Introduction

Any business transmitting money in Arizona—including fintechs, payment apps, and crypto firms—must hold a state-issued Money Transmitter License from the Arizona Department of Financial Institutions (AZDFI). Operating without this authorization exposes companies to criminal liability under ARS Title 6, Chapter 12, with violations prosecuted as felonies under ARS § 13-2317.

Arizona overhauled its money transmission law in 2022 with Senate Bill 1580, adopting the Conference of State Bank Supervisors (CSBS) Model Money Transmission Modernization Act. That update revised:

- Net worth standards and minimum capital thresholds

- Surety bond calculations tied to transaction volume

- Permissible investment categories for customer funds

- Customer protection provisions for disclosures and refunds

The modernization aligns Arizona with national standards, enabling faster multistate expansion for compliant licensees. This guide covers exactly what your fintech, crypto platform, or payment service needs to apply, qualify, and stay compliant—whether you're entering Arizona for the first time or updating your program after the 2022 changes.

Key Takeaways

- A Money Transmitter License is required to sell payment instruments, issue stored value, or receive money for transmission from Arizona residents

- NMLS applications have a 120-day review window — no decision by day 120 triggers automatic approval

- Net worth minimum: $100,000; surety bond ranges from $25,000 to $500,000 based on daily transmission liability

- Fees: $1,500 non-refundable application fee, $500 annual renewal

- Post-approval: quarterly condition reports, annual audited financials, BSA/AML filings, and permissible investments equal to outstanding obligations

What Is the Arizona Money Transmitter License and Who Needs It?

The Arizona Money Transmitter License (AMTL) is the state-issued authorization required under ARS § 6-1207 before any person or entity may engage in, advertise, or hold itself out as providing money transmission services in Arizona. AZDFI issues and enforces these licenses under the modernized framework enacted in 2022.

Activities That Trigger Licensing

Under ARS § 6-1201, "money transmission" encompasses three distinct activities:

- Selling or issuing payment instruments to Arizona residents

- Selling or issuing stored value to Arizona residents

- Receiving money for transmission from Arizona residents

Digital nexus: Arizona's "in this state" definition covers more than physical presence. It includes any person's address, principal place of business, or account address in your records. If customer data ties to an Arizona address—even for a fully remote, digital business—licensure applies.

Who Is Exempt?

ARS § 6-1202 exempts:

- Federally insured depository financial institutions

- Government entities

- Registered broker-dealers

- Payment system operators providing only processing, clearing, or settlement between exempt entities

- Agents of a payee meeting specific written-agreement criteria

Warning: Claiming an exemption incorrectly carries significant legal risk. If you're unsure whether your business qualifies, assume licensure is required until you obtain definitive regulatory guidance.

Arizona Money Transmitter License: Document and Financial Requirements

Core Application Documents (NMLS Forms)

Applications go through NMLS using two primary forms:

- Form MU1 (Company Form): Legal name, fictitious/trade names, business addresses, and a description of proposed money transmission activities in Arizona. Also includes a list of proposed authorized delegates and locations, plus disclosure of material litigation or criminal convictions in the past 10 years.

- Form MU2 (Individual Form): Required for each key individual and control person

Financial Statement Requirements

Applicants must submit the following financial documentation:

- Audited financial statements prepared under U.S. GAAP for the most recent fiscal year (two prior years where available)

- Certified copy of unaudited statements for the most recent fiscal quarter

All statements must demonstrate the $100,000 minimum tangible net worth threshold—a baseline that scales upward with total assets, as described later in this guide.

Background Check Requirements

Every key individual, officer, director, partner, and any person controlling 10% or more of voting shares must:

- Submit fingerprints through NMLS

- Complete personal history questionnaires via NMLS

- Provide an independent investigative background report in English if they've lived outside the U.S. in the past 10 years (must include comprehensive credit report and court data search)

BSA/AML Program Documentation

Under ARS § 6-1220 and AZDFI practice, applicants must submit:

- Written AML/BSA Compliance Manual

- Current AML/BSA Risk Assessment

- Evidence of an AML/BSA Independent Review

AZDFI scrutinizes these for adequacy. Fintech companies and early-stage money transmitters that haven't yet built these programs may benefit from working with a fractional BSA Officer to develop compliant documentation before filing. Fraxtional provides fractional BSA Officer services specifically for this purpose—helping companies build AML/BSA programs that meet AZDFI standards without the cost of a full-time hire.

