This guide is for founders, compliance officers, and financial services leaders navigating Virginia's money transmitter licensing framework. Virginia enacted significant updates to its money transmitter law in 2025, effective July 1, 2026, that fundamentally restructure net worth requirements, surety bond formulas, and permissible investment obligations. If you're relying on outdated guidance—such as the old $200,000 flat net worth minimum—you may significantly underestimate your capital requirements.

This guide covers what the Virginia Money Transmitter License is, who needs it, exact requirements under the new 2025 law, the step-by-step application process through NMLS, and ongoing compliance obligations after approval.

Key Takeaways

- Any business that sells payment instruments, issues stored value, or receives money for transmission from Virginia residents must hold a Virginia Money Transmitter License

- The Virginia State Corporation Commission regulates the license; expect a 120-day review period after your NMLS application is deemed complete

- Core requirements: $1,000 application fee, net worth minimum starting at $100,000, surety bond of $100,000–$1 million, and an independently reviewed AML/BSA program

- FinCEN MSB registration is also required before you can operate

- Operating without a license is a Class 1 misdemeanor with civil penalties up to $2,500 per transaction

- Post-approval, you must file quarterly condition reports, submit annual audited financials, oversee authorized delegates, and hold permissible investments covering all outstanding transmission obligations

What Is the Virginia Money Transmitter License?

The Virginia Money Transmitter License is a state-issued authorization required under Virginia Code Title 6.2 Chapter 19.1 (the 2025 law, effective July 1, 2026) that permits a business to engage in money transmission in Virginia.

Money transmission is defined as:

- Selling or issuing payment instruments

- Selling or issuing stored value

- Receiving money for transmission from persons located in Virginia

Under the new Virginia definition, money transmission explicitly includes payroll processing services — meaning companies that receive money to deliver wages, pay payroll taxes, or fund employee benefit plans now require licensure.

The definition does, however, exclude virtual currency from the definition of "money." Crypto platforms dealing exclusively in virtual currency (without fiat transmission legs) fall outside the scope, as does the provision solely of online or telecommunications services or network access.

Key Distinctions:

- This is a state-level requirement — separate from, and in addition to, any federal obligations

- You still need FinCEN's federal MSB registration alongside this license

- The license is issued to entities, not individuals

- Licenses are non-transferable

- Holding a license in another state does not exempt you from Virginia's requirement if you transmit money to or from Virginia residents

Who Needs a Virginia Money Transmitter License — and Who Is Exempt?

Who Needs a License

Any entity engaged in money transmission in Virginia must be licensed, including:

- FinTech startups and payment apps

- Remittance companies

- Payroll processors (new under the 2025 law)

- Stored value issuers

- Embedded finance platforms

Authorized delegates of a licensed entity do not need their own license, but must operate under a written contract with the licensee and are subject to the licensee's oversight.

Key Exemptions Under §6.2-1923

Virginia law provides specific statutory exemptions for certain entities:

Federally insured depository institutions:

- Banks, credit unions, and their subsidiaries

- Bank holding companies

- Qualifying foreign bank branches

Payment system operators: Entities providing only processing, clearing, or settlement services exclusively between exempt entities or licensees

Agents of payees:

- Persons collecting payments for goods or services under written agreement where the payor's obligation is extinguished upon receipt by the agent

Registered financial intermediaries: Securities broker-dealers and futures commission merchants operating within their registered scope

Government entities:

- USPS, state/local governments, and contractors handling electronic funds transfers for government benefits

Critical Note for Embedded Finance Companies

These exemptions matter most to embedded finance companies, where the line between "agent" and "money transmitter" is genuinely blurry.

If your company acts solely as an intermediary processing payments on behalf of a licensed entity, you may not need your own license—but the conditions are strict. The "agent of the payee" exemption requires contract language that confirms the consumer bears no risk of loss once funds reach the agent.

