Introduction

Regulatory pressure on financial institutions has never been more concentrated. FinCEN extracted a $1.3 billion penalty from TD Bank in 2024. The FCA fined Santander UK £107.7 million for persistent AML failures. FINTRAC handed Royal Bank of Canada a CAD $7.5 million administrative penalty. Each case traced back to the same root cause: inadequate compliance leadership.

An AML Compliance Officer is the senior professional accountable for designing, operating, and continuously improving an organization's anti-money laundering program.

This guide covers their core responsibilities, required skills, jurisdiction-specific title differences, and how companies at different stages (banks, fintechs, crypto firms) should think about structuring this function.

Whether you're hiring for the role, building out your AML program, or evaluating fractional alternatives to a full-time hire, this guide gives you a clear framework to act on.

TLDR

- The role is legally required in the US, UK, and Canada — title varies by jurisdiction: BSA Officer, MLRO, or CAMLO

- Core duties span AML program ownership, risk assessments, KYC/CDD oversight, transaction monitoring, SAR filing, and regulatory liaison

- Enforcement penalties run into billions — weak AML programs expose firms to fines, operational restrictions, and personal liability

- CAMS and CFCS are the primary credentials; the role demands regulatory knowledge, risk analysis, and board-level communication

- Early-stage fintechs and crypto firms increasingly use fractional AML officers to satisfy designation requirements cost-effectively

What Is an AML Compliance Officer?

An AML Compliance Officer is a senior compliance professional responsible for designing, overseeing, and continuously improving an organization's anti-money laundering program. The role spans applicable laws and regulatory frameworks — the BSA, FATF recommendations, EU AML directives — and must stay calibrated to the organization's own risk appetite.

Organizational Positioning

The AML CO typically sits within the compliance or risk function, reports directly to senior management or the board, and maintains independence from the business lines they oversee. That independence isn't optional — it's a specific regulatory expectation. An AML officer embedded within, or subordinate to, revenue-generating units creates a structural conflict that examiners will flag.

Title Variations by Jurisdiction

The role carries different designations depending on where the institution operates:

| Title | Jurisdiction | Regulatory Basis |

|---|---|---|

| BSA Officer | United States | 31 CFR 1020.210 |

| CAMLO (Chief Anti-Money Laundering Officer) | Canada | PCMLTFA / FINTRAC guidance |

| MLRO (Money Laundering Reporting Officer) | United Kingdom | MLR 2017, Regulation 21 |

| AML Compliance Officer | General / multi-jurisdiction | Organizational title, no single statute |

The designations vary by jurisdiction, but the core mandate is the same: prevent, detect, and report financial crime.

Why the AML Compliance Officer Role Is Critical

Regulators don't treat AML program ownership as optional. Under 31 CFR 1020.210, US banks must designate individual(s) responsible for coordinating and monitoring day-to-day BSA/AML compliance. The UK's MLR 2017 Regulation 21 requires firms to appoint both a senior compliance-responsible officer and a nominated officer. FINTRAC lists appointing a compliance officer as one of five mandatory elements of a Canadian compliance program.

The enforcement record shows what happens without adequate oversight:

- $3.4 billion — FinCEN's civil money penalty against Binance in 2023, accompanied by a five-year monitorship

- $1.3 billion — FinCEN's 2024 consent order against TD Bank

- £63.9 million — FCA fine against HSBC for deficient transaction monitoring controls

- CAD $9.2 million — FINTRAC's 2024 penalty against TD Bank Canada

Beyond fines, the consequences extend to operational restrictions. After Starling Bank's financial crime control failures, the FCA restricted the firm from opening new accounts for high-risk customers — a restriction Starling then breached, resulting in over 54,000 accounts opened for approximately 49,000 high-risk customers.

The Strategic Dimension

Those penalties reflect a narrow slice of the actual exposure. The AML CO shields the institution from regulatory breach while protecting the broader financial system from money laundering, terrorist financing, and sanctions evasion — and the scale of the threat keeps growing. Chainalysis reported $40.9 billion received by illicit crypto addresses in 2024, with estimates suggesting the true figure may be closer to $51 billion.

That context has fundamentally changed the role. The AML CO is no longer a back-office function signing off on reports — they're now a strategic risk advisor shaping product decisions, onboarding design, and cross-border expansion strategy before problems reach the regulators.

Key Responsibilities of an AML Compliance Officer

The AML CO carries both strategic and operational accountability across five core functions — each one a building block of the institution's financial crime defense.

