Introduction

A single failed compliance audit can trigger consequences that take years to recover from — regulatory sanctions, frozen licenses, or a sponsor bank ending the relationship overnight. For fintech, crypto, and embedded finance companies, these aren't theoretical risks. They're outcomes that have materialized repeatedly across the industry.

The pressure is especially acute for scaling companies operating across the US, UK, EU, or Canada without a dedicated compliance team. When an examiner from FinCEN, the FCA, or FINTRAC requests documentation, there's no room to improvise. The procedure is formal, expectations are specific, and gaps become findings — findings that can escalate into enforcement actions, consent orders, or license revocations.

This guide covers what a regulatory compliance audit actually is, why it carries real consequences for financial services companies, how the procedure works step by step, and what a realistic preparation process looks like in practice. The goal is to help your organization build genuine readiness before an examiner comes knocking.

Key Takeaways

- A regulatory compliance audit confirms whether your organization's operations conform to applicable laws across frameworks like BSA/AML, GDPR, and FCA rules

- Internal audits find gaps proactively; external/regulatory audits carry enforcement consequences

- The procedure follows six stages: scope definition, documentation, process testing, findings analysis, reporting, and remediation

- Common failure points like incomplete documentation, unresolved prior findings, and undertrained staff can be caught before an audit begins

- Cross-border fintech and crypto companies face compounded complexity from overlapping regulatory frameworks

What Is a Regulatory Compliance Audit?

A regulatory compliance audit is a structured evaluation of whether an organization's policies, procedures, and operations conform to applicable laws and regulatory standards. Unlike a general internal audit — which focuses on operational efficiency and risk management — a compliance audit has a narrower, higher-stakes mandate: are you following the specific rules that govern your industry?

In financial services, those rules vary by jurisdiction and business model:

- US: BSA/AML requirements under FinCEN, Reg E, UDAAP, OFAC sanctions

- UK: FCA SYSC 6 obligations, the Money Laundering Regulations 2017

- Canada: FINTRAC requirements under the PCMLTFA, including program elements and a biennial effectiveness review

- EU/cross-border: AML/CFT directives, EBA guidelines, and FATF standards for virtual assets

Crypto firms and embedded finance companies face a layered set of obligations, often spanning multiple jurisdictions simultaneously. That complexity makes understanding what actually triggers an audit — and which type — one of the more practical questions a compliance team can answer upfront.

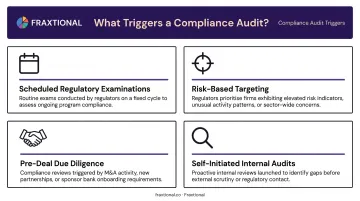

What Triggers a Compliance Audit?

Not all audits are created equal. The trigger determines the stakes:

- Scheduled regulatory examinations — periodic supervisory reviews mandated by bodies like the FCA, FinCEN, or FINTRAC based on your risk profile and prior findings

- Risk-based targeting — FFIEC scoping uses an institution's products, customers, and geographies to develop examination plans; higher-risk profiles attract closer scrutiny

- Pre-deal due diligence — sponsor banks and investors conduct their own compliance reviews before entering partnerships; the OCC's interagency guidance on third-party relationships requires it

- Self-initiated internal audits — proactive reviews ahead of licensing applications, market expansions, or known program gaps

The distinction between a regulatory audit (conducted or mandated by an external regulatory body) and a statutory audit (a legally required independent review of financial statements) is worth keeping clear. The two are conducted by different parties, serve different purposes, and carry different consequences — conflating them is a common and costly mistake.

Why Regulatory Compliance Audits Are Critical for Financial Companies

The numbers make the case plainly. According to Fenergo's 2024 AML enforcement analysis, global enforcement actions against financial institutions totaled $4.6 billion in 2024, with transaction monitoring failures alone accounting for $3.3 billion of that figure. The year prior saw $6.6 billion — a 57% increase from 2022.

Individual cases illustrate what audit failure looks like at scale:

| Entity | Regulator | Penalty | Primary Finding |

|---|---|---|---|

| TD Bank | FinCEN | $1.3B | Willful BSA violations; largest depository institution penalty in FinCEN history |

| Starling Bank | FCA | £28.9M | 54,000+ accounts opened for high-risk customers despite a self-imposed account freeze |

| Block / Cash App | State regulators | $80M | BSA/AML violations in CDD, identity verification, and SAR reporting |

| Binance Holdings | FINTRAC | CAD $6M | Failure to register as a foreign money services business |

Beyond fines, enforcement actions can carry operational consequences that hurt more than any penalty. The OCC required Blue Ridge Bank to obtain written non-objection before onboarding new fintech partners — a restriction that directly limited its growth.

The Proactive Case for Compliance Audits

Regular compliance audits build institutional credibility that goes beyond penalty avoidance. For Series A/B fintechs, that credibility is what unlocks new banking partnerships and clears investor due diligence reviews.

