Introduction

On January 1, 2025, Massachusetts rewrote its money transmission rules entirely. Governor Maura Healey signed House Bill 4840 (Chapter 312 of the Acts of 2024) into law, replacing the prior Chapter 169—which only covered foreign remittance—with a comprehensive framework that now applies to both domestic and international money transmission to consumers.

Who this guide is for: FinTech startups, crypto companies, payment platforms, embedded finance businesses, and remittance services that serve Massachusetts residents. If you're unsure whether your business model triggers licensing requirements, this guide clarifies exactly where the new law draws the line.

What you'll learn:

- What the Massachusetts Money Transmitter License covers under the new law

- Who needs a license — and who qualifies for an exemption

- Exact application requirements and supporting documents

- How to file through NMLS

- Ongoing compliance obligations after approval

Key Takeaways

- Massachusetts expanded its money transmission rules in 2025 to cover both domestic and foreign consumer transactions

- Minimum requirements: $100,000 surety bond, permissible investments equal to outstanding obligations, tiered net worth formula

- Key exemptions include agents of payees, intermediary processors, and service providers to federally exempt institutions

- All applications go through NMLS — transitional applicants who filed by July 2025 are permitted to operate pending approval

- Ongoing compliance covers quarterly and annual reporting, transaction receipts, and change-of-control notices

What Is the Massachusetts Money Transmitter License?

The Massachusetts Money Transmitter License is a state-issued authorization from the Massachusetts Division of Banks (MDOB) permitting businesses to sell or issue payment instruments, sell or issue stored value, or receive money for transmission from Massachusetts consumers.

Legal Framework and MTMA Adoption

Chapter 312 of the Acts of 2024 replaced the prior Chapter 169 framework, which only covered foreign money transmission. The new M.G.L. c. 169B aligns Massachusetts with the model Money Transmission Modernization Act (MTMA) developed by the Conference of State Bank Supervisors, making Massachusetts one of the more recent states to adopt a unified domestic and international money transmission framework.

The Consumer-Only Restriction

Unlike most state money transmission laws, Massachusetts applies its licensing requirement exclusively to consumer transactions—those conducted for personal, family, or household purposes. The statute explicitly excludes commercial transactions between businesses from the definition of money transmission.

A payment processor handling only B2B transactions may not need a Massachusetts license. A platform serving both consumers and businesses, however, must carefully evaluate which portions of its operations fall within scope — Massachusetts is one of a handful of states with this restriction, and the line matters for multi-sided platforms and embedded finance companies alike.

Who Needs a Massachusetts Money Transmitter License?

Expanded Scope Under the New Law

Under M.G.L. c. 169B, any person or entity that engages in the following activities with Massachusetts consumers now requires a license:

- Selling or issuing payment instruments (checks, money orders, electronic payment instruments)

- Selling or issuing stored value (prepaid cards, digital wallets, reloadable accounts)

- Receiving money for transmission (remittance, P2P payments, cross-border transfers)

These activities capture a wide range of business models. The following types typically fall within scope:

- Consumer-facing payment apps

- Digital wallet providers

- Remittance and money transfer services

- Stored value and prepaid card issuers

- Peer-to-peer payment platforms

- FinTech platforms offering money movement to retail users

One important wrinkle: the law applies only to consumer transactions. Determining whether activity is "consumer" versus "commercial" is fact-specific and requires careful legal review. A platform collecting rent from tenants operates differently than one processing wholesale invoices between businesses — and mixed-use platforms need to evaluate each transaction flow separately.

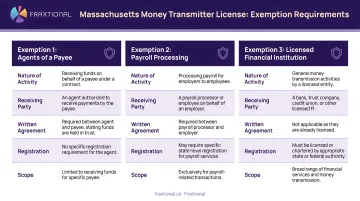

Three Primary Exemptions

M.G.L. c. 169B § 2 provides specific exemptions, each with strict qualifying conditions:

| Exemption | Requirements |

|---|---|

| Agent of a Payee | Written agreement to collect/process payments; payee publicly identifies agent as accepting payments; payment extinguishes payor's obligation upon agent receipt |

| Intermediary Processor | Processes payments between a licensed/exempt entity and designated recipient; the entity with direct obligation provides transaction receipts and bears full responsibility |

| Third-Party Service Provider | Written appointment by an exempt financial institution; the exempt entity assumes all risk of loss and legal responsibility |

Additional automatic exemptions: Federally insured depository institutions, bank holding companies, registered broker-dealers, government entities, and the U.S. Postal Service are exempt. The Massachusetts Commissioner of Banks retains discretionary authority to grant additional exemptions where doing so serves the public interest.

Claiming any exemption requires strict adherence to its specific contractual and operational conditions — the MDOB can and does request documentation to verify qualification.

Key Requirements for the Massachusetts Money Transmitter License

Surety Bond

Licensees must maintain a surety bond equal to the greater of $100,000 or 100% of the licensee's average daily money transmission liability in Massachusetts calculated over the most recently completed 3-month period, capped at $500,000.

