Introduction

Many fintech startups, crypto firms, and payment platforms planning to operate in Colorado must clear a critical regulatory hurdle before accepting or moving customer funds: obtaining a money transmitter license. Operating without this authorization exposes companies to license revocation, civil penalties, and criminal misdemeanors.

The Colorado Money Transmitter License is a state-issued authorization required to legally conduct money transmission services in Colorado, regulated by the Colorado Division of Banking within the Department of Regulatory Agencies (DORA).

This guide is written for fintech startups, crypto exchanges, payment processors, embedded finance companies, and digital wallet providers preparing to enter the Colorado market. Colorado law classifies selling payment instruments, storing value, or transmitting money on behalf of consumers as regulated activity, so you cannot legally operate without DORA's approval.

Colorado enacted the Model Money Transmission Modernization Act (MTMA) via House Bill 25-1201, signed into law on April 18, 2025, with an effective date of August 6, 2025. If you've researched this license before, that matters: this legislation completely overhauled previous requirements, standardizing definitions, exemptions, and licensing procedures in alignment with 31 other states. Many existing guides are outdated — this article reflects the new MTMA framework.

Key Takeaways

- A Colorado Money Transmitter License is required for any company transmitting money, selling payment instruments, or storing value in the state—including crypto-based transmission under the 2025 MTMA

- Applications go through NMLS and require a minimum $250,000 surety bond (up to $1,000,000) and net worth of at least $100,000, scaling with total assets

- FinCEN MSB registration and a BSA/AML compliance program with independent review are also mandatory before approval

- Initial license fees are $6,000 if applying January 1–June 30, or $3,000 if applying July 1–December 31

- Colorado's MTMA allows multistate licensing coordination, simplifying the process for companies already licensed in other MTMA states

- Missing any document or compliance requirement is the most common reason for delays—plan for a thorough pre-application review

What Is a Colorado Money Transmitter License and Who Needs One?

Under Colorado's MTMA (C.R.S. § 11-110-201), a money transmitter is any person or entity that:

- Sells or issues payment instruments to a person located in Colorado

- Sells or issues stored value to a person located in Colorado

- Receives money for transmission from a person located in Colorado

This definition explicitly includes digital channels and extends well beyond traditional wire transfers.

Money transmitters vs. Money Services Businesses (MSBs): An MSB is the broader federal regulatory category defined by FinCEN at 31 CFR 1010.100(ff), covering currency dealers, check cashers, money order issuers, and other financial service providers. A money transmitter is a specific subset of MSBs focused on moving funds between parties—requiring its own state license in addition to federal MSB registration.

Who needs this license:

- Payment processors and remittance services

- Digital wallet providers storing customer funds

- Crypto platforms transmitting fiat or digital assets

- Payroll processing companies

- Embedded finance platforms facilitating customer-to-customer payments

- Payment instrument issuers (money orders, traveler's checks)

The 2025 MTMA update (HB 25-1201): Colorado repealed its legacy Money Transmitters Act and replaced it with the Model Money Transmission Modernization Act, which standardizes definitions, exemptions, and licensing procedures aligned with 27+ other MTMA states. This modernization includes multistate coordination mechanisms, updated net worth formulas, revised surety bond calculations, and clarified exemptions.

Agent-to-payee exemption: The MTMA codifies an important carve-out at C.R.S. § 11-110-301(1)(b). Certain intermediaries acting on behalf of payees are exempt from licensing if three conditions are met:

- A written agreement exists between the payee and agent

- The payee holds the agent out to the public as accepting payments on its behalf

- Payment is treated as received by the payee upon receipt by the agent, extinguishing the payor's obligation (meaning the payer is considered paid in full)

Merchant aggregators and payment facilitators are the most common business models that qualify — but the line between exempt intermediary and licensed transmitter is fact-specific and worth confirming early.

Understanding which exemptions apply to your model is especially relevant for crypto businesses, where Colorado's rules have specific nuances.

Are Crypto Exchanges Money Transmitters in Colorado?

Under Colorado's updated MTMA, digital money transmission is explicitly regulated. DORA's December 18, 2025 Interim Guidance draws a clear line between two scenarios:

| Scenario | License Required? |

|---|---|

| Receiving standard virtual currency for transmission | No — virtual currency doesn't meet the statutory definition of "money" |

| Selling or issuing payment stablecoins (per the GENIUS Act) | Yes — constitutes selling "stored value" |

| Federal Qualified Payment Stablecoin Issuer (FQPSI) | No — federal designation preempts state licensure |

Most crypto exchanges that transmit funds on behalf of users, facilitate fiat-to-crypto conversions, or issue stablecoins will need a Colorado MTL. If your platform touches stablecoins, confirm your FQPSI status before assuming you're exempt.

