't fit the user's stated purpose or behavior baseline:

- Large or rapid transactions inconsistent with user profile

- Transfers to high-risk jurisdictions

- Behavior mismatched with stated purpose

Flagged activity must be reported to financial authorities. In the U.S., Money Service Businesses must file a Suspicious Activity Report (SAR) within 30 days for transactions of at least $2,000 that appear suspicious.

Verification timelines:

| Platform | Verification Type | Processing Time |

|---|---|---|

| Kraken | Standard (Automated) | Instant |

| Kraken | Standard (Manual) | ~45 minutes |

| Coinbase | Standard ID Check | Within 24 hours |

| Jumio | Automated IDV | Real-time/seconds |

Why Crypto Exchanges Are Required to Implement KYC

Regulatory Classification

In the U.S., most crypto exchanges converting fiat to crypto are classified as Money Service Businesses (MSBs) under FinCEN's interpretation of the Bank Secrecy Act (BSA).

This means BSA/AML obligations—including KYC—apply directly.

Global Regulatory Landscape

- European Union: The 5th Anti-Money Laundering Directive (5AMLD) extended AML/CFT obligations to crypto exchange services and custodian wallet providers. The 6th AMLD (2024) further harmonized rules across member states. The Markets in Crypto-Assets Regulation (MiCA), which entered force in June 2023, institutes uniform EU market rules covering authorization, disclosure, and supervision of Crypto-Asset Service Providers.

- FATF Recommendation 16 (Travel Rule): Requires VASPs to share originator and beneficiary information on transactions above USD/EUR 1,000, extending KYC obligations to counterparty data sharing between exchanges.

The Cost of Non-Compliance

Regulators are levying substantial penalties for KYC/AML failures:

| Firm | Regulator(s) | Fine Amount | Year | Violation |

|---|---|---|---|---|

| Binance | FinCEN, OFAC, DOJ, CFTC | $4.3B | 2023 | Willfully failed to establish effective AML program, failed to perform KYC on large number of users, failed to report 100,000+ suspicious transactions |

| BitMEX | CFTC, DOJ | $200M | 2021/2025 | Failed to establish adequate AML/KYC program; operated unregistered platform |

| Bittrex | FinCEN, OFAC | $53M | 2022 | Failure to maintain effective AML program; failure to file SARs; sanctions violations |

Non-compliance is a business risk, not just a legal technicality.

Banking Access and Institutional Investment

Crypto firms lacking robust KYC programs are routinely denied banking relationships and institutional investment. Sponsor banks conduct thorough compliance reviews before onboarding crypto clients, specifically examining:

- AML framework design and documented policies

- Independent testing results and audit findings

- Agent management practices and oversight controls

According to FinCEN's Interagency Interpretive Guidance, banks must also confirm MSB registration, state licensing, and complete BSA/AML risk assessments before providing services. Without passing that review, a crypto firm can't access the banking rails it needs to operate.

KYC vs. AML: Understanding the Relationship

KYC is a component of AML — not a standalone obligation. AML is the broader compliance framework covering policies, controls, and reporting designed to prevent money laundering. KYC is the identity verification piece that feeds into AML risk assessment and informs how a firm classifies and monitors each customer.

AML programs include:

- Transaction monitoring systems

- Suspicious Activity Report (SAR) filing

- Employee training and awareness

- Designated compliance officer oversight

- Internal audits and testing

KYC without a full AML program leaves a firm exposed. Regulators — including FinCEN in the U.S. and the FCA in the UK — examine the entire program, not just whether identity checks are in place.

The Crypto Travel Rule

While KYC verifies individual users, the FATF Travel Rule extends identity verification to counterparty transactions. FATF Recommendation 16 requires VASPs to obtain, hold, and transmit originator and beneficiary information for transfers above USD/EUR 1,000.

Required data fields for each transfer:

| Party | Required Information |

|---|---|

| Originator | Name, wallet address, physical address or national ID, date and place of birth |

| Beneficiary | Name and wallet address |

Buying Crypto Without KYC: What You Should Know

It's technically possible to acquire crypto without KYC through:

- Crypto ATMs (within transaction limits)

- Decentralized exchanges (DEXs) like Uniswap or Bisq

- Peer-to-peer (P2P) platforms

None of these are automatically illegal — but each comes with regulatory and practical risks that operators and users need to understand.

