Introduction

FinTech companies managing payment data, customer financial records, or cryptocurrency assets face a hard reality: enterprise clients, investors, and sponsor banks now expect SOC 2 compliance before signing contracts or closing funding rounds.

Yet most seed-to-Series B companies don't know where their readiness gaps actually lie until a formal audit surfaces them—often too late to avoid deal delays or failed examinations.

67% of companies report losing business deals due to customer lack of confidence in their security strategy. For FinTechs, this isn't just a sales inconvenience—it's a fundamental business barrier. This guide covers the most common SOC 2 readiness gaps, how to find them systematically, and a prioritized approach to closing them before auditors arrive—so compliance becomes a deal-maker, not a blocker.

TLDR:

- Gap analysis catches control deficiencies before formal audits cause qualified opinions or deal delays

- Access controls, stale policies, and weak vendor management are the most common early-stage failures

- Systematic readiness assessment follows 5 steps: scope, asset inventory, control mapping, risk ranking, and documentation

- Most remediation timelines run 3–6 months; unresolved gaps stall enterprise sales and sponsor bank relationships

- Fractional compliance leadership delivers director-level expertise to own the remediation roadmap without a full-time hire

What Is a SOC 2 Gap Analysis (and Why Should FinTech Companies Care)?

A SOC 2 gap analysis measures your organization's current security controls against the Trust Services Criteria (TSC)—Security, Availability, Processing Integrity, Confidentiality, and Privacy—to identify specific deficiencies before an official audit. Security is the only mandatory criterion; additional criteria are selected based on your service commitments and what you promise customers.

For FinTechs, that definition carries real commercial weight — here's why the stakes are higher than for most technology companies.

Why FinTech Companies Face Heightened Scrutiny

Unlike generic tech startups, FinTechs handling payment data, customer financial records, or cryptocurrency assets operate under intense regulatory and partner scrutiny. The 2023 Interagency Guidance on Third-Party Relationships advises banking organizations to review SOC reports during vendor due diligence. For companies managing sponsor bank relationships, unaddressed SOC 2 gaps become deal-breakers, not audit inconveniences.

Key business drivers:

- 65% of organizations report customers, investors, and suppliers increasingly require proof of compliance

- Enterprise procurement now involves 6-10 stakeholders, with B2B decision timelines increasing by 54 days between 2021 and 2024

- Half of businesses have ended vendor relationships due to security concerns

Gap Analysis vs. Formal Audit: Critical Distinction

A gap analysis is a pre-audit diagnostic with no formal attestation output. Its value lies in giving you time to remediate before auditors arrive, rather than discovering deficiencies during the examination itself.

Done well, a gap analysis delivers three concrete advantages before your auditor walks in:

- Prevents qualified opinions by surfacing control failures early

- Reduces audit costs by limiting the scope of remediation work

- Accelerates time-to-certification with a clear remediation roadmap

The Most Common Gaps Found in SOC 2 Readiness Assessments

While every organization's control environment differs, certain gaps consistently surface—especially in early-stage and high-growth companies. The following are the most frequently cited findings and what remediation typically involves.

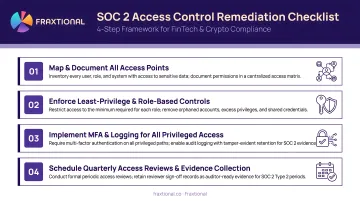

Access Controls and User Provisioning Failures

This is the most common gap across organizations. Excessive access privileges, missing multi-factor authentication (MFA), and inadequate user provisioning and deprovisioning processes plague early-stage companies. Particularly problematic: contractors, temporary employees, and former staff who retain system access after termination.

By the numbers:

- System Access exceptions represent 17% of all control exceptions noted during audits

- Over 99.9% of compromised accounts lack MFA protection

- MFA adoption in finance and banking reached only 60% in 2023

Auditors specifically look for evidence that the principle of least privilege is enforced. The AICPA Trust Services Criteria explicitly requires this under CC6.3: "The entity authorizes, modifies, or removes access to data, software, functions, and other protected information assets based on roles, responsibilities, or the system design and changes."

