Introduction

Most regulated firms don't fail onboarding compliance because they ignore it. They fail because they treat it like a generic HR process when regulators expect something far more specific.

For most industries, a standard HR checklist covers the basics. In financial services — fintech, banking, crypto, money transmission — that's nowhere near enough.

Regulatory frameworks like BSA/AML, GDPR, CCPA, and FCA rules impose direct obligations on what employees must be trained on, what they must acknowledge, and when. Missing those requirements doesn't just create HR problems; it creates examinable compliance failures.

The gap between general onboarding and compliance onboarding is exactly where regulated firms get caught. Audit-ready documentation, role-based training, jurisdiction-specific verification — none of that appears on a generic first-week checklist.

This guide walks through every onboarding compliance step in sequence — from pre-hire verification and role-based training assignments to BSA/AML acknowledgments, ongoing obligations, and audit-ready documentation — with specific attention to what financial services firms must do differently.

Key Takeaways

- Onboarding compliance spans documentation, identity verification, training, and policy acknowledgment — each step carries its own audit exposure

- Financial services adds BSA/AML training, data privacy obligations, and role-specific regulatory requirements on top of standard HR steps

- Compliance training must be documented with signed acknowledgments — completion records are examinable

- The most common failures are treating onboarding compliance as a one-time event, relying on generic checklists, and missing jurisdiction-specific requirements

- Organizations without dedicated compliance leadership carry the highest exposure; fractional compliance officers close that gap without a full-time hire

What Is Onboarding Compliance?

Onboarding compliance is the set of processes an organization must complete to legally and regulatorily integrate a new employee — covering documentation, employment eligibility verification, mandatory training, and policy acknowledgment.

The goal is threefold: the organization meets its legal obligations, the employee understands the rules of their role, and a documented record exists proving both happened.

How It Differs from General Onboarding

General onboarding focuses on cultural integration and role readiness — team introductions, system access, job expectations. Compliance onboarding is specifically about legal, regulatory, and policy obligations.

The distinction matters most in regulated industries. Consider what each side covers:

- General onboarding: role clarity, team integration, system access, culture fit

- Compliance onboarding: I-9 verification, mandatory training completion, policy sign-offs, audit-ready documentation

In most industries, failing one means a poor employee experience. In regulated industries, failing the compliance side means failed audits, regulatory penalties, and potential license revocation. These are two separate obligations — and only one carries legal consequences.

Why Onboarding Compliance Is Critical in Financial Services

Regulated firms operate under frameworks — BSA/AML, UDAAP, Reg E, GDPR, FCA/FinCEN rules — that don't treat employee training as optional. They treat it as a control. If a new hire handles transactions without AML awareness, or accesses sensitive data without privacy training, the firm bears the regulatory consequence.

The penalties for AML program failures illustrate the stakes:

| Firm | Regulator | Penalty | Failure Signal |

|---|---|---|---|

| Binance | FinCEN (2023) | $3.4B | AML program and sanctions failures |

| TD Bank, N.A. | OCC (2024) | $450M | BSA/AML deficiencies, growth restriction imposed |

| USAA FSB | FinCEN (2022) | $140M | Deficient AML training at documented review |

| Al Rayan Bank | FCA (2023) | £4,023,600 | Inadequate AML controls, staff training cited |

| Ghana International Bank | FCA (2022) | £5,829,900 | Poor AML and counter-terrorism financing controls |

Sources: FinCEN Binance settlement, OCC TD Bank order, FCA Al Rayan notice

These cases set the benchmark for what regulators expect from AML programs — and onboarding is where those programs either start correctly or don't.

The exposure extends to individuals, not just firms:

- FinCEN assessed a $1 million penalty against the former MoneyGram chief compliance officer and sought to bar him from the financial industry

- In Canada, FINTRAC's administrative monetary penalty policy allows individual fines up to CAD $100,000 per serious violation

The Onboarding Compliance Process: Step-by-Step

Onboarding compliance runs from before a hire's first day through their first weeks. Each step has a distinct legal or regulatory function — skipping one doesn't just create a gap, it creates an examinable finding.