A common mistake: assuming that routing payments through a licensed banking partner automatically qualifies your company for an exemption. Under Virginia's statute, that assumption doesn't hold. The exemption analysis is fact-specific, and getting it wrong means operating without a required license — a violation Virginia takes seriously.

Virginia Money Transmitter License Requirements

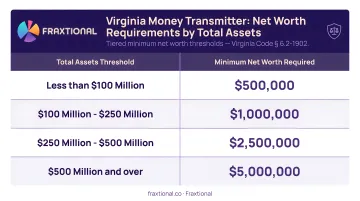

1. Tiered Net Worth Requirements (§6.2-1950)

Virginia's 2025 law replaces the old $200,000 flat minimum with a tiered tangible net worth structure based on total assets:

| Total Assets | Tangible Net Worth Requirement |

|---|---|

| ≤ $100 Million | Greater of $100,000 or 3% of total assets |

| $100M to $1 Billion | $3,000,000 plus 2% of assets in excess of $100 million |

| > $1 Billion | $21,000,000 plus 0.5% of assets in excess of $1 billion |

What this means in practice:

- Capital-light startups benefit from the $100,000 floor

- Scaling enterprises must forecast balance sheet growth against escalating capital requirements

- Tangible net worth must be demonstrated at application and maintained continuously

2. Surety Bond Requirements (§6.2-1951)

Virginia's surety bond requirement is now dynamically linked to Virginia-specific transmission liability:

Minimum bond amount:

- Greater of $100,000 or 100% of average daily Virginia money transmission liability for the most recent quarter

- Maximum cap: $1,000,000

- Alternative minimum: $100,000 if tangible net worth exceeds 10% of total assets

Critical Bond Rules:

- Bond must remain in place for five years after ceasing money transmission activities

- Cancellation requires 90 days' written notice to the Commission

- Surety companies will run credit checks on business owners

- Typical market premiums range from 1% to 12.5% annually based on credit profiles

3. Permissible Investments (§6.2-1952)

Licensees must at all times maintain permissible investments with a market value equal to aggregate outstanding money transmission obligations across all states.

Permissible investment types include:

- Cash in federally insured institutions

- U.S. government obligations

- Certificates of deposit from insured institutions

- AAA-rated money market mutual funds

- Irrevocable standby letters of credit (meeting specific SCC criteria)

- Senior debt obligations of insured depository institutions

Under the 2025 law, Virginia law holds permissible investments in statutory trust for consumers if the licensee becomes insolvent — giving regulators real-time visibility into your liquidity position as a continuous safeguard.

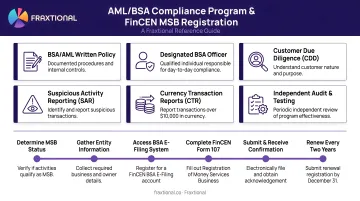

4. AML/BSA Program and FinCEN Registration

Federal MSB Registration:

- Applicants must register as a Money Services Business with FinCEN before applying for a Virginia license

- File FinCEN Form 107 (RMSB) within 180 days of establishment

- NMLS application requires your FinCEN Registration Confirmation Number and Filing Date

AML/BSA Compliance Program:

- Submit an independently reviewed AML/BSA policy with your application

- Policy must address BSA reporting obligations, suspicious activity monitoring, and compliance procedures

- The independent review is a mandatory application component—internal reviews are not sufficient

For early-stage fintechs and crypto companies, building a compliant AML/BSA program is often the most time-intensive part of the application. Fraxtional's fractional BSA Officers can serve as the named BSA Officer of record, satisfying the independent review requirement without the cost of a full-time compliance hire.

5. Personal History and Background Checks (§6.2-1932)

Every key individual and person in control must submit:

- Fingerprints for FBI criminal background check ($36.25 per person)

- Authorization for credit report ($15 per person)

- Disclosure of criminal convictions, regulatory actions, and civil litigation

- International background report if resided outside the U.S. in the past 10 years (commissioned from independent search firm covering 10 years of global court, credit, and media history)

Budget extra time and capital for international founders' background reports.

