Introduction

Financial crime costs the global economy between $1.6 trillion and $4 trillion annually, according to IMF estimates — and regulators are running out of patience. In 2024, FinCEN assessed a record $1.3 billion penalty against TD Bank for willfully failing to monitor trillions in transactions. FINTRAC issued 12 Notices of Violation totaling over $26 million in penalties in the same year.

The problem isn't that financial institutions lack transaction monitoring (TM) systems. Most already have systems in place. The problem is poor calibration — systems generating enormous alert volumes while missing genuine suspicious activity.

For FinTechs, crypto firms, and emerging banks, this matters beyond regulatory risk. An underoptimized TM program generates false positives that consume analyst time, creates backlogs that delay SAR filings, and raises red flags with sponsor banks during due diligence reviews.

This article covers the practical strategies that move a TM program from technically compliant to genuinely effective: threshold calibration, customer segmentation, rule tuning, and SAR workflow improvement.

Key Takeaways

- Over 90% of TM alerts are false positives in most institutions — the problem is calibration, not volume

- Risk-based segmentation and regular tuning are essential complements to rule-based systems

- ML and advanced analytics can reduce false positives by 20–30% while cutting manual review workload by up to 50%

- Behavioral baselines and unified customer data consistently outperform arbitrary dollar thresholds

- TM optimization is an ongoing governance process, not a one-time configuration

Why Transaction Monitoring Optimization Is Now a Business Imperative

Optimization isn't a technology upgrade project. It directly affects regulatory standing, operational costs, and a firm's ability to detect actual financial crime.

The FCA fined HSBC £63.9 million for TM failures: inadequate scenario coverage, untested parameters, and incomplete data feeding into automated monitoring. FINTRAC penalized Exchange Bank of Canada for failing to file suspicious transaction reports and conduct ongoing monitoring of business relationships. Both firms had systems in place. What they lacked was the governance to make those systems work.

Cost pressure compounds the problem. LexisNexis Risk Solutions reported $61 billion in annual financial crime compliance costs across the US and Canada in 2023, with 70% of institutions identifying cost reduction as a priority. Reducing waste through better calibration — not weaker controls — is how institutions close that gap.

For growing FinTechs and crypto firms, the stakes compound quickly:

- Sponsor banks assess TM maturity before onboarding; weak frameworks can stall partnerships or trigger enhanced due diligence

- FinCEN, FCA, and FINTRAC each presume a risk-based, documented, and regularly reviewed program — not a static one

- Volume growth multiplies every calibration flaw: a 90% false positive rate at 10,000 transactions per month becomes unmanageable at 1 million

For scaling institutions, a poorly tuned TM program doesn't just create compliance risk — it actively blocks the partnerships and growth they're trying to build.

Common Pitfalls in Legacy and Underoptimized TM Systems

Legacy TM systems share recurring structural problems — and they rarely come down to the technology itself.

The False Positive Trap

McKinsey found that more than 90% of TM alerts are false positives, with only 1 or 2 out of every 100 alerts resulting in any action. Rule-based systems with static, one-size-fits-all thresholds are the primary cause — they flag legitimate transactions at the same rate as suspicious ones because they apply identical parameters across customers with vastly different risk profiles.

The consequence isn't just wasted analyst time. When every alert looks the same, genuine risk gets buried in noise.

Siloed Data

When KYC records, transaction history, account behavior, and external risk signals live in separate systems, compliance teams never see the full picture. A transaction that looks unremarkable in isolation may look very different alongside:

- A customer's onboarding profile and declared business purpose

- Prior alert history and disposition patterns

- Counterparty relationships and network-level risk signals

Without data integration, analysts are making judgment calls on partial evidence.

The "Set It and Forget It" Failure Mode

Many institutions configure TM rules at implementation and don't revisit them. ACAMS recommends reviewing monitoring models every 12 to 18 months — but that's a floor, not a ceiling.

As product lines expand, customer bases shift, and criminal typologies evolve, rules calibrated for an earlier version of the business stop catching what they were designed to find. The FCA's HSBC findings cited exactly this problem: failing to assess whether scenarios still covered current money-laundering risks.

Strategy 1: Rule Calibration, Threshold Tuning, and Scenario Development

Designing Rules That Reflect Actual Risk

Effective TM rules start with a clear understanding of the institution's specific risk profile — not templates borrowed from another institution's program. FATF's risk-based approach guidance requires that monitoring measures be commensurate with identified risks, which means rules must map to documented typologies relevant to the institution's actual business model, customer types, and geographies.