Remediation essentials:

- Formalize an access provisioning policy that defines who can grant access and under what conditions

- Implement MFA across all critical systems (no exceptions)

- Establish a documented offboarding checklist with defined timelines for access revocation

- Conduct quarterly user access reviews for privileged accounts, annually for all users

Missing or Outdated Security Policies and Procedures

Auditors examine whether written policies exist and whether they've been reviewed and updated within the past year. Many organizations discover they have no formal policies for critical areas—incident response, acceptable use, data classification, or business continuity.

Others have policies on paper that haven't been reviewed since the company was founded.

According to KPMG's Controls Assurance Benchmarking Report, 89% of all exceptions noted on tests of operating effectiveness were manually operated controls, with Management Review controls accounting for 30% of exceptions.

Remediation requirements:

- Draft, approve, and distribute policies mapped to applicable TSC criteria

- Establish an annual review cycle with documented sign-off from responsible personnel

- Ensure policies reflect current operations, not aspirational or outdated processes

- Track policy acknowledgment from all employees with signed records

Inadequate Third-Party and Vendor Risk Management

For FinTechs with complex vendor ecosystems—payment processors, cloud infrastructure providers, identity verification vendors, sponsor bank partners—the absence of a formal vendor risk management program is a critical gap. 30% of breaches in 2025 were linked to third-party involvement.

During vendor risk reviews, auditors look for:

- Vendor inventories (complete and current)

- Tiering models (risk-based classification)

- Contractual security requirements (in signed agreements)

- Periodic review of vendor SOC reports (annual minimum)

Remediation approach:

- Build a comprehensive vendor inventory

- Assign a risk tier to each vendor based on data access and criticality

- Define review frequencies based on tier (quarterly for high-risk, annually for low-risk)

- Embed security clauses into contracts before execution

- Track third-party SOC reports annually and maintain evidence of review

Change Management and Segregation of Duties Gaps

Many early-stage companies lack formal change management controls. Developers push changes directly to production without independent approval or testing, violating segregation of duties (SoD) requirements. This is especially common at small companies where teams are lean, but auditors still expect documented processes—even lightweight ones.

What auditors expect:

- Change request documentation (who requested, what changed, why)

- Independent approval (someone other than the developer)

- Testing evidence (proof the change was validated before deployment)

- Deployment records (who deployed, when, and confirmation of success)

Remediation steps:

- Implement a change management workflow (even a simple ticketing system)

- Define distinct roles for developers versus deployers

- Document each step of the change lifecycle with approver, tester, and deployment date

- Maintain a change log that can be audited retrospectively

Insufficient Logging, Monitoring, and Incident Response

Organizations frequently lack comprehensive logging coverage across critical systems and have no defined process for reviewing logs for anomalies. Many also have no documented or tested incident response plan—and auditors flag the absence of a tabletop exercise as a consistent remediation item.

What closing this gap requires:

- Centralized log management with defined retention periods (typically 90 days minimum)

- Alert thresholds and review responsibilities (who monitors, how often)

- Documented incident response plan with clear roles and escalation paths

- Evidence of testing (tabletop exercise at minimum annually)

Weak Security Awareness Training and Personnel Offboarding

Inconsistent or undocumented security training is a persistent finding, particularly at fast-growing companies where onboarding processes haven't kept pace with headcount. Similarly, the lack of a formalized offboarding process—especially for contractors—creates access control gaps that directly map to TSC requirements.

Both training and offboarding must be documented with evidence of completion—performing them without a paper trail won't satisfy auditors.

Remediation requirements:

- Implement mandatory security awareness training at onboarding and annually thereafter

- Track completion with signed acknowledgment records

- Build a structured offboarding checklist that ties HR, IT, and security responsibilities together

- Define timelines (access revocation within 24 hours of termination, equipment return within 5 business days)

How to Conduct a SOC 2 Gap Assessment: A Step-by-Step Approach

Step 1 — Define Scope Before Anything Else

Determine which Trust Services Criteria apply to your organization based on the services you provide and commitments made to customers. Scoping errors at this stage lead to over-engineering (assessing irrelevant criteria) or under-engineering (missing applicable criteria), and either outcome creates problems when the audit begins.

