Introduction

The Michigan Money Transmitter License is the state-issued authorization required to legally provide money transmission services in Michigan under the Money Transmission Services Act (2006 PA 250), codified at MCL § 487.1001–487.1047. Operating without it carries serious consequences.

Knowingly engaging in unlicensed money transmission is a felony under Michigan law, punishable by up to five years imprisonment and fines up to $100,000. Civil penalties add up to $10,000 per day for ongoing violations.

This guide is written for fintech startups, crypto companies, payment platforms, and embedded finance businesses transmitting money in Michigan. If you receive, transmit, or issue payment instruments in the state — whether through a digital wallet, cross-border remittance service, or payment processor — this license applies to you.

This guide covers:

- What qualifies as money transmission under Michigan law

- Who must be licensed and available exemptions

- Application requirements and the NMLS filing process

- Ongoing compliance obligations after approval

Key Takeaways

- Michigan requires licensing for any entity receiving, transmitting, or issuing payment instruments under the Money Transmission Services Act (effective January 1, 2007)

- Submit applications through NMLS; the Michigan Department of Insurance and Financial Services (DIFS) has 120 days to approve or deny completed applications

- Core requirements: $500,000–$1,500,000 surety bond, $100,000–$1,000,000 minimum net worth, and a documented AML/BSA program

- Licenses expire December 31 annually and must be renewed by December 1 each year

- Quarterly MSB Call Reports and authorized delegate management are mandatory ongoing obligations

What Is the Michigan Money Transmitter License and Who Needs One?

The Michigan Money Transmission Services Act (2006 PA 250) governs all money transmission activity in the state and has required licensing since January 1, 2007. MCL § 487.1011 establishes the core authority: no person may provide money transmission services without a license after December 31, 2006.

If your business moves money on behalf of customers — in any form — this law almost certainly applies to you.

What Counts as Money Transmission?

Under MCL § 487.1003, "money transmission services" means:

- Selling or issuing payment instruments

- Selling or issuing closed-loop prepaid access devices or vehicles

- Receiving money or monetary value for transmission

The statute excludes pure telecommunications services, network access, credit card vouchers, letters of credit, and tangible objects redeemable in goods or services by the issuer.

Who Needs This License?

You must hold a Michigan Money Transmitter License if you operate as a principal in any of these business models:

- Fintech payment platforms processing person-to-person or business payments

- Digital wallet providers holding customer funds for transmission

- Remittance companies transferring money domestically or internationally

- Money order issuers selling payment instruments to consumers

- Crypto firms holding or transmitting customer funds — including cryptocurrency

- Any company acting as a principal in a Michigan money transmission flow

Authorized delegates of a licensed entity do not need their own separate license, provided they operate under a written agreement with the licensed principal and comply with the Money Transmission Services Act (MTSA).

Michigan Money Transmitter License Requirements

Meeting DIFS requirements involves business documentation, financial guarantees, and a credible compliance program. Here's what to prepare:

Business Documentation

Prepare the following core documents:

- Registered Michigan business entity with formation documents

- Certificate of Authority or Good Standing dated within 60 days of application

- Organizational chart showing ownership structure

- Management chart identifying key personnel and control persons

- Business plan detailing operations and flow of funds

- FinCEN registration confirmation number

- Registered agent information for Michigan service of process

- Disclosure questions and control person attestations (MU2 forms)

Consult the NMLS Michigan Phase 2 Checklist for the complete requirements list.

Surety Bond

The surety bond requirement under MCL § 487.1013 is:

- $500,000 for the first location

- $10,000 for each additional location or authorized delegate

- Maximum cap: $1,500,000

The bond must be submitted electronically via NMLS from a surety company authorized to operate in Michigan. This bond protects customers and guarantees compliance with the MTSA. Expect to pay a premium of 0.5%–5% of the bond amount annually, depending on your financial profile and creditworthiness.

Net Worth and Financial Statements

Minimum net worth requirements scale with your footprint:

- $100,000 base for a single location

- Plus $25,000 per additional location or authorized delegate

- Maximum requirement: $1,000,000

You must submit financial statements covering the last two fiscal years. Statements may be unaudited if signed by an executive officer, though audited statements strengthen your application. If assets are pledged to meet net worth requirements, attach a detailed report of pledged assets.

AML/BSA Program

Your application must include a written Anti-Money Laundering (AML) / Bank Secrecy Act (BSA) policy. DIFS expects an operationally credible program, not a boilerplate policy. Your policy should demonstrate:

- Customer identification and verification procedures

- Transaction monitoring protocols

- Suspicious Activity Report (SAR) filing processes

- Currency Transaction Report (CTR) obligations

- Employee training requirements

- Independent testing and audit procedures

For early-stage companies without a full compliance team, Fraxtional's fractional BSA Officer services provide director-level oversight to build an AML/BSA program that meets DIFS expectations — without the overhead of a full-time hire.

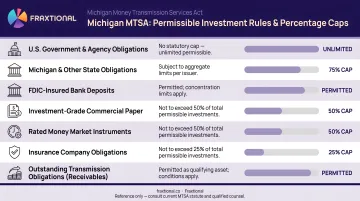

Permissible Investments

Under Sections 31–32 of the MTSA, licensees must hold permissible investments with a market value equal to or exceeding all outstanding payment liabilities at all times. Key rules:

- Authorized delegate receivables cannot exceed 20% of total permissible investments

- Receivables from a single delegate cannot exceed 10% of total permissible investments

- ACH and credit card receivables qualify as permissible investments under DIFS Order No. 2020-15-CF, subject to a 50% cap and a 5-business-day aging limit

How to Apply for a Michigan Money Transmitter License

All applications are submitted through NMLS, but the process doesn't stop there. Certain documents must also be mailed directly to the DIFS Consumer Finance Section at P.O. Box 30220, Lansing, MI 48909-7720. The four steps below cover everything from entity registration through post-approval obligations.