Additional Required Items

- Certificate of Good Standing from state of incorporation

- FinCEN registration as a Money Services Business

- Business plan with executive summary and financial projections

- Sample authorized delegate contract (if applicable)

- Sample payment instrument or stored value form

- Name and address of Arizona registered agent

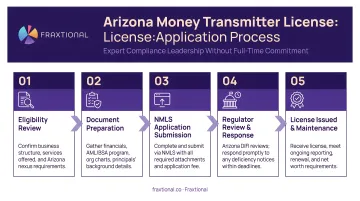

How to Apply for an Arizona Money Transmitter License: Step-by-Step

Arizona offers two pathways—NMLS (preferred for multistate operators) and the Arizona Professional Licensure E-licensing Portal. Both have identical requirements. Note that once issued, the license is not transferable or assignable to another entity.

Step 1: Register Your Business in Arizona

Before applying, your entity must be registered with the Arizona State Corporation Commission (for corporations and LLCs) or the Secretary of State (for limited partnerships and LLPs). You must also designate an active Arizona registered agent. This is a prerequisite, not part of the NMLS process itself.

Step 2: Register with FinCEN as a Money Services Business

Under 31 U.S.C. § 5330, applicants must register with FinCEN as an MSB via the BSA E-Filing System before or alongside the state application. Operating as an unlicensed money transmitter without FinCEN registration carries criminal penalties under ARS § 13-2317.

Step 3: Create an NMLS Account and Complete Application Forms

- Create a company account in NMLS

- Designate a Primary and Secondary Account Administrator

- Complete the Company (MU1) form

- Complete Individual (MU2) forms for all key individuals (owners, officers, control persons)

- Answer all disclosure questions fully — incomplete answers are a common cause of delays

- Attach supporting documentation for any "yes" disclosure answers before submitting

Step 4: Compile and Submit All Supporting Documents

Once your NMLS forms are complete, upload supporting documents electronically through NMLS or mail them to AZDFI. Required documents include:

- Audited and unaudited financial statements

- Surety bond

- Background check authorizations

- BSA/AML program documentation

- Business plan

- Certificate of Good Standing

Critical timing note: The application is not considered "complete" until all items are received. The 120-day review clock only starts from the completion date.

Step 5: Pay Fees and Await AZDFI Review

Pay the $1,500 non-refundable application fee plus the applicable prorated license fee at submission. Once the application is deemed complete, AZDFI has 120 days to approve or deny. If no decision is made within 120 days, AZDFI automatically approves the application. Any denial must specify the reasons and outline your appeal rights — so keeping a complete, well-documented file from day one is your best protection against rejection.

License Costs, Surety Bond, and Net Worth Requirements

Fee Structure

| Fee Type | Amount | Notes |

|---|---|---|

| Application Fee | $1,500 + $25 per branch/delegate (max $4,500) | Non-refundable |

| Annual Renewal Fee | $500 + $25 per branch/delegate (max $2,500) | Due annually |

| Late Renewal Penalty | $500 | If renewed by January 31 after expiration |

The first year's license fee is prorated by quarters remaining until the next renewal under ARS § 6-126.

Surety Bond Requirement

Under ARS § 6-1228, the bond amount is the greater of:

- $25,000 (minimum), or

- 100% of the licensee's average daily money transmission liability in Arizona (calculated over the most recently completed three-month period)

The bond is capped at $500,000.

If your tangible net worth exceeds 10% of total assets, you may maintain a reduced surety bond of just $25,000 regardless of transaction volume — which directly affects how you structure your net worth position.

Applicants pay only a surety premium—a percentage of the bond face value determined by the surety based on creditworthiness—not the full bond amount.

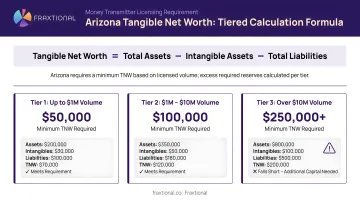

Tangible Net Worth Requirement

ARS § 6-1227 requires licensees to maintain at all times tangible net worth equal to the greater of:

- $100,000 (baseline), or

- 3% of total assets for the first $100 million in assets

Plus 2% of assets between $100M–$1B

Plus 0.5% of assets above $1B

Example calculations:

- $50M total assets: 3% of $50M = $1,500,000 required tangible net worth

- $1.2B total assets: 3% of $100M ($3M) + 2% of $900M ($18M) + 0.5% of $200M ($1M) = $22,000,000 required tangible net worth

Permissible Investments Requirement

Under ARS § 6-1229 and § 6-1230, licensees must continuously maintain permissible investments with a GAAP market value of not less than the aggregate amount of all outstanding money transmission obligations.