Developing and Maintaining the AML Program

The AML CO owns a written program covering policies, procedures, internal controls, and governance structures — tailored to the organization's risk profile, products, customer base, and geographic footprint. This isn't a one-time build. The program requires ongoing updates to reflect:

- Regulatory changes and new guidance

- New product launches or business model changes

- Lessons from internal audits or external examination findings

- Emerging financial crime typologies

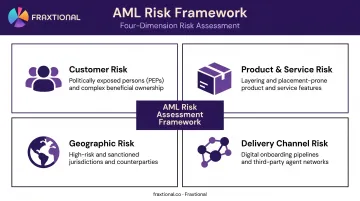

Conducting AML Risk Assessments

Risk assessments drive everything else. The AML CO evaluates exposure across four dimensions, as outlined in FCA FCG 3.2 and aligned with FATF Recommendation 1:

- Customer risk — PEPs, high-risk industries, complex ownership structures

- Product and service risk — features that could be exploited for layering or placement

- Geographic risk — customers or transactions involving high-risk jurisdictions

- Delivery channel risk — digital onboarding, agent networks, third-party channels

Examiners verify the risk assessment first. Disproportionate or ineffective controls trace back to a weak one almost every time.

KYC, CDD, and Enhanced Due Diligence Oversight

The AML CO governs the customer onboarding process, ensuring Know Your Customer (KYC), Customer Due Diligence (CDD), and Enhanced Due Diligence (EDD) procedures are applied consistently — particularly for higher-risk relationships such as:

- Politically exposed persons (PEPs)

- Customers with complex beneficial ownership structures

- Relationships involving high-risk jurisdictions

Oversight extends beyond onboarding. Ongoing KYC refresh and periodic remediation fall under this function, and the AML CO must ensure customer risk profiles are reviewed and updated throughout the relationship lifecycle.

Transaction Monitoring and SAR Filing

The AML CO oversees the transaction monitoring function — ensuring detection rules, alert thresholds, and investigation workflows are calibrated to the institution's risk profile. The goal is timely identification of suspicious activity without generating excessive false positives that overwhelm investigation teams.

SAR/STR filing obligations attach directly to this role:

- US: SARs must be filed with FinCEN no later than 30 calendar days after initial detection, with a possible 30-day extension if no suspect is identified (31 CFR 1020.320). FinCEN recorded 4.7 million SARs in FY2024, averaging 12,870 filings per day

- UK: Nominated officers must file with the NCA as soon as practicable after relevant information comes to them (POCA 2002, section 331). The UKFIU received 872,048 SARs in 2023-2024

- Canada: STRs must be submitted to FINTRAC as soon as practicable after reasonable grounds to suspect are established

In all jurisdictions, tipping off (disclosing that a SAR has been filed or is under consideration) is a criminal offense. The AML CO must maintain strict confidentiality throughout.

Staff Training, Regulatory Liaison, and Control Testing

Regulators assess training adequacy and compliance culture during every examination. This subsection covers the three outward-facing responsibilities that complete the AML CO's mandate:

- Staff training — Role-based programs equip front-line staff to recognize red flags, understand reporting obligations, and escalate concerns. Frequency and content are standard examination checkpoints.

- Regulatory liaison — The AML CO serves as the primary contact for regulators, supervisory authorities, and law enforcement, managing examinations, responding to inquiries, and coordinating remediation of identified deficiencies.

- Control testing — Conducted in partnership with internal audit, ongoing testing validates program effectiveness and surfaces gaps before examiners do.

Essential Skills and Qualifications

Technical Knowledge

Strong AML officers combine regulatory depth with practical application:

- Jurisdiction-specific AML laws: BSA/USA PATRIOT Act, UK POCA/MLRs, Canadian PCMLTFA

- FATF recommendations and risk-based approach methodology

- KYC/CDD frameworks and EDD triggers

- SAR/STR filing requirements and tipping-off rules

Professional certifications signal demonstrated competence. ACAMS describes CAMS (Certified Anti-Money Laundering Specialist) as the global AML competency benchmark, recognized by institutions, governments, and regulators worldwide. The CFCS (Certified Financial Crime Specialist) from ACFCS covers the broader financial crime spectrum and is increasingly valued for roles spanning fraud, corruption, and sanctions alongside AML.