Scoping considerations:

- Security is mandatory for every SOC 2 audit

- Availability applies if you guarantee uptime SLAs

- Processing Integrity applies if you process financial transactions or calculations

- Confidentiality applies if you handle customer proprietary information

- Privacy applies if you collect personal information and commit to specific handling practices

Step 2 — Build Your Asset and Data Inventory

Document what data your organization processes, where it lives, how it moves through your systems, and who has authorized access. For FinTechs, that means mapping payment data flows, customer PII handling, and data shared with banking partners or subprocessors.

Essential inventory elements:

- Data classification schema (public, internal, confidential, restricted)

- System inventory (all applications and infrastructure)

- Data flow diagrams (how sensitive data moves between systems)

- Access authorization matrix (who can access what, and why)

Step 3 — Map Existing Controls to TSC Requirements

With your inventory in hand, compare each applicable criterion against controls currently in place. Identify which criteria are fully met, which are partially met, and which have no corresponding control. This mapping exercise reveals the gap landscape and forms the foundation of your remediation plan.

Mapping approach:

- Review each TSC criterion and its points of focus

- Document the specific control (if any) that addresses it

- Rate control effectiveness (effective, partially effective, not implemented)

- Capture evidence of control operation (or note its absence)

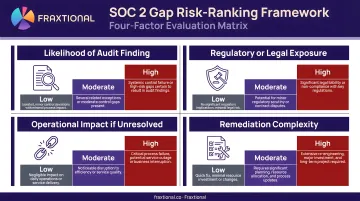

Step 4 — Risk-Rank Identified Gaps

Once gaps are mapped, not all of them demand equal urgency. Evaluate each gap against business impact, likelihood of exploitation, and remediation complexity — then sequence your remediation around the highest-risk findings, not the easiest ones.

Use this framework to rank each gap:

| Factor | Key Question |

|---|---|

| Severity | Could this gap lead to a data breach or regulatory violation? |

| Likelihood | How easily could this gap be exploited? |

| Business Impact | Would this gap cause audit failure or deal delays? |

| Remediation Effort | How quickly and easily can this be fixed? |

Step 5 — Document Findings and Build an Evidence Baseline

Capture all assessment findings in a structured format that directly feeds your remediation plan. At the same time, start organizing existing evidence for controls that are already functioning — doing this now significantly reduces the collection burden when the formal audit period begins.

Documentation best practices:

- Create a gap register with owner, priority, and target date for each finding

- Organize existing control evidence by TSC criterion

- Establish a central repository for audit evidence

- Track remediation progress against the gap register

Closing the Gaps: Building Your Remediation Plan

A remediation plan converts each gap into a specific action, owner, deadline, and success metric. Sequence remediation by risk priority — tackle high-risk gaps first, ordered by dependencies — rather than addressing everything simultaneously. Attempting too much at once overwhelms teams and increases the chance of poorly implemented controls.

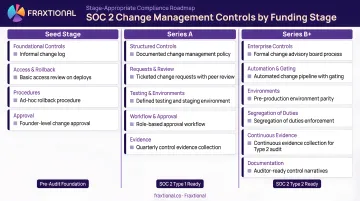

Implementing Stage-Appropriate Controls

A 15-person seed-stage startup needs different control implementations than a 200-person Series B company. The goal is not to build a compliance program designed for an enterprise, but to implement controls that are proportionate, defensible, and scalable. Auditors assess whether controls are fit-for-purpose for the organization's size and maturity.

Stage-appropriate examples:

- Seed-stage: Simple change management via GitHub pull request reviews may suffice

- Series A: Ticketing system (Jira, Linear) with approval workflows becomes appropriate

- Series B: Dedicated change advisory board with formal CAB meetings may be required

The Fractional Compliance Leadership Model

Once you know what controls to build, the harder question is who owns the work. For early-stage FinTech companies without a full-time compliance officer, a fractional compliance leader — such as those Fraxtional provides — gives organizations director-level expertise to own the remediation roadmap, advise on control design, and liaise with auditors, without the cost of a full-time hire.

