Introduction

Any business engaged in money transmission in Alaska must hold an Alaska Money Transmitter License (ALMTL), issued by the Division of Banking and Securities (DBS). Since January 2023, this requirement explicitly extends to virtual currency businesses under the Alaska Uniform Money Transmission Modernization Act.

The licensing process is document-intensive and multi-step. Incomplete applications or missing documents can push approval timelines back by months, so understanding requirements upfront matters.

Crypto businesses face the steepest requirements. Cryptocurrency exchanges, wallet providers, and crypto ATM operators must meet a $500,000 surety bond — compared to the $25,000 base bond for standard money transmitters.

This guide covers:

- Who needs an Alaska Money Transmitter License

- Document and bonding requirements

- The step-by-step application process

- Timelines, fees, and common delays

Key Takeaways

- Alaska's money transmitter license is required for transmitting money or virtual currency; file via NMLS

- Minimum net worth of $25,000, electronic surety bond starting at $25,000 (or $500,000 for virtual currency firms), and FinCEN registration required

- Typical processing time is 120 days after a complete application is submitted

- Expect annual renewals with quarterly reporting and strict AML/BSA compliance obligations

- Virtual currency businesses must confirm their license scope explicitly covers crypto activities — a common gap that triggers enforcement

What Is the Alaska Money Transmitter License?

The ALMTL is a state-level regulatory authorization issued by the Alaska Division of Banking and Securities under AS 06.55 (Alaska Uniform Money Transmission Modernization Act). It permits businesses to engage in money transmission activities within or from Alaska.

Activities Authorized Under the License

The license covers a broad range of money transmission activities:

- Electronic money transmitting

- Issuing or selling money orders and traveler's checks

- Prepaid access and stored value products

- Foreign currency exchange

- Bill payment services

- Cryptocurrency dealing, exchanging, and custodial services

- Crypto ATMs and kiosks (also called Bitcoin ATMs or BTMs)

Since January 2023, cryptocurrency-related activities moved from a limited licensing framework to full money transmitter licensure, bringing previously unregulated crypto firms under the same prudential standards as traditional money transmitters.

How This Differs from a Business Registration

The ALMTL is not a one-time approval. It carries ongoing prudential obligations that stay with you for the life of the license:

- Minimum net worth requirements

- Surety bond posting

- Permissible investments equal to outstanding obligations

- AML/BSA compliance programs

- Periodic reporting to the DBS

This makes the ALMTL a continuous regulatory commitment — one that requires active compliance infrastructure to maintain in good standing.

Who Needs an Alaska Money Transmitter License?

Any person or entity engaging in "money transmission" as defined under AS 06.55.990 must be licensed. This includes receiving money for transmission, selling payment instruments, issuing stored value, and — since January 2023 — conducting virtual-currency business activity unless explicitly exempt.

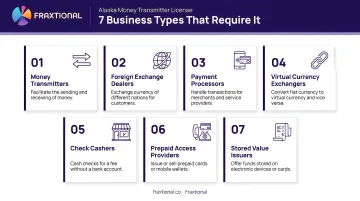

Primary Business Types Requiring Licensure

The following business models require the ALMTL:

- Fintech payment platforms facilitating transfers between consumers or businesses

- Remittance services sending money across state or national borders

- Crypto exchanges and wallet providers offering buy/sell or custody services

- Crypto ATM operators enabling cash-to-crypto or crypto-to-cash conversions

- Prepaid card issuers providing stored value or reloadable payment cards

- Payroll processors transmitting employee wages on behalf of employers

- Foreign currency exchange businesses buying or selling currencies

The 2023 expansion brought previously unregulated crypto firms under this requirement, ending the Limited License Agreement (LLA) era for virtual currency businesses.

Authorized Delegates and Third-Party Agents

Using third-party agents doesn't transfer licensing responsibility — the license holder remains accountable for every transaction their delegates conduct. Alaska statute requires written contracts with each authorized delegate, along with written policies to ensure ongoing compliance on their part.

Important: Outside counsel and consultants cannot serve as primary contacts under the DBS application. The Primary Company Contact must be an actual employee of the applicant.

Key Requirements to Qualify for an Alaska Money Transmitter License

Net Worth

The minimum tangible net worth requirement is $25,000 under GAAP. AS 06.55.506 then adds tiered thresholds based on total assets:

- $100,000 or 3% of total assets (whichever is greater) for the first $100 million in total assets

- Additional net worth requirements apply as total assets increase

Startups and established firms alike must document this net worth through CPA-prepared audited financial statements.

Surety Bond

The electronic surety bond requirement varies significantly by business type:

Standard Money Transmitters:

- $25,000 base bond

- Plus $5,000 for each additional location (branches, internet portals, mobile apps, authorized delegate locations)

- Maximum cap of $150,000

Virtual Currency Applicants:

- $500,000 electronic surety bond required under AS 06.55.104(f) — reflecting DBS's stricter stance on cryptocurrency volatility and consumer protection

All surety bonds must be electronic (submitted through NMLS) and issued by an Alaska-authorized surety company.