This is a significant increase from the prior $50,000 minimum under Chapter 169. The bond must be maintained as a condition of licensure and obtained from an authorized surety company meeting Massachusetts' requirements.

Permissible Investments

M.G.L. c. 169B § 9(c) requires licensees to maintain permissible investments with a market value equal to or greater than all outstanding money transmission obligations—a liquidity safeguard ensuring consumer funds remain protected.

Qualifying permissible investments include:

- Cash and demand deposits in FDIC-insured institutions

- Certificates of deposit in federally insured institutions

- Government obligations (U.S. Treasury securities, state/municipal bonds)

- AAA-rated money market mutual funds

- Receivables from authorized delegates (≤7 days old, capped at 50% of total investments, single delegate max 10%)

- Short-term eligible-rated investments (≤6 months, capped at 20% per category, 50% combined)

- Irrevocable standby letters of credit (Commissioner as beneficiary)

- Surety bond amounts exceeding average daily liability

Tangible Net Worth

Licensees must maintain tangible net worth (total assets excluding intangibles) equal to the greater of $100,000 or a tiered formula based on total assets:

- 3% of the first $100,000,000 in total assets

- 2% of assets between $100,000,000 and $1,000,000,000

- 0.5% of assets exceeding $1,000,000,000

Example: A licensee with $150,000,000 in total assets must maintain tangible net worth of at least $4,000,000 ($3,000,000 for the first $100M + $1,000,000 for the additional $50M).

Key Application Documents

Applications through NMLS typically require:

- Business formation documents (articles of incorporation, operating agreements)

- Audited financial statements for the most recent fiscal year

- Business plan detailing target markets, products, and transaction volumes

- Comprehensive AML/BSA compliance program

- Background checks and fingerprints for all control persons and key individuals

- Organizational charts showing ownership structure and management hierarchy

- State-specific disclosures required by MDOB

Each of these documents signals to MDOB that your compliance infrastructure is built—not bolted on. Fraxtional's fractional compliance leadership, including named CCOs and BSA Officers, helps companies build AML programs and prepare application packages that meet the quality and completeness regulators expect, including frameworks that satisfy sponsor bank and investor due diligence.

How to Apply for a Massachusetts Money Transmitter License

All applications are submitted through the Nationwide Multistate Licensing System (NMLS), allowing companies already licensed in other states to streamline multi-state filings.

Step 1: Create or Log In to Your NMLS Account

Register or access your existing account at the NMLS Consumer Access portal, then complete the following:

- File the Company Form (MU1) to create your company record

- Have all control persons (owners with 10%+ equity, officers, directors) complete Individual Forms (MU2)

- Submit background checks and FBI fingerprinting for each control person

Step 2: Complete the Massachusetts-Specific Application and Upload Documents

Select Massachusetts as your license state within NMLS, complete all required form fields, and upload required documentation:

- Financial statements (audited)

- Business plan

- AML/BSA compliance policies and procedures

- Organizational documents

- State-specific disclosures required by MDOB

Verify the current NMLS Massachusetts checklist for completeness requirements, as document expectations may be updated by regulators.

Step 3: Obtain and Upload the Surety Bond

Secure and upload your surety bond through NMLS:

- Source the bond from an authorized surety company meeting Massachusetts' requirements

- Confirm the bond amount meets the $100,000 minimum — higher amounts may apply based on average daily transmission volume

- Expect bond premiums to vary based on creditworthiness and transaction volume

Step 4: Pay Filing Fees and Submit

Current Massachusetts NMLS filing fees:

| Fee Type | Amount |

|---|---|

| MA License Fee | $1,000 |

| MA Investigation Fee | $300 |

| NMLS Company Set-up Fee | $120 |

| FBI Background Check (per person) | $36.25 |

| Credit Report (per person) | $15.00 |

Total state fees are $1,300, plus NMLS processing fees and per-person background checks. After payment, review your submission for completeness and submit through the NMLS portal.

Step 5: Respond to MDOB Review and Await Decision

After submission, the Massachusetts Division of Banks reviews your application. Expect deficiency notices or requests for additional information — respond promptly to avoid delays.

Key dates and timeline considerations:

- Transitional provision: Businesses newly required under Chapter 169B (not previously licensed under Chapter 169) had until July 1, 2026 to file. Those who submitted complete applications by the deadline may continue operating during review.

- Application window: MDOB began accepting applications July 1, 2025, with licensing and regulation taking effect January 1, 2026.

- Review timeline: Neither MDOB nor NMLS publishes guaranteed processing timeframes. Plan for several months of review — responsiveness to regulator inquiries is the biggest variable.