Legal Status

For end users, buying crypto without KYC is not automatically illegal in most jurisdictions. However, using platforms that violate local regulatory requirements can expose both the platform and users to legal risk — and OFAC sanctions violations apply regardless of what platform type is used.

Recent Enforcement

| Platform | Regulator | Year | Outcome |

|---|---|---|---|

| Paxful | FinCEN | 2025 | $3.5M penalty for willful BSA violations, failure to register as MSB, failure to file SARs |

| Bitzlato | DOJ, FinCEN | 2023 | Founder arrested for operating unlicensed money transmitting business; identified as "primary money laundering concern" |

| Tornado Cash | OFAC | 2022 | Added to SDN List for laundering $7B+ in virtual currency |

Practical Risks for Users

- Scam and manipulation rates are significantly higher on non-KYC platforms

- Recovering assets from unregulated platforms is difficult, with limited legal recourse

- On-chain activity is traceable regardless of KYC status — Form 1099-DA requirements now require brokers to report gross proceeds from digital asset sales starting with 2025 transactions

Building a Compliant KYC Program for Your Crypto Exchange

Every crypto exchange needs the same foundational components to satisfy regulators and banking partners. A compliant KYC framework includes:

- Documented Customer Identification Program (CIP)

- Risk-based Customer Due Diligence (CDD) procedures

- Sanctions screening process (OFAC, PEPs, adverse media)

- Transaction monitoring capabilities

- SAR filing procedures

- Designated compliance officer or BSA Officer

The Challenge for Growing Crypto Firms

Building this infrastructure from scratch requires regulatory expertise across multiple jurisdictions: BSA/AML obligations, FATF standards, and local licensing requirements. For most startups and Series A-B companies, that depth of knowledge is difficult to justify as a full-time hire.

Fractional compliance leadership fills that gap. Experienced Chief Compliance Officers, BSA Officers, or Chief AML Officers provide director-level oversight on a flexible basis — letting firms meet their obligations without the cost of a permanent executive.

Fraxtional, a T100 Finance Award recipient for compliance leadership, operates this way for crypto and fintech firms across the U.S., Canada, UK, and EU. Its Directors embed directly with client teams to lead AML framework design, SAR workflows, sanctions screening, and sponsor bank relationship support — all aligned with FinCEN guidelines and FATF travel rules.

Key Operational Decisions

When building KYC infrastructure, exchanges face three core decisions:

KYC technology vendors — Select document verification providers, liveness detection tools, and sanctions screening platforms that integrate with your onboarding flow.

Tiered verification levels — Define what each tier requires:

- Basic: Lower transaction limits, standard ID documents

- Advanced: Higher limits, enhanced identity verification

- Institutional: Beneficial ownership documentation, source of funds

Audit trails — Maintain version-controlled policies, monitoring dashboards, SAR summaries, sanctions logs, and QA reports structured for regulatory review.

These systems must satisfy both regulators and potential banking partners.

Frequently Asked Questions

How does KYC work in crypto?

Crypto KYC requires users to submit identity documents (government ID, proof of address, selfie) during onboarding. The platform verifies documents against official databases and screens against sanctions and PEP lists before granting account access.

Is KYC required for crypto?

KYC is legally required for regulated exchanges, custodial wallet providers, and fiat-to-crypto platforms in most jurisdictions—especially in the U.S. under the BSA and in the EU under AMLD. DEXs and non-custodial wallets generally are not required to implement KYC.

Is it illegal to buy crypto without KYC?

For end users, buying crypto without KYC is not automatically illegal in most countries. However, using platforms that are themselves non-compliant can carry legal risk. Sanctions violations and tax reporting obligations apply regardless of the platform's KYC status.

How long does KYC verification take on crypto exchanges?

Verification time varies by platform and method. Automated KYC systems complete verification in minutes, while manual reviews may take hours to 24+ hours. Document quality, jurisdiction, and platform technology are the main factors.

Is KYC safe for cryptocurrency?

Reputable exchanges are legally required to protect submitted personal data with encryption and access controls. KYC also makes platforms harder to exploit for fraud—so it protects users, not just regulators. Before submitting documents, confirm the exchange holds a valid license in your jurisdiction.

Can the IRS see your crypto wallet?

The IRS cannot monitor wallets in real-time, but all blockchain transactions are publicly traceable. Regulated exchanges report user data directly to the IRS, and the agency uses blockchain analytics to identify taxable activity whether or not a platform runs KYC.