Key advantages:

- Director personally owns the remediation roadmap and interfaces directly with auditing CPA firms

- Embedded model — attends meetings and represents your business to auditors and regulators

- Officially named as your CCO in regulatory filings, audits, and contracts

- Delivers stage-appropriate control guidance that scales as the business grows

Continuous Monitoring After Initial Remediation

Remediation closes the gaps you found today — it doesn't prevent new ones from opening. Controls must be reviewed and tested on an ongoing basis as the organization scales, its technology stack evolves, and new regulatory requirements emerge. SOC 2 is an annual report, and gaps can re-emerge between audit cycles without an active monitoring program.

Monitoring requirements:

- Quarterly control testing for critical controls

- Annual control testing for all other controls

- Continuous log monitoring and alerting

- Annual policy review and update cycle

- Triggered assessments when significant changes occur (new systems, acquisitions, major vendor changes)

What Happens If SOC 2 Gaps Go Unaddressed?

Business Consequences

Enterprise sales cycles stall when security questionnaires surface unanswered risks. Sponsor banks and financial institution partners may withdraw or delay partnerships when due diligence reveals control deficiencies. Investors conducting pre-deal security reviews increasingly expect SOC 2 readiness as a baseline for Series A and beyond.

Real-world impact:

- 77% of B2B buyers describe their purchase experience as extremely complex, with risk aversion driving defensive decision-making

- 43% of B2B buyers make defensive purchase decisions more than 70% of the time

- 80% of sponsor banks find meeting compliance requirements challenging, and 39% lost at least $250,000 due to compliance violations

Audit Consequences

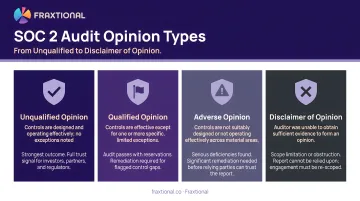

Gaps discovered during a formal SOC 2 examination result in qualified opinions or noted exceptions in the final report, which are visible to every customer or partner who reads it. Remediating post-audit is far more costly and reputationally damaging than addressing gaps proactively.

Audit opinion types:

- Unqualified: Controls were designed and operating effectively

- Qualified: Issues identified were significant enough to deem one or more controls ineffective

- Adverse: Material deficiency is pervasive; users cannot rely on the service organization's system

- Disclaimer: Auditor unable to issue an opinion due to limitations

Broader Security Benefit

The security improvements that come from SOC 2 remediation extend well beyond the audit itself. Closing gaps in access control, vendor oversight, and monitoring reduces real exposure — data breaches, insider threats, and operational failures that cost companies far more than any compliance program.

Financial cost of inaction:

- Average cost of a data breach in financial services: $5.56 million in 2025

- Global average cost: $4.44 million

- United States leads all countries at $10.22 million per breach

- 88% of basic web application attacks involved stolen credentials

Frequently Asked Questions

Frequently Asked Questions

What is a gap analysis in SOC?

A SOC 2 gap analysis is a preliminary assessment that compares an organization's current security controls and processes against the Trust Services Criteria requirements, identifying deficiencies that must be remediated before a formal SOC 2 audit can result in a clean opinion.

What is the difference between a SOC 2 gap analysis and a SOC 2 audit?

A gap analysis is an internal or advisory exercise that produces no official attestation — it's designed to prepare the organization for audit. A SOC 2 audit is a formal examination conducted by an independent CPA firm that results in an official report shared with customers and partners.

How long does it take to close SOC 2 readiness gaps?

Remediation timelines vary widely by gap type and organizational maturity. Policy gaps can often be closed in weeks, while technical control gaps or vendor management programs may take several months to build and evidence. Most organizations preparing for their first SOC 2 should plan for 3-6 months of remediation time before beginning the audit period.

Can a startup conduct a SOC 2 gap analysis on its own?

While internal self-assessments are possible, they carry significant risk of blind spots and missed requirements. Many early-stage startups benefit from engaging a third-party advisor or fractional compliance leader with SOC 2-specific expertise — someone who knows what auditors actually look for.

How often should a SOC 2 gap analysis be performed?

Gap assessments should be performed at least annually, aligned with SOC 2 report renewal cycles. They should also be triggered by significant organizational changes — new product lines, infrastructure migrations, new vendor relationships, or significant headcount changes — that may introduce new control gaps.