Step 1: Preboarding and Pre-Employment Verification

Before day one, the following must be completed:

- Employment eligibility verification (US) — Form I-9 required for all hires; Section 1 due by day one, employer review within 3 business days

- Right-to-work checks (UK) — must be completed before employment begins; no exceptions

- Social Insurance Number (Canada) — employers must request within 3 days of employment start

- Background checks and reference verification — standard across most roles; required for regulated roles

- Regulatory screenings — for financial services firms, this includes FINRA Form U4 filings for broker-dealer associated persons, with accuracy verification required within 30 calendar days of filing under FINRA Rule 3110(e)

- FCA fit-and-proper assessments — Senior Management Functions require FCA or PRA approval before starting their roles; no exceptions

Multi-jurisdiction hires require separate preboarding workflows — deadline mismatches between US, UK, and Canadian requirements are one of the most common sources of early compliance gaps.

Step 2: Required Documentation and Recordkeeping

Core documentation collected at or before the start date includes:

- Employment contract and offer letter

- Tax withholding forms (W-4 in the US, P45/P46 in the UK, TD1 in Canada)

- Benefit enrollment forms

- State or jurisdiction-specific required notices

- Signed acceptable use and data access agreements

Financial services firms require additional documentation: dual-control acknowledgments, data classification notices, and regulatory disclosure forms specific to the employee's role and access level.

Step 3: Compliance Training and Policy Acknowledgment

This is where most regulated organizations fall short — not because they skip training, but because they can't prove it happened correctly.

Minimum training coverage for all employees:

- Code of conduct and ethics policy

- Anti-harassment and workplace conduct

- Cybersecurity awareness and acceptable use

Regulated roles carry additional mandatory coverage:

- AML/BSA awareness, including red flags and suspicious activity reporting obligations

- Data privacy training mapped to applicable law (GDPR, CCPA, PIPEDA, UK GDPR) based on data access and role

- Sanctions screening awareness for relevant operations staff

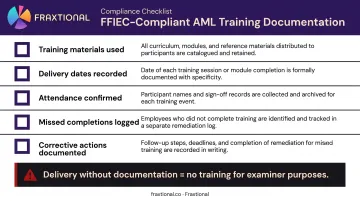

Every module must result in a signed acknowledgment. The FFIEC BSA/AML Examination Manual explicitly states that examiners expect documented training records — covering materials used, delivery dates, attendance, missed completions, and corrective actions taken.

Delivery without documentation is, for examiner purposes, the same as no training at all.

Financial Services-Specific Compliance Requirements During Employee Onboarding

Standard HR checklists were not designed for regulated environments. Financial services onboarding carries a second tier of requirements that must be addressed separately.

BSA/AML Training as a Day-One Control

AML training obligations attach to specific regulatory frameworks by entity type:

- Banks (31 CFR 1020.210): FFIEC guidance requires a BSA overview during orientation or shortly after; training records must be available for examiner review

- Money services businesses (31 CFR 1022.210): Same requirement applies across the board

- FINTRAC (Canada): Compliance program guidance explicitly allows event-based training — including before a new employee deals with clients

AML onboarding training is a regulatory gate before transaction-handling begins — not an orientation nicety.

Data Privacy Training by Role and Jurisdiction

Privacy training obligations are role-based, not universal. The relevant hooks by jurisdiction:

- GDPR / UK GDPR (Article 39): DPOs must monitor staff training for employees involved in processing operations

- CCPA/CPRA: Staff handling California consumer privacy inquiries must be informed of consumer rights requirements

- PIPEDA: Accountability obligations include staff training and communication as core fair-information principles

For fintech and embedded finance companies handling high volumes of sensitive financial data, these aren't abstract requirements — they attach to specific roles and access levels from day one.