Financial Statements

CPA-prepared audited financial statements (GAAP-compliant) must cover:

- The most recent fiscal year

- Up to two prior fiscal years (if available)

- Balance sheet, income statement, and statement of cash flows

Startups without prior fiscal year financials must provide:

- An initial statement of condition

- Documentation of capitalization sources

These statements must demonstrate the required minimum net worth and financial stability.

AML/BSA Policy and Compliance Infrastructure

The DBS requires three core compliance documents:

- Board-approved AML/BSA policy covering customer due diligence, transaction monitoring, and suspicious activity reporting procedures

- Independent review of the AML/BSA program conducted by a qualified third party

- Information Security Policy addressing breach handling under AS 45.48.010–090

For early-stage companies without in-house compliance staff, a fractional BSA Officer — like those Fraxtional places — can build and own this program from day one, audit-ready and DBS-compliant.

FinCEN Registration and Background Requirements

Every applicant must satisfy the following federal and individual-level requirements:

- Be registered with FinCEN as a Money Services Business (MSB) under 31 USC 5330

- Provide their FinCEN registration number and authorization date

- Complete MU2 individual forms for all control persons

- Submit to credit report authorization via NMLS

- Provide criminal background checks from all relevant countries (for foreign nationals or individuals who lived outside the US in the past 10 years), translated into English

- Authorize identity verification (IDV) and credit reports through NMLS at $15 per control person

How to Apply for an Alaska Money Transmitter License: Step-by-Step

Applications are submitted through the Nationwide Multistate Licensing System (NMLS). Alaska does not issue paper licenses. Processing begins only when all required documents and fees are received, with a typical review period of approximately 120 days.

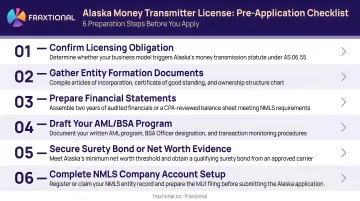

Step 1: Pre-Application Preparation

Before opening your NMLS application, gather and complete:

- Alaska Business License from the Department of Commerce, Community, and Economic Development (CBPL)

- Registered agent appointed and registered in Alaska

- Audited financial statements prepared by a CPA

- Business plan and separate flow of funds document

- AML/BSA policy approved by your board of directors

- Electronic surety bond through an Alaska-authorized surety company

This phase typically takes 2–3 months for well-capitalized startups. It can run 4–6 months for firms that still need to draft AML/BSA policies, appoint a compliance officer, or restructure ownership documentation.

Step 2: Complete and Submit NMLS Forms

Submit the following through NMLS:

Company Form (MU1):

- Financial statements and bank account details

- FinCEN registration information

- Authorized agent reporting setup (UAAR) — required if using authorized delegates

- Disclosure questions with supporting documentation

Individual Forms (MU2):

- One form for each control person

- Identity verification (IDV) completion

- Credit report authorization

Critical: DBS rejects generic email addresses for contacts. Use individual employee email addresses for all contact points.

Step 3: Upload Supporting Documents and Pay Fees

Upload all required documents in NMLS:

- Formation documents (articles of incorporation, operating agreements)

- Certificate of Good Standing from CBPL

- Alaska Business Affidavit (digitally or physically signed — mixed signatures invalidate the form)

- Management chart showing individual names, titles, and compliance reporting structure

- Organizational chart with direct and indirect ownership percentages

- Flow of funds structure (separate from your business plan)

- Trade name registrations (if applicable)

Fees payable through NMLS:

| Fee Type | Amount |

|---|---|

| Application fee | $2,000 |

| License fee | $1,000 |

| NMLS initial processing fee | $120 |

| Credit report per control person | $15 |

All fees paid through NMLS are non-refundable.

Step 4: Respond to Regulator Inquiries and Await Decision

Once submitted, DBS may issue requests for additional information. Response time matters — slow replies extend your timeline. Designate a Primary Company Contact who is an actual employee, not outside counsel, and who can respond promptly to regulator questions.

If your company holds licenses in other states, there's a potential shortcut: under AS 06.55.110, DBS can accept investigation results from a lead state in multistate licensing processes. This can meaningfully reduce review time for businesses already licensed elsewhere.

Costs, Fees, and Renewal Obligations

All Fees Associated with the ALMTL

Initial Application:

- $2,000 application fee

- $1,000 license fee

- $120 NMLS initial processing fee

- $15 per control person for credit reports

- Surety bond costs: $25,000 base (or $500,000 for virtual currency)

Ongoing Annual Fees:

- Uniform Authorized Agent Reporting (UAAR) fee: $0.25 per active agent location

- First 100 agents are free

- Maximum annual UAAR fee: $25,000 per licensee

The DBS invoices UAAR fees through NMLS each November 1, based on the number of active agents in the system as of August 16.