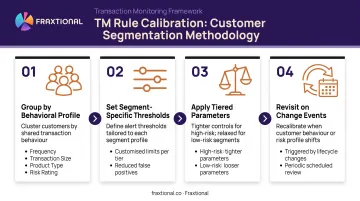

Customer segmentation is the most practical tool for reducing false positives without weakening detection:

- Group customers by behavioral profile — transaction frequency, average size, product type, and risk rating

- Set segment-specific thresholds rather than universal dollar amounts

- Apply tighter parameters to high-risk segments (PEPs, high-volume MSB clients, elevated-risk jurisdictions) while loosening thresholds on demonstrably low-risk behavior

- Revisit segmentation when new products launch or customer mix changes materially

Getting segmentation right is only half the equation. The other half is knowing when to act on what the data is telling you.

Trigger-Based Tuning vs. Calendar-Based Tuning

Traditional tuning on a fixed 12-to-18-month schedule creates drift — rules that were accurate when configured become less relevant as the business evolves. Trigger-based tuning uses live performance data to initiate rule reviews as needed.

Key metrics that should trigger a tuning review:

| Metric | What It Signals |

|---|---|

| Rule effectiveness ratio (escalated alerts ÷ total alerts) | Low ratio indicates poor calibration |

| SAR-to-alert conversion rate | Declining rate suggests rules are catching less relevant activity |

| Threshold clustering | High alert volume near a single threshold indicates poor calibration at that level |

| False positive rate spike | Any material increase warrants immediate review |

Once those metrics flag a review, deployment discipline matters. Back-test updated rules against historical transaction data before going live. Shadow testing — running new configurations in parallel with existing ones — prevents the common mistake of over-tightening thresholds and inadvertently suppressing legitimate suspicious activity.

Strategy 2: Leveraging AI, Machine Learning, and Advanced Analytics

Moving Beyond Static Rules

Static rules cannot detect what they weren't written to catch. Financial criminals adapt their patterns specifically to evade known thresholds — structuring transactions just below reporting limits, using multiple accounts to distribute activity, or rotating counterparties to avoid pattern detection.

Machine learning models trained on historical transaction data identify complex, non-obvious patterns that rule sets miss. More practically, they score alerts based on learned behavioral baselines rather than fixed dollar amounts. The system distinguishes between a customer doing something unusual yet consistent with their history versus a genuine deviation from expected behavior.

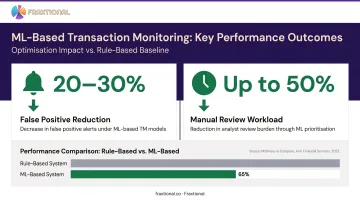

McKinsey reported that ML-based approaches can reduce false positive reports by 20% to 30% and cut manual investigative work by up to 50%. For compliance teams buried in alert queues, that's a direct reduction in investigator hours and review costs.

Advanced Analytics Use Cases in TM Optimization

Network analysis is one of the highest-value applications. Mapping relationships between accounts, entities, and counterparties surfaces patterns that single-transaction review cannot detect:

- Placement-and-layering sequences across multiple accounts

- Frequent interactions between related or shell entities

- Activity clusters associated with fraud rings or human trafficking

McKinsey's work on network analytics confirms its effectiveness in revealing hidden links that single-customer monitoring misses entirely.

Regulatory explainability is a hard requirement, not a best practice. FATF's 2021 guidance on new technologies for AML/CFT and the Wolfsberg Group's effective monitoring statement both require that ML models be explainable, validated, and governed. Institutions must be able to document:

- What the model was trained on

- How decisions are reached

- How model performance is validated over time

- How human review integrates with model outputs

For FinTechs and crypto firms working through fractional compliance leadership — such as a fractional BSA Officer or CAMLO through a firm like Fraxtional — this documentation work often happens in parallel with model deployment, ensuring regulatory readiness from the start rather than as an afterthought.

Strategy 3: Data Integration and Risk-Based Customer Segmentation

A TM system is only as good as the data feeding it. When KYC records, onboarding data, account activity, and external risk signals exist in separate systems that don't communicate, analysts lose the holistic view needed to accurately distinguish suspicious from legitimate activity.