Sponsor banks expect maturity and consistency from fintech partners. A company that arrives at a pre-deal review with current documentation, a qualified BSA Officer, and evidence of internal testing signals it's ready to operate at scale — not just ready to talk about it.

That distinction shapes which fintechs get partnership offers — and which ones don't.

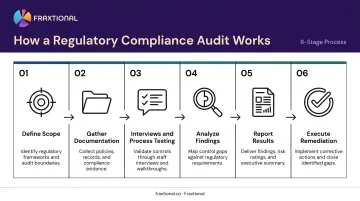

How a Regulatory Compliance Audit Works – Step by Step

While every audit varies by regulator and jurisdiction, the underlying procedure follows consistent logic. The FFIEC BSA/AML Examination Manual and FINTRAC's assessment framework both describe similar phases: scoping, assessment, and finalizing conclusions. Understanding each stage helps companies allocate preparation resources correctly.

Step 1 – Define Scope and Objectives

Clarify upfront what the audit covers: which regulations, business lines, geographies, and time periods are in scope. For a cross-border fintech, this might mean deciding whether to audit BSA/AML controls, data privacy obligations, consumer protection requirements, or all of the above. Scope creep is a real risk. Define boundaries in writing before fieldwork begins.

Step 2 – Gather and Organize Documentation

Auditors will request specific evidence. Have it ready before the audit begins:

- Written AML/compliance policies and procedures

- BSA/AML program documentation, including risk assessments

- Transaction monitoring reports and alert disposition records

- KYC/CDD files for customer samples

- SAR filing logs and supporting documentation

- Staff training records (current and dated)

- Prior audit findings and remediation evidence

- Board or management reporting on compliance matters

Incomplete or outdated documentation is among the most common reasons audits produce adverse findings. If a procedure exists but isn't documented, auditors treat it as if it doesn't exist.

Step 3 – Conduct Interviews and Process Testing

Auditors don't just read documents — they test whether documented procedures are actually followed. This phase involves:

- Interviews with the BSA Officer, compliance staff, and senior leadership

- Walkthroughs of key processes: customer onboarding, suspicious activity reporting, transaction screening

- Sample testing of individual KYC files and transaction monitoring records for accuracy and consistency

The gap between written policy and operational reality is where most significant findings originate.

Step 4 – Analyze Findings and Identify Gaps

Collected evidence is compared against regulatory standards to identify deficiencies. The FFIEC consumer compliance rating system evaluates findings across four dimensions: root cause, severity, duration, and pervasiveness.

That last factor matters. A recurring gap is treated more seriously than an isolated one. Findings are then mapped to the specific requirements not met, which drives the remediation roadmap.

Step 5 – Report Results and Issue Recommendations

The compliance audit report contains three core components:

- Scope and methodology summary — what was reviewed and how

- Findings with evidence and risk ratings — specific gaps tied to regulatory requirements

- Corrective action recommendations — each with a target completion timeline

For external or regulatory audits, this report may be shared directly with the regulating body. Regulators read it looking for acknowledgment of gaps and a credible remediation plan — format and tone reflect on your compliance culture.

Step 6 – Execute Remediation and Close the Loop

The audit doesn't end at the report stage. Organizations must implement corrective actions, document evidence of remediation, and in many cases submit a formal response to regulators confirming that gaps have been addressed.

Failure to follow through is treated as an aggravating factor in subsequent reviews. Partial remediation is nearly as problematic as none at all — auditors check whether prior findings were fully resolved, not simply acknowledged.

Regulatory Compliance Audit in Practice: A Fintech Scenario

A Series B cross-border payments company operating in the US and UK receives notice of an upcoming BSA/AML compliance review. Here's what a realistic preparation and response process looks like.

Pre-audit phase: The compliance team pulls together AML policy documentation and reviews transaction monitoring alert disposition records. Training logs show most staff certifications are current — but two employees completed training over 14 months ago.

Worse, a prior internal review had identified two gaps in the enhanced due diligence process that were only partially addressed. Partial remediations draw scrutiny — auditors look specifically for findings that were acknowledged but not closed.

During the audit: Auditors request a sample of 25 KYC files for high-risk customers and schedule a call with the BSA Officer and operations lead. During file review, they find inconsistencies between the written EDD policy and actual file-level documentation — several files are missing required source-of-funds documentation that the policy explicitly requires. That gap between written procedure and practice becomes a significant finding.

Post-audit: The company receives a findings report with two significant findings and one critical finding tied to incomplete SAR documentation procedures. They have 30 days to submit a written remediation plan and 90 days to demonstrate corrective action.

An effective response requires:

- A specific root cause analysis for each finding

- Documented corrective actions with named owners and realistic deadlines

- Interim controls in place while permanent fixes are completed

- A tracking mechanism the regulator can review at follow-up

Building a clean-audit foundation:

- A living compliance program with current, documented procedures

- A designated, qualified BSA Officer with clear accountability

- Regular internal testing — not just annual reviews

- A remediation tracking process that closes findings fully, not partially

Companies that avoid these findings share one trait: they treat internal testing as continuous, not calendar-driven. By the time an auditor arrives, there are no surprises to manage.