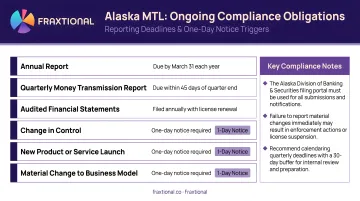

Annual Renewal Requirements

Licenses are issued for one year and must be renewed annually. Licensees must continue meeting all qualifications applicable to new applicants, including:

Quarterly Reports:

- Report of condition covering the licensee's own activities and those of authorized delegates

- Due within 45 days after the end of each quarter

- MSB Call Report (Sections I, II, III) due to FinCEN 45 days after each quarter

Annual Submissions:

- Audited financial statements within 90 days after fiscal year end

- Ongoing demonstration of permissible investments equal to outstanding money transmission obligations

Ongoing Compliance Obligations Post-Licensure

Renewal keeps your license active — but these standing requirements apply year-round, regardless of reporting cycles.

Licensees must maintain:

- Records for a minimum of 5 years (increased from 3 years under the updated model law)

- Permissible investments equal to outstanding money transmission obligations

- OFAC screening, US Patriot Act compliance, and full BSA program requirements

Certain events also require reporting to the DBS within one business day:

- Bankruptcy filings or reorganization proceedings

- License actions in other states

- Bond cancellations or impairment

- Felony charges against the licensee, executive officers, managers, directors, persons in control, or authorized delegates

Failure to maintain these standards can result in license suspension or revocation under AS 06.55.108.

Exemptions and Common Misconceptions

Key Exemptions Under Alaska Law

Exemptions under AS 06.55.802 and AS 06.55.205:

- Low-volume virtual currency businesses: Persons whose virtual-currency business activity is expected to be $5,000 or less annually (measured in dollar equivalent)

- Insurance and title companies: When money transmission is ancillary to their primary business

- Attorneys: Providing money transmission as an ancillary service to the practice of law

- Employees of licensees: Acting within authorized scope

- Agents of payees: In certain defined circumstances

- DBS discretionary exemptions: The DBS can grant additional exemptions "in the public interest" and may require supporting documentation from anyone claiming an exemption

Three Common Misconceptions

A general Alaska business license is sufficient. The ALMTL is a separate, more rigorous authorization with its own prudential standards, bonding requirements, and ongoing compliance obligations. A basic CBPL business license does not permit money transmission.

Pre-2023 crypto Limited License Agreements (LLAs) still cover operations. LLAs were voided effective January 1, 2023. Businesses must now hold a full ALMTL that explicitly covers virtual currency activities.

Multistate licensing automatically satisfies Alaska's requirements. Alaska has its own checklist and prerequisites. While the DBS may accept lead-state investigation results under AS 06.55.110, you must still satisfy Alaska-specific requirements — registered agent, Alaska business license, and state-specific forms.

Virtual Currency Asset Protection

These misconceptions matter most for crypto operators, where the stakes extend beyond licensing to customer asset safety. Under AS 06.55.208, customer virtual currency interests take priority over the licensee's creditors. The Alaska MTL also prohibits rehypothecation (using customer crypto holdings as collateral for the licensee's own obligations). Alaska law treats these assets as customer property held in trust — not as licensee assets.

Frequently Asked Questions

What is an Alaska money transmitter license?

A state-issued license from Alaska's Division of Banking and Securities (DBS), it authorizes businesses to legally conduct money transmission — including virtual currency activities — in Alaska under AS 06.55, the Alaska Uniform Money Transmission Modernization Act.

What qualifies as a money transmitter in Alaska?

Activities include receiving money for transmission, selling payment instruments, issuing stored value, and conducting virtual-currency business activity — all as defined under AS 06.55.990 — unless an exemption applies under state law.

What is the Alaska Money Transmission Act?

AS 06.55 — now called the Alaska Uniform Money Transmission Modernization Act — was updated by Senate Bill 238 to align with the CSBS model law and add virtual currency to money transmission definitions, effective January 2023.

How much does an Alaska money transmitter license cost?

Base fees total $3,120: a $2,000 application fee, $1,000 license fee, and $120 NMLS processing fee. Surety bond requirements start at $25,000 for standard transmitters and $500,000 for virtual currency businesses, plus ongoing annual renewal and reporting fees.

How do I renew my Alaska money transmitter license?

Renewals are filed annually through NMLS and require continued compliance with licensure qualifications, quarterly reports of condition, and an annual audited financial statement. DBS invoices Uniform Authorized Agent Reporting (UAAR) fees through NMLS each November.