Unified customer data enables:

- Detection of suspicious patterns that span multiple accounts or products

- Behavioral baselines per customer — what "normal" looks like for that specific entity

- Alerts triggered by genuine deviations rather than arbitrary thresholds

- Faster, better-informed investigative decisions

That integration also has direct regulatory implications. For crypto firms and FinTechs specifically, the FCA's cryptoasset registration requirements explicitly require firms to demonstrate configured transaction monitoring tools with rules and thresholds aligned to business-model risks — covering both fiat off-chain and cryptoasset on-chain activity. FATF's virtual asset guidance similarly expects ongoing monitoring that can be continuous and triggered by specific transaction types.

Real-time vs. batch processing is a practical decision point for growing institutions. Real-time monitoring is increasingly expected by regulators and sponsor banks for high-risk transaction types, but it requires data architecture that many early-stage firms don't yet have.

Batch processing works for lower-risk activities but creates real exposure for time-sensitive suspicious activity. Institutions should evaluate their current architecture honestly against their product risk profile, and document the rationale for whichever approach they use.

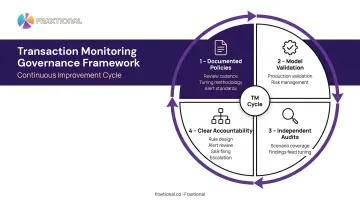

Building a Governance Framework for Continuous TM Improvement

Optimization is not a project with an end date. Without ongoing governance, even a well-designed TM system degrades as the business evolves.

A functional TM governance framework includes:

- Documented policies covering rule review cadence, tuning methodology, and alert disposition standards

- Model validation practices once TM is in production, consistent with model risk management expectations

- Regular independent audits that assess whether rules are detecting what they were designed to catch — findings should feed directly into the next tuning cycle

- Clear accountability for who owns each component: rule design, alert review, SAR filing, and escalation

The FCA's HSBC enforcement action makes this concrete. The failures weren't purely technical: HSBC failed to assess scenario coverage, conduct timely scenario risk assessments, test and update parameters, and verify data completeness. These are governance failures, not system failures.

FINTRAC requires a compliance effectiveness review at minimum every two years. FinCEN's BSA compliance advisory states that institutions must devote appropriate staffing based on their risk profile. Neither standard is met by a compliance program that exists on paper but isn't actively managed.

For many FinTechs, startups, and scaling crypto firms, meeting these standards requires compliance leadership that most founding teams haven't had to build before — deep knowledge of regulatory requirements, typology risk, and tuning methodology.

Fraxtional's fractional BSA Officers and CAMLOs provide named director-level accountability for daily monitoring, SAR/STR workflows, regulator and sponsor bank interactions, and ongoing program recalibration. The engagement is structured to deliver that leadership without the cost or commitment of a full-time executive hire.

Frequently Asked Questions

What is transaction monitoring optimization?

TM optimization is the ongoing process of refining rules, thresholds, data inputs, and workflows to improve detection accuracy and reduce false positives. The goal is keeping the system current with evolving financial crime typologies, regulatory requirements, and shifts in the institution's own business model.

How often should transaction monitoring rules be reviewed and updated?

At minimum quarterly, with comprehensive annual assessments. More frequent reviews are warranted when:

- New products launch or the customer base changes materially

- False positive rates spike above baseline

- Regulators issue updated guidance relevant to the institution's risk profile

What is the most common cause of high false positive rates in transaction monitoring?

Overly broad, static thresholds that don't account for customer risk segmentation or behavioral baselines. When all customers are monitored against the same dollar thresholds, legitimate transactions get flagged at the same rate as suspicious ones.

How does AI improve transaction monitoring compared to rule-based systems?

ML models learn from historical alert outcomes to detect non-obvious patterns, score alerts by actual risk level, and adapt as criminal tactics evolve. According to McKinsey, this reduces false positives by 20–30% and cuts manual investigative work by up to 50% — results static rules simply cannot replicate.

Do FinTechs and startups need dedicated compliance leadership to optimize transaction monitoring?

Yes. Effective TM optimization requires someone with fluency in regulatory requirements, typology risk, and tuning methodology — technology configuration alone isn't enough. Many FinTechs and startups meet this need through fractional compliance officers, gaining director-level expertise without a full-time hire.

What is trigger-based tuning in transaction monitoring?

Trigger-based tuning uses real-time performance metrics — false positive rates, SAR filing proximity to thresholds, alert escalation ratios — to initiate rule reviews as needed, rather than waiting for a fixed calendar schedule. It produces more responsive, data-driven calibration decisions.