Ongoing Compliance Obligations After Licensure

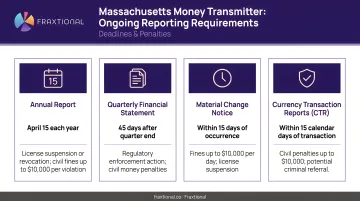

Reporting Requirements

Massachusetts imposes strict periodic reporting obligations. The four core reports — each with firm deadlines — are:

| Report | Deadline | Key Notes |

|---|---|---|

| Quarterly Report of Condition | 45 days after quarter-end | Includes financial data, nationwide and MA transaction volume, and permissible investments. Destination country reporting required in Q4 only. |

| Annual Audited Financials | 90 days after fiscal year-end | Full audited financial statements |

| Annual Report | Date set by the Commissioner | Late filing triggers a $50-per-day penalty |

| Change Notices | Prompt / as required | Required for criminal convictions of officers or delegates, regulatory actions in other states, changes to application information, and authorized delegate updates |

Transaction-Level Requirements

Beyond periodic reporting, licensees must meet specific requirements at the individual transaction level.

Refunds: Licensees must refund money within 10 days of a valid written request, unless the money was already forwarded, instructions were given committing the funds, or the transaction is suspected of fraud or criminal activity.

Transaction Receipts: M.G.L. c. 169B § 8(c) mandates receipts include:

- Sender name

- Designated recipient

- Transaction date

- Unique transaction identifier

- Licensee name, business address, and customer service phone number

- NMLS Unique Identifier

- USD amount

- Fees charged

- Taxes collected

Change of Control and License Maintenance

Managing ownership changes and keeping your license in good standing are equally ongoing obligations.

Key requirements include:

- Anyone seeking to acquire control of a licensee must file notice with the Commissioner before completing the acquisition

- Adding or replacing a "key individual" requires notice within 15 days of appointment

- Maintain the required surety bond and permissible investments on an ongoing basis

- Renew your license on schedule through NMLS renewal cycles

- Businesses that previously held Chapter 169 licenses (Foreign Transmittal Agencies) transitioned to the new framework by filing renewal/transition requests through NMLS starting November 1, 2025

Common Mistakes and Misconceptions

Assuming the Old Exemption Still Applies

Many businesses exempt under Chapter 169—which only regulated foreign remittance—are now in scope under Chapter 312. Domestic consumer payment activities that previously operated without licensing now require authorization. Failing to reassess your obligations under the new law creates compliance risk that regulators will scrutinize.

Misreading the Consumer-Only Carve-Out

A common mistake is assuming that because Massachusetts only regulates consumer transactions, platforms serving both consumers and businesses are fully exempt. The consumer-facing portion of your business may still trigger licensing requirements.

The line between consumer and commercial transactions gets especially blurry for:

- Multi-sided platforms

- Marketplace facilitators

- Embedded finance products

Each of these warrants careful transactional analysis before concluding you're out of scope.

Overlooking Virtual Currency Implications

Massachusetts did not adopt the specific virtual currency provisions of the MTMA model act. That said, the MDOB has explicitly stated that it considers most common transactional virtual currencies (including Bitcoin and USDC) to be a form of "monetary value." Companies engaged in virtual currency transmission require licensure under Chapter 169B. If you're relying on the new law's silence on crypto to claim exemption, the MDOB's published FAQ directly contradicts that position.

Frequently Asked Questions

What is a money transmission license?

A money transmission license is a state-issued authorization required to legally accept, hold, or transfer money on behalf of consumers. In Massachusetts, this is now governed by Chapter 312 of the Acts of 2024, administered by the Division of Banks.

Do I need a money transmitter license?

If your business sells payment instruments, issues stored value, or receives money for transmission from Massachusetts consumers for personal, family, or household purposes, you likely need a license—unless a specific exemption applies, such as agent of a payee or intermediary processor.

How much does a money transmitter license cost?

Massachusetts charges $1,300 in state fees ($1,000 license + $300 investigation), plus $120 NMLS processing fee and $51.25 per control person for background/credit checks. The surety bond (minimum $100,000) is an additional cost that varies based on creditworthiness and transmission volume.

Can I get my MA license online?

Yes. Massachusetts money transmitter license applications are submitted entirely through the NMLS online portal at nmlsconsumeraccess.org. The process includes electronic submission of documents, background checks, and bond information.

How to get MSB certification?

MSBs must register with FinCEN at the federal level and separately obtain state money transmitter licenses where required. In Massachusetts, state licensing runs through the Division of Banks via NMLS—both obligations apply independently.

What is a 12C license in Massachusetts?

A "12C license" was the former foreign money transmitter license category under Chapter 169 of Massachusetts law. That framework was replaced by the new money transmitter license under Chapter 312 of the Acts of 2024. Businesses holding 12C licenses transitioned to the new framework at their next renewal.

Need help navigating Massachusetts money transmitter licensing? Fraxtional provides fractional compliance leadership—including named CCOs and BSA Officers—for fintech, crypto, and payment companies managing the NMLS application process. Contact Fraxtional to discuss your licensing needs.