How Fraxtional Can Help

Most scaling fintechs and crypto firms don't need a full-time Chief Compliance Officer or BSA Officer on day one. But they do need director-level compliance expertise embedded in the business — particularly when an examination is approaching, a sponsor bank is conducting due diligence, or post-audit remediation is time-sensitive.

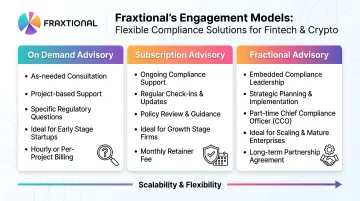

Fraxtional was built for exactly that gap. Recognized as a Top 10 Best Fractional Compliance Firm in the US for 2024 and 2025 — with founder Ryan Cimo named one of the Top 100 Leaders in Finance — the firm delivers fractional compliance leadership across the US, UK, EU, and Canada through three engagement models:

- On Demand Advisory: flat-fee project work — pre-audit reviews, risk assessments, policy development

- Subscription Advisory: ongoing retainer with a dedicated Director for sustained readiness and staff augmentation

- Fractional Advisory: named executive title (CCO, BSA Officer, MLRO, CAMLO) with continuous leadership accountability

For audit-specific support, Fraxtional's team:

- Conducts pre-audit internal reviews, delivering board-ready findings and prioritized remediation roadmaps

- Builds BSA/AML program documentation aligned with FFIEC, FinCEN, FATF, and FCA standards

- Prepares clients for FinCEN examinations, FCA supervisory reviews, and FINTRAC assessments

- Represents clients in regulatory conversations, with fractional BSA Officers and CCOs named directly on regulatory filings

- Leads post-audit remediation planning and tracks corrective actions through to closure

Fraxtional's AML frameworks are pre-approved by sponsor banks and have been used in pre-deal compliance reviews trusted by investors and banking partners. Team credentials span CAMS, CFE, ACAMS FCI, ABA CERP, and Certified Bitcoin Professional — covering both traditional BSA/AML and digital asset compliance.

Conclusion

A regulatory compliance audit reflects the health of your entire compliance infrastructure — not just your preparation in the weeks before an examiner arrives. Companies that treat audit readiness as an ongoing practice come out of examinations in far better shape. That means maintained documentation, regular internal testing, and qualified leadership already embedded in the business before any regulator sends a request letter.

For fintech and financial services companies operating across multiple jurisdictions, having qualified compliance leadership embedded in the business is the most direct path to sustained audit readiness. A fractional CCO, BSA Officer, or MLRO — engaged through a flexible retainer rather than a full-time hire — gives growing firms that expertise at a cost that scales with the business. That's the practical difference between companies that pass audits and those that spend months recovering from them.

Frequently Asked Questions

What is the difference between a regulatory audit and a statutory audit?

A regulatory audit assesses whether an organization is adhering to industry-specific laws and regulations, such as BSA/AML requirements, FCA rules, or FINTRAC obligations. A statutory audit is a legally required independent examination of an organization's financial statements to verify their accuracy and fairness. They serve different purposes and are conducted by different parties.

What are the 4 types of audit?

The four main types are:

- Regulatory compliance audits — adherence to laws and regulations

- Financial/statutory audits — accuracy of financial statements

- Operational audits — efficiency of internal processes

- Internal audits — broad evaluation of risk management and controls

Fintech and financial companies often face several types at once, especially during regulatory scrutiny or investor due diligence.

How often should a fintech company conduct a compliance audit?

Most regulators expect at least an annual compliance review; FINTRAC requires a program effectiveness review at least every two years. High-risk businesses (crypto firms, money transmitters, cross-border payment companies) should test quarterly or semi-annually to catch gaps before examiners do.

What documents are typically required for a regulatory compliance audit?

Auditors typically request:

- Written AML/compliance policies and procedures

- KYC/CDD files and transaction monitoring records

- SAR filing logs and staff training records

- Prior audit findings with remediation evidence

- Risk assessments and board/management compliance reporting

How current and complete these records are matters as much as whether they exist at all.

What happens if a company fails a regulatory compliance audit?

Consequences range from written findings requiring a remediation response to more serious enforcement actions — fines, mandatory third-party compliance reviews, cease-and-desist orders, or restrictions on onboarding new customers or partners. Severity depends on the nature of the findings and whether prior issues were left unaddressed. Unresolved repeat findings draw the harshest responses.

Do fintech startups need a dedicated compliance officer to pass a regulatory audit?

Many regulators — particularly in BSA/AML — require a designated compliance officer to be in place. However, this doesn't have to be a full-time in-house hire. A qualified fractional compliance officer with relevant credentials and industry experience can satisfy regulatory expectations, and has done so for fintech and crypto firms across sponsor bank reviews and regulatory examinations.