Colorado Money Transmitter License Requirements

Colorado's MTMA introduced new financial thresholds effective August 6, 2025. The legacy requirements ($50,000 base net worth, $1,000,000 minimum bond) no longer apply.

Financial Requirements

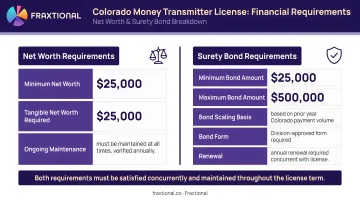

Minimum Net Worth:

- Greater of $100,000 OR:

- 3% of total assets for the first $100M

- 2% for assets between $100M and $1B

- 0.5% for assets over $1B

- Net worth must be calculated per GAAP

- Audited financial statements covering the most recent fiscal year and the two-year period immediately preceding submission are required

Surety Bond:

- Minimum bond: $250,000

- Maximum bond: $1,000,000

- The bond amount must equal the greater of $250,000 or 100% of the licensee's Average Daily Money Transmission Liability in Colorado

- The Banking Board can adjust bond requirements based on transaction volume, liquidity, and net worth risk factors

- Alternative: A combination of surety bond and permissible investments may be approved by the Banking Board, provided the bond floor remains at least $250,000

BSA/AML Compliance Program

Regulators scrutinize BSA/AML documentation more closely than almost any other part of the application. Applicants must submit:

- BSA/AML Policies and Procedures covering all federal requirements

- Independent Review of AML/BSA Program: an external audit or review confirming program effectiveness, not just a written policy document

- Compliance plan addressing federal AML, recordkeeping, and registration obligations

- Evidence of ongoing monitoring and employee training programs

This is where many applicants stumble. Incomplete or unreviewed compliance programs are a leading cause of application rejection or extended review times. Fraxtional's BSA Officer and compliance leadership services help money transmitters build and maintain audit-ready programs — without the cost of a full-time hire.

Background & Personnel Documentation

Each person in a control position must be individually vetted. Required documentation includes:

- Interagency Biographical and Financial Report (IBFR) for all individuals in control and key individuals

- Fingerprint cards for FBI background checks

- Five-year history of material litigation and criminal convictions for all directors, key shareholders, and executive officers

- Organizational chart showing ownership structure and reporting lines

Supporting Documents

- Business plan detailing your operations, target market, and revenue model

- History of operations (if applicable)

- Sample agent contracts (if you plan to authorize agents)

- Sample payment instrument forms

- List of proposed authorized agents in Colorado

- Clearing bank details and account information

- Copy of FinCEN MSB Registration (Form 107)

How to Apply for a Colorado Money Transmitter License: Step-by-Step

Colorado processes money transmitter license applications through the Nationwide Multistate Licensing System (NMLS), with the complete package submitted online and mailed to the Colorado Division of Banking alongside a fee check.

Step 1: Register Your Business in Colorado

Before initiating the license application, register your legal entity and trade name with the Colorado Secretary of State via the Colorado business portal (https://www.coloradosos.gov/).

Step 2: Register as an MSB with FinCEN

Register your company as a Money Services Business with the Financial Crimes Enforcement Network (FinCEN) through the BSA E-Filing System (https://bsaefiling.fincen.gov/). This federal registration is mandatory and must be completed before submitting the state license application. You must file FinCEN Form 107 within 180 days of establishing your business and renew every 24 months.

Step 3: Assemble Your Application Package

Complete the money transmitter application form via NMLS and compile all supporting documents:

- Audited financial statements

- Organizational chart

- BSA/AML program and independent review

- Background reports and fingerprint cards

- Surety bond documentation

- FinCEN registration confirmation

Missing documents are the most common cause of delays. DORA's NMLS checklist is comprehensive—review it carefully and ensure every item is included before submission.

Step 4: Obtain Your Surety Bond

Secure a surety bond of at least $250,000 (or qualify for the reduced option with permissible investments). Bond premiums typically run 1–3% of the face value annually, based on your company's credit profile. Get quotes from at least two surety providers before committing.

