Introduction

Picture this: a fintech founder receives an email from a promising investor asking for a compliance review call. The first question? "What does your GRC program look like?" The team scrambles to piece together fragmented policies, outdated risk spreadsheets, and incomplete audit logs—realizing too late that governance, risk, and compliance weren't just checkboxes for later-stage companies.

GRC is no longer a concern only for multinational banks. For any financial services company—especially fintechs, crypto platforms, and money transmitters operating under intense regulatory scrutiny—a functioning GRC program is foundational infrastructure. Non-compliance costs organizations an average of $14.82 million annually—2.71 times higher than the $5.47 million cost of maintaining a compliant program.

Governance, Risk, and Compliance (GRC) is an integrated approach that helps organizations set clear policies, identify and manage threats, and meet regulatory obligations as one unified strategy—not three disconnected functions.

This guide breaks down each pillar, explains why GRC is especially critical in fintech and financial services, and shows how to build a working program even without a full-time compliance executive.

Key Takeaways

- GRC stands for Governance, Risk, and Compliance—three interconnected disciplines ensuring reliable, ethical operations

- Governance establishes accountability; risk management identifies threats; compliance enforces regulatory adherence

- Siloed GRC creates duplicated effort, blind spots, and costly regulatory exposure

- Fintech and crypto firms navigate dense requirements: BSA/AML, UDAAP, Reg E, GDPR, and more

- Fractional compliance leadership lets early-stage companies build credible GRC without full-time executive hires

What Is GRC? The Three Pillars Explained

The acronym "GRC" was coined by the Open Compliance and Ethics Group (OCEG) in 2002 and formalized in academic literature in 2007. GRC emerged following high-profile corporate failures like Enron and WorldCom, which exposed the dangers of disconnected governance and risk functions and led to the Sarbanes-Oxley Act of 2002.

For fintech, crypto, and banking operators, understanding each pillar isn't academic — it determines whether your organization can scale, retain banking partners, and survive regulatory scrutiny.

Governance

Governance is the system of policies, rules, and frameworks that shapes how an organization makes decisions, assigns accountability, and maintains oversight—from the board level down to daily operations. Key elements include:

- Ethics and conflict resolution policies

- Resource allocation and spending controls

- Transparency in reporting and oversight

- Decision-making authority structures

Without governance, teams lack clear directives, accountability gaps emerge, and consistent compliance becomes impossible. In practice, governance defines the boundaries within which risk is tolerated and compliance obligations are prioritized.

Risk Management

Risk management is the process of identifying, assessing, and prioritizing potential threats to the organization—financial, legal, operational, strategic, and cybersecurity risks—then mitigating, transferring, or monitoring them before those threats materialize into losses.

Effective risk management anticipates problems rather than responding to them. Organizations use tools like:

- Risk registers documenting identified threats and controls

- SWOT analyses to surface strategic vulnerabilities

- Scenario planning to test resilience

In fintech, common risks include fraud exposure, AML/BSA violations, third-party vendor risk, and data breach liability.

Compliance

Compliance means adhering to — and demonstrating adherence to — mandatory regulations and voluntary standards. For fintech and banking companies operating in the US and UK, that includes frameworks such as BSA/AML, UDAAP, Reg E, GDPR, HIPAA, and SOX.

Regulations change, enforcement evolves, and new requirements emerge continuously. The consequences of falling behind include:

- Regulatory fines and enforcement actions

- Loss of money transmitter or banking licenses

- Reputational damage with customers and investors

- Severed sponsor bank relationships that can shut down operations entirely

Compliance isn't a one-time project — it's an ongoing operational function.

Why GRC Matters — Especially for FinTech and Financial Services Companies

While all industries need GRC, the stakes are uniquely high in financial services. Companies operate under direct regulatory oversight, must maintain relationships with sponsor banks and payment networks, and handle sensitive consumer financial data.

The Cost of Getting It Wrong

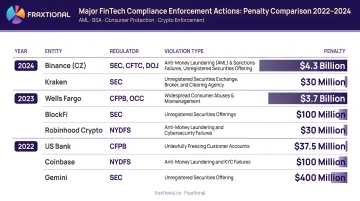

Financial services firms face severe penalties for compliance failures. These aren't edge cases — enforcement actions have hit some of the most recognized names in the industry:

| Company | Regulator | Penalty | Primary Violation | Year |

|---|---|---|---|---|

| Binance | FinCEN/DOJ | $3.4 billion | Failure to register as MSB and maintain AML program | 2023 |

| Wells Fargo | CFPB | $3.7 billion | Mismanagement of loans and surprise overdraft fees | 2022 |

| Cash App | CFPB | $175 million | Failure to investigate unauthorized transactions | 2024 |

| Bittrex | FinCEN | $29.2 million | Failure to maintain AML program and file SARs | 2022 |

Navigating Regulatory Density

Behind each of those enforcement actions is a specific regulatory requirement that wasn't met. Fintechs must navigate several overlapping frameworks simultaneously:

- BSA/AML: Money Services Businesses must register with FinCEN, establish written AML programs, and file SARs and CTRs

- UDAAP: Prohibits unfair, deceptive, or abusive acts that take advantage of consumer lack of understanding

- Regulation E: Governs electronic fund transfers, establishing error resolution responsibilities

- GDPR: Applies to US fintechs handling EU residents' data, requiring lawful basis for data processing and enforceable data subject rights