Role-Based and Jurisdiction-Specific Obligations

Senior and regulated roles carry pre-start obligations that must be sequenced correctly:

- FCA Senior Management Functions — require FCA or PRA approval before the individual begins acting in the role

- FCA Certification Regime — covered staff must be certified as fit and proper on appointment and at least annually thereafter

- FINRA registered persons — Form U4 must be filed and verified within 30 calendar days

- FINTRAC compliance officer — must have documented authority, resources, and knowledge of the firm's business structure and ML/TF risk exposure

For fintechs and startups scaling across the US, UK, EU, or Canada, no single global template covers these requirements. Each jurisdiction adds its own sequencing obligations, and the gaps tend to surface during examinations or investor due diligence.

Firms without dedicated compliance leadership — a full-time CCO, fractional BSA Officer, or MLRO — carry the highest risk of acting-in-role violations. Fraxtional places named executives into these roles, including regulatory filing use, across all four jurisdictions without requiring a full-time hire.

Common Mistakes in Onboarding Compliance

Treating It as a One-Time Paperwork Exercise

The most common mistake is assuming that completing onboarding tasks once creates a permanent compliance record. Regulators don't see it that way. FFIEC expects not just that training happened, but that completion was tracked, missed completions were remediated, and records are available on demand.

Using a Generic HR Checklist in a Regulated Environment

A standard HR onboarding checklist doesn't include AML red flag training, FINRA Form U4 verification, FCA pre-approval sequencing, or role-based data privacy obligations. Using one in a financial services context actively creates false assurance that compliance has been addressed when it hasn't.

Common oversimplifications:

- Sending the same compliance training module to all employees regardless of role

- Assuming multi-state or multi-country hires share the same documentation requirements

- Treating a signed offer letter as a substitute for documented policy acknowledgment

Confusing Onboarding Compliance with Ongoing Training

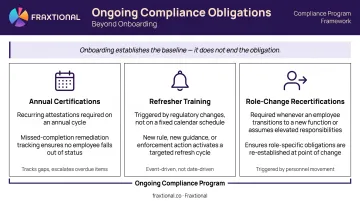

Onboarding compliance establishes the baseline. It is not the end of the obligation.

Three distinct ongoing requirements each carry their own documentation trail:

- Annual certifications — recurring attestations that must be tracked and remediated on missed completions

- Refresher training — triggered by regulatory changes, not scheduled on a fixed calendar

- Role-change recertifications — required when an employee moves into a new function with different compliance obligations

Organizations that treat first-week training as the whole program will fail examiner review when these ongoing records don't exist.

Frequently Asked Questions

What is onboarding compliance?

Onboarding compliance is the process of ensuring new hires complete all steps required by law and regulation during integration, covering employment eligibility verification, mandatory documentation, and role-specific training. The goal is to protect the organization from legal exposure and maintain a documented record that obligations were met.

What are the 5 C's of onboarding?

The 5 C's framework covers: Compliance (legal and regulatory requirements), Clarification (role expectations), Culture (organizational values), Connection (team relationships), and Check-back (ongoing feedback during the transition). In regulated industries, the Compliance component requires significantly more depth than the others.

Who is responsible for onboarding compliance?

Responsibility is typically shared among HR, legal/compliance, hiring managers, IT, and payroll. In regulated industries, a dedicated compliance officer (or fractional equivalent) should own the compliance-specific components. HR alone does not have the technical depth required for BSA/AML, FCA, or FINTRAC obligations.

What documents are required for employee onboarding compliance?

The standard set includes employment eligibility verification (Form I-9 or jurisdiction equivalent), tax withholding forms, employment contracts, benefit enrollment forms, and signed policy acknowledgments. Financial services firms add regulatory-specific documentation, including dual-control acknowledgments and data access agreements.

How does onboarding compliance differ for financial services companies?

Financial services firms must go beyond standard HR requirements: BSA/AML training before transaction handling, data privacy certifications mapped to applicable law, and role-based regulatory disclosures are all required. Senior regulated roles also require fit-and-proper assessments or regulatory pre-approval, with full documentation maintained for examiner review.

What happens if a company fails to meet onboarding compliance requirements?

Consequences range from regulatory fines and failed examiner reviews to increased sponsor bank scrutiny and potential license revocation. In financial services, compliance officers can face personal liability — FinCEN assessed a $1 million penalty against an individual compliance officer for program failures.