Step 5: Submit Your Application and Pay the Licensing Fee

Mail your complete application package to:

Colorado Division of Banking

1560 Broadway, Suite 975

Denver, CO 80202

Include a check payable to the Colorado Division of Banking:

- $6,000 if applying between January 1 and June 30

- $3,000 if applying between July 1 and December 31

Tip: Call DORA at 303-894-7575 after mailing to confirm receipt and track your application status.

Ongoing Compliance Obligations After Licensing

Obtaining your Colorado Money Transmitter License is just the beginning. Three core obligations govern your ongoing standing: quarterly reporting, record retention, and agent/consumer disclosure requirements.

Quarterly NMLS Reporting

All licensees must submit NMLS Money Service Business Call Reports within 45 calendar days after each calendar quarter end. This includes:

- Financial condition updates

- Transaction volume data

- Permissible Investment Report detailing how you are maintaining required reserves

Late filings trigger penalties and can jeopardize your license status.

Record Retention

Under the MTMA, record retention is standardized to 3 years for all required records, including:

- General ledgers and financial institution reconciliation records

- Transaction records

- Outstanding payment instrument records

- Agent lists and contracts

Records may be stored electronically and maintained outside Colorado, provided they are accessible to the Banking Board within 10 business days upon request.

Consumer Notices & Agent Reporting

Three additional requirements apply once you are licensed and operating:

- Consumer disclosures — Receipts and your website or mobile app must display the Division's name, phone number, and a statement that customers may file complaints directly with the Division.

- Agent reporting — Submit a report of authorized delegates within 45 days after each calendar quarter end via NMLS.

- Change of control — Any acquisition of control requires written Banking Board approval before the transaction closes; the Board has a 90-day review period.

Common Mistakes and Misconceptions About the Colorado MTL

"We can operate temporarily without a license while the application is pending."

False. Engaging in money transmission without a license, even temporarily or through an agent relationship, is a Class 2 misdemeanor under C.R.S. § 11-110-1105(2). The Banking Board can also assess civil penalties for each day the violation continues, plus investigation costs and attorney fees. The license covers the principal entity; agents are authorized under that license, but the licensee bears full compliance responsibility.

"FinCEN MSB registration is sufficient on its own."

No. FinCEN's official Form 107 instructions explicitly state: "Note: This registration does not satisfy any state or local licensing or registration requirements." Federal MSB registration and state money transmitter licensing are separate, complementary requirements. Both are mandatory.

"We can submit our internal AML policy and that's enough."

Not under Colorado's requirements. DORA's NMLS checklist strictly requires an Independent Review of AML/BSA Program, not just a written policy document. You need an external audit or independent assessment that demonstrates your program's effectiveness.

Submitting incomplete or unreviewed compliance programs is one of the leading causes of application rejection and extended review times.

These three misconceptions account for a disproportionate share of delayed or rejected Colorado MTL applications:

- Operating without a license while an application is pending is a Class 2 misdemeanor — not a gray area

- FinCEN MSB registration satisfies federal requirements only; Colorado licensing is a separate, mandatory obligation

- An internal AML policy alone does not meet DORA's checklist — an independent program review is required

Frequently Asked Questions

What qualifies as a money transmitter?

Under Colorado's MTMA, a money transmitter is any entity that sells or issues payment instruments, stores value, or transmits money—including digitally—on behalf of consumers for compensation.

What is the difference between a money service business and a money transmitter?

An MSB is the broader federal category covering activities like currency exchange, money orders, and check cashing. A money transmitter is a specific type of MSB focused on moving funds between parties, and it requires its own state license.

How do I register as an MSB?

MSB registration is a federal requirement completed through FinCEN's BSA E-Filing System at https://bsaefiling.fincen.gov/. You must finish this step before applying for a Colorado money transmitter license.

How hard is it to get a money transmitter license?

The main challenges are assembling a complete documentation package (especially the BSA/AML program with independent review), meeting net worth and bonding thresholds, and clearing background checks for all key personnel. Most applicants who prepare thoroughly get through it.

Are crypto exchanges money transmitters?

Under Colorado's updated MTMA, most crypto exchanges or platforms transmitting funds on behalf of users will need a Colorado Money Transmitter License. Specific exemptions may apply depending on business model—particularly around standard virtual currency versus payment stablecoins.

How to get a crypto license?

For crypto businesses transmitting funds in Colorado, the applicable license is the Money Transmitter License from DORA. It's obtained via the same NMLS application process, with the same bond, net worth, and BSA/AML requirements as any other money transmitter.