Permissible investments include:

- Cash and demand deposits in federally insured institutions

- AAA-rated money market mutual funds

- U.S. government obligations or state/governmental subdivision securities

- Excess surety bond (100% of bond amount exceeding average daily Arizona transmission liability)

- Irrevocable standby letters of credit from eligible-rated institutions

- Authorized delegate receivables less than 7 days old (capped at 50% of total permissible investments, max 10% from a single delegate)

- Rated short-term investments (commercial paper, bonds, tri-party repos, capped at 20% per category, 50% combined)

Early-stage applicants frequently miscalculate this requirement by focusing only on fees and bond costs. If your outstanding transmission obligations grow faster than your liquid investment position, you'll face a compliance gap that can stall renewal or trigger regulatory action.

Post-Licensing: Compliance Obligations and Common Pitfalls

Ongoing Reporting Obligations

After license issuance, licensees must file:

- Quarterly Reports of Condition: Due within 45 days of quarter end. Must include financial statements, transaction data, and permissible investments reports (ARS § 6-1216)

- Annual Audited Financial Statements: Due within 90 days of fiscal year end (ARS § 6-1217)

- Authorized Delegate Reports: Due within 45 days of quarter end

- Material Event Reporting: Immediate reporting (within 1–3 business days) for bankruptcy filings, criminal charges against key individuals, or license revocations in other states (ARS § 6-1219)

BSA/AML Ongoing Obligations

Under ARS § 6-1220 and § 6-1242, licensees and authorized delegates must:

- File all required Suspicious Activity Reports (SAR) and Currency Transaction Reports (CTR) with FinCEN

- Maintain transaction records for at least five years

- File duplicate suspicious activity reports with the Arizona Attorney General within 30 days for transactions of $5,000 or more meeting defined criteria

These obligations require a dedicated BSA Officer — someone accountable for filings, recordkeeping, and ongoing program oversight. Companies not ready to bring on a full-time hire often work with Fraxtional, whose fractional BSA Officer model provides director-level oversight at a fraction of the cost.

That complexity is also where most newly licensed transmitters run into trouble. Here are the four pitfalls that most commonly threaten licenses in Arizona.

Most Common Pitfalls

1. Incomplete BSA/AML Documentation

Submitting unreviewed or inadequate BSA/AML programs that fail AZDFI scrutiny delays applications by months. Ensure your AML Manual, Risk Assessment, and Independent Review are comprehensive and tailored to your business model.

2. Underestimating Permissible Investments

As transaction volume grows, permissible investments must scale proportionally. Many applicants underestimate this requirement relative to projected growth, creating compliance gaps shortly after licensure.

3. Missing Material Event Notification Deadlines

Failing to notify AZDFI within 1–3 business days when key individuals change or material events occur (bankruptcy, felony charges, license revocations) can jeopardize your license.

4. Operating as an Authorized Delegate of an Unlicensed Entity

Under ARS § 6-1223, anyone engaging in money transmission on behalf of an unlicensed or nonexempt person is jointly and severally liable with the unlicensed entity. Always verify your principal's licensure status.

Frequently Asked Questions

How do I get an Arizona money transmitter license?

Register through NMLS, submit Form MU1 along with all required documents (audited financials, surety bond, BSA/AML program, background checks), and pay a $1,500 application fee. AZDFI must complete its review within 120 days of a complete application.

Who needs a money transmitter license in Arizona?

Any person or company selling payment instruments, selling stored value, or receiving money for transmission to or from Arizona residents must be licensed. This applies even to remote or digital businesses with no physical presence in Arizona, per ARS § 6-1207.

How much does an Arizona money transmitter license cost?

Key costs include:

- Application fee: $1,500 (non-refundable)

- License fee: Prorated at time of approval

- Branch/delegate fees: $25 each

- Annual renewal: $500

- Additional costs: Surety bond premium and any legal or compliance preparation expenses

What is the surety bond requirement for Arizona money transmitters?

The bond must be the greater of $25,000 or 100% of average daily money transmission liability in Arizona over the most recent three-month period, capped at $500,000. Applicants pay only a premium based on creditworthiness, not the full bond amount.

How long does it take to get an Arizona money transmitter license?

AZDFI has up to 120 days to approve or deny a complete application. Preparation time—gathering documents, building BSA/AML programs, obtaining audited financials—often adds several weeks before submission, bringing total timelines to 4–6 months.

Does the 2022 Arizona law change affect existing money transmitter licensees?

Yes. SB 1580 (effective August 2022) replaced Arizona's prior statute with the CSBS Model Act, bringing new net worth standards, permissible investment rules, receipt requirements, and refund rights. Existing licensees received a transition period tied to their next renewal — but all are now subject to the updated requirements.