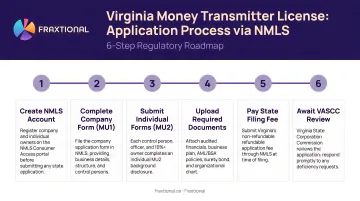

How to Apply for a Virginia Money Transmitter License: Step-by-Step

Applications are filed electronically through NMLS and reviewed by the Virginia State Corporation Commission, Bureau of Financial Institutions. The nonrefundable application fee is $1,000.

Step 1: Register Your Business Entity

Before applying, ensure:

- Business is properly registered in Virginia

- Federal EIN obtained

- Entity registered with the Virginia State Corporation Commission

- Certificate of Good Standing obtained

- Virginia Tax registration completed

Step 2: Register with FinCEN as a Money Services Business

Complete MSB registration with FinCEN:

- File FinCEN Form 107 (RMSB)

- Obtain FinCEN confirmation number and filing date

- This is mandatory before submitting your NMLS application

Step 3: Create an NMLS Account and Prepare Application Documents

Register for an NMLS company account, then assemble the full document package:

Financial Documents:

- Audited financial statements (most recent fiscal year + 2 prior years)

- Unaudited financial statements for most recent quarter

Operational Documents:

- Detailed business plan

- AML/BSA compliance policy

- Independent review of AML/BSA program

- Flow of funds structure

- Management and organizational charts

- Authorized delegate list

- Sample payment instrument or stored value forms

Corporate Documents:

- Company formation documents

- Certificate of Good Standing

Step 4: Complete and Submit MU1 and MU2 Forms, and Upload Documents to NMLS

Complete MU1 (company application) and MU2 (individual) forms in NMLS, upload all required documents, and pay applicable fees electronically.

Certain highly sensitive documents must be mailed directly to the Bureau of Financial Institutions — do not upload these to NMLS:

- Criminal history records checks

- Personal financial statements for control persons

- Three business references

- Bank references

- Independent background reports (for individuals who resided outside the U.S.)

Step 5: Obtain and Submit the Surety Bond

Obtain a bond in the required amount from an approved surety company. Note that surety companies will run credit checks on business owners, and the bond must be in a form satisfactory to the Commission.

Once secured, submit the bond in two ways:

- Upload completed bond form (including power of attorney) electronically through NMLS

- Mail the original to the Bureau of Financial Institutions

Step 6: Respond to Commission Review and Await Decision

The Commission first reviews your application for completeness. Once deemed complete, it has 120 days to approve or deny — if no decision is issued within that window, the application is automatically approved on the next business day. Expect possible outreach from a reviewing analyst to discuss your experience and operational readiness.

Approved licenses begin on the approval date and expire December 31 of that year. Exception: Licenses approved between November 1 and December 31 expire December 31 of the following year.

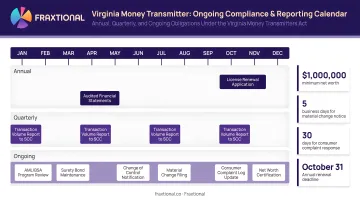

Ongoing Compliance Obligations After Getting Licensed

Reporting Requirements

Quarterly Report of Condition:

- Due within 45 days of each quarter-end

- Covers financial data, transaction volumes, permissible investment status, and authorized delegate information

Annual Audited Financials:

- Due within 90 days of fiscal year-end

Material Change Reporting:

- Any material change to business or key individuals must be reported promptly

Event-Triggered Reporting:

- 1-day events: Bankruptcy, receivership, or license revocation in another state

- 3-day events: Felony indictments or convictions of key individuals or authorized delegates

License Renewal

Annual renewal mechanics:

- License renews annually on December 31

- $750 renewal fee due no more than 60 days before expiration

- Renewal includes disclosure of material changes from original application

- Failure to maintain net worth thresholds, surety bond coverage, or permissible investment levels can trigger suspension or revocation

Authorized Delegate Oversight

Licensees are strictly liable for authorized delegates and must maintain:

- Written contracts with each delegate

- Background checks on delegates

- Risk-based supervision programs

- Monitoring and audit protocols

Record Retention

Maintain all transaction records for minimum of three years, including ledgers, bank statements, and compliance documentation.