Step 1: Register Your Business Entity

Before applying, register your business with the Michigan Corporation Division. You'll need:

- Certificate of Authority or Good Standing dated no more than 60 days before filing

- Trade name registration if operating under a DBA

With entity registration confirmed, you can move directly into assembling the full document package DIFS requires.

Step 2: Prepare and Assemble Application Documents

Organize your full document package before starting the NMLS application. Required materials include:

- Business plan with detailed flow of funds

- Organizational chart showing ownership and control structure

- AML/BSA policy tailored to your operations

- Direct ownership verification (stock certificates or operating agreements)

- Internet security policy (required if conducting online business)

- Professional license lists for key personnel and any credit report explanations for derogatory items on MU2 forms

Critical: Incomplete applications reset DIFS's 120-day review clock. Treat the NMLS checklist as a pre-submission audit before you click submit.

Step 3: Submit Application and Pay Fees via NMLS

The fee structure is:

- $600 application fee (non-refundable)

- $3,050 license fee

- $50 per additional location

After submission, DIFS has 120 days to approve or deny your completed application. The clock starts only when DIFS determines your application is complete—missing documents restart the timeline.

Step 4: Post-Approval Obligations

Once approved, three ongoing requirements take effect immediately:

- Upload your authorized delegate list via the Uniform Authorized Agent Reporting (UAAR) system in NMLS

- Renew annually by December 1 — licenses expire December 31 each year

- Submit 30-day advance notice through NMLS for material changes: business address, name, ownership shifts exceeding 25%, or legal entity type changes (applicable fees apply)

Ongoing Compliance Obligations After Licensing

Maintaining your license requires continuous compliance, not just one-time approvals.

Quarterly MSB Call Report

You must file a Money Services Business Call Report quarterly through NMLS, due 45 days after each quarter-end. This report covers money transmission volumes and authorized delegate activity. Filing is mandatory even if there are no changes to report.

Authorized Delegate Management

If you operate through authorized delegates:

- Maintain written agreements with all delegates requiring MTSA compliance

- Provide delegates with compliance policies and procedures

- Submit quarterly UAAR updates through NMLS for any additions, deletions, or modifications to your delegate list

DIFS Examination and Investigation Authority

DIFS may examine the licensee and any authorized delegates. You must retain all financial records for a minimum of three years. Examination findings are generally confidential but may be shared with other regulatory bodies.

Continuous Compliance

Staying exam-ready means treating compliance as an ongoing program, not a checklist. Three obligations run continuously after licensing:

- BSA/AML program: Must be maintained and updated as your business evolves

- Permissible investments: Must continuously cover all outstanding payment obligations

- Material changes: Require advance notification to DIFS before implementation

For fintechs managing these obligations without a dedicated compliance team, Fraxtional's CCO and BSA Officer model provides director-level oversight at a fraction of a full-time hire's cost.

Common Misconceptions and Mistakes to Avoid

"Authorized Delegates Don't Need to Understand Compliance"

Authorized delegates don't need their own license, but they're far from exempt from compliance obligations. They must operate strictly within the licensed principal's scope, under a written agreement that mandates MTSA compliance. Delegates are subject to DIFS examination and must follow all policies and procedures the principal provides.

"Foreign Currency Exchange Is Excluded"

The MTSA does not apply to pure currency exchange activities. However, if your business also holds funds in an e-wallet or transmits money in any form, a license is required. The exclusion is narrow—most businesses that exchange currency also provide money transmission services.

Submitting Incomplete Applications

DIFS's 120-day review clock only starts when the application is determined complete. The most common documents that trigger delays include:

- AML/BSA policies (incomplete or missing entirely)

- Ownership verification documentation

- Credit explanations on MU2 forms

Treat the NMLS checklist as a mandatory pre-submission audit. An incomplete filing doesn't pause the clock — it resets it.

Frequently Asked Questions

How much does it cost to get a Michigan money transmitter license?

The application fee is $600 (non-refundable), the license fee is $3,050, and each additional location costs $50. You'll also pay an annual surety bond premium—typically 0.5%–5% of the required bond amount ($500,000–$1,500,000), depending on your financial profile.

Who needs a Michigan money transmitter license?

Any business providing money transmission services in Michigan must be licensed under the MTSA. This includes selling payment instruments, issuing prepaid access, and receiving money for transmission. Authorized delegates of a licensed entity are exempt from separate licensing.

What is the money transmitter law in Michigan?

The Money Transmission Services Act (2006 PA 250), codified under MCL § 487.1001–487.1047, governs money transmission in Michigan and is administered by the Michigan Department of Insurance and Financial Services (DIFS).

What is a licensed money transmitter?

DIFS approves licensed money transmitters to receive money or monetary value from customers and transmit it to recipients. Covered products include payment instruments, wire transfers, digital wallets, and prepaid access products.

What is an unlicensed money service business?

An unlicensed MSB operates without the required state license. In Michigan, doing so after December 31, 2006 violates the MTSA and can trigger enforcement action, fines up to $10,000 per day, and felony criminal charges.