For lean fintech teams, keeping up with these obligations is time-intensive without dedicated compliance staff. Fraxtional's fractional CCO and BSA Officer services provide director-level compliance leadership — embedded directly with your team as the named compliance officer of record — without the cost of a full-time hire.

Common Mistakes and Misconceptions About the Virginia Money Transmitter License

Mistake 1: Relying on Outdated Requirements

Many guides (and even some advisors) still reference pre-2025 requirements—including the flat $200,000 net worth minimum and the $25,000–$500,000 bond range. The 2025 law (effective July 1, 2026) replaced these with tiered net worth thresholds starting at $100,000 and a new bond formula based on average daily money transmission liability.

Consequence: Companies relying on outdated guidance may underestimate their capital requirements, leading to application delays or denials.

Mistake 2: FinCEN vs. State License Confusion

A federal FinCEN MSB registration does not substitute for a Virginia state money transmitter license. Both are required. Operating with only FinCEN registration is non-compliant and exposes your business to criminal and civil penalties.

Holding a license in another state does not exempt you from Virginia's licensing requirement if you transmit money to or from Virginia residents.

Mistake 3: Underestimating Penalty Risk

Operating without a license is not just a civil matter. The exposure stacks up fast:

- Criminal liability: Unlicensed operation is a Class 1 misdemeanor under §6.2-1957

- Civil penalties: Up to $2,500 per violation under §6.2-1955

- Per-transaction counting: Each unlicensed transaction is a separate violation

A payment business processing 1,000 transactions before discovery faces up to $2.5M in civil exposure alone—before any criminal charges.

Frequently Asked Questions

How much does it cost to get a money transmitter license in Virginia?

The $1,000 nonrefundable application fee covers the application itself, plus $36.25 per person for FBI background checks and $15 per person for credit reports. Surety bond premiums run 1%–12.5% of the bond amount annually, depending on credit profiles. Annual renewal is $750.

What can you do with a money transmitter license in Virginia?

A Virginia money transmitter license authorizes selling or issuing payment instruments, issuing stored value, and receiving money for transmission on behalf of Virginia-based persons — covering payment apps, remittance services, payroll processors, and similar operations.

How long does it take to get a Virginia money transmitter license?

Once the application is deemed complete, the Commission has 120 days to approve or deny it. In practice, pre-submission preparation — document assembly, surety bond procurement, AML/BSA program build-out, and FinCEN registration — typically adds several months to the overall timeline.

Who is exempt from the Virginia money transmitter license requirement?

Key exemptions under §6.2-1923 include federally insured banks and credit unions, authorized delegates of licensed transmitters, agents of payees collecting for goods/services, and registered broker-dealers. Companies should conduct a formal exemption analysis before assuming they qualify — the agent-of-payee carve-out in particular carries narrow conditions that are easy to misread.

What is the net worth requirement for a Virginia money transmitter license?

The tiered tangible net worth structure under the 2025 law starts at the greater of $100,000 or 3% of total assets for licensees with assets under $100 million. This replaces the prior flat $200,000 requirement. Larger entities face significantly higher thresholds.

What happens if I operate as a money transmitter in Virginia without a license?

Unlicensed operation is a Class 1 misdemeanor under §6.2-1957, and each unlicensed transaction can trigger a separate civil penalty of up to $2,500 under §6.2-1955. This creates compounding legal and financial exposure for payment businesses.