Analytical and Investigative Skills

AML work requires making evidence-based decisions under pressure, often with incomplete information. Specific capabilities include:

- Interpreting transaction patterns across large datasets

- Assessing complex risk scenarios involving multiple entities or jurisdictions

- Identifying anomalies that warrant investigation or escalation

- Documenting findings clearly enough to withstand regulatory scrutiny

Leadership and Communication

The AML CO operates at the intersection of legal obligation and business operations. That requires a specific communication range most technical roles don't demand:

- Presenting program gaps and risk findings to the board in plain language

- Engaging examiners with credibility and thoroughness during regulatory reviews

- Influencing business units to adopt controls without becoming a bottleneck

- Translating dense regulatory requirements into guidance teams can actually follow

Officers who do this well rarely generate MRAs for inadequate BSA programs — because examiners leave with confidence the program is understood and owned at the top.

AML Compliance Officer vs. MLRO vs. BSA Officer: Key Differences

These titles are frequently used interchangeably, but they carry jurisdiction-specific meaning and distinct legal obligations. The table below maps each title to its legal basis and primary obligation.

| Role | Jurisdiction | Legal Basis | Primary Obligation | Legally Required? |

|---|---|---|---|---|

| BSA Officer | US | 31 CFR 1020.210 | Coordinate and monitor day-to-day AML compliance | Yes (banks) |

| CAMLO | Canada | PCMLTFA / FINTRAC guidance | Implement all elements of the compliance program | Yes (reporting entities) |

| MLRO | UK | MLR 2017, Reg 21; POCA 2002, s.331 | Review internal disclosures; file SARs with NCA | Yes (regulated firms) |

| AML Compliance Officer | General | Organizational | Oversee AML framework, governance, and controls | Best practice / varies |

The AML CO vs. MLRO Distinction

This matters most in UK-regulated entities. The AML Compliance Officer oversees the overall framework, governance, and controls. The MLRO holds a specific statutory obligation: reviewing internal suspicious activity disclosures and deciding whether to file an external SAR with the NCA.

Under POCA 2002 section 331, failure to disclose where required is a criminal offense. That makes the MLRO designation a position of genuine personal legal accountability — not just a title.

In smaller firms, one person typically holds both designations. Larger institutions may separate them for independence, with the MLRO focused on disclosure decisions and the AML CO handling broader program governance.

Multi-Jurisdictional Complexity

Fintechs, crypto firms, and embedded finance companies operating across borders may need to satisfy BSA Officer, CAMLO, and MLRO requirements simultaneously. Each jurisdiction adds its own layer of obligation:

- Separate filing timelines — SAR deadlines and formats differ between FinCEN, FINTRAC, and the NCA

- Different regulatory contacts — each regulator has distinct escalation paths and expectations

- Distinct staffing requirements — some jurisdictions require named, designated individuals on record

This compounds both compliance complexity and staffing costs — which is why the fractional model has gained traction among cross-border operators.

Full-Time vs. Fractional AML Compliance Officer: What's Right for Your Business?

Not every regulated entity has the budget or workload to justify a full-time AML officer. A senior BSA Officer in the US earns between $96,000 and $169,000 in total pay (per Glassdoor benchmarks), while a Head of Financial Crime or MLRO in the UK commands approximately £150,000–£300,000 according to Barclay Simpson's 2025 salary guide. Add benefits, management overhead, and compliance infrastructure, and the full-time model becomes a significant commitment for early-stage companies.

What the Fractional Model Provides

A fractional AML Compliance Officer delivers director-level expertise on a part-time or advisory basis — embedded into the organization's operations, available to represent the firm before regulators and the board, and scalable as the business grows. The FCA has confirmed that smaller firms may propose part-time or fractional MLROs, and that it has sometimes accepted this arrangement, provided accountability remains clear.

The fractional model is particularly suited to:

- Seed to Series B fintechs building their first compliant AML program

- Crypto firms navigating FinCEN registration, FINTRAC obligations, or FCA authorization

- Companies needing to satisfy a sponsor bank's BSA Officer requirement ahead of go-live

- Multi-jurisdictional operators requiring simultaneous BSA Officer, CAMLO, and MLRO coverage

How Fraxtional Structures This

Fraxtional provides fractional compliance leadership — including named BSA Officer, CAMLO, and MLRO services — to fintechs, banks, crypto firms, and embedded finance companies across the US, UK, and Canada.

The Fractional Advisory model includes a named Director, board-level reporting, and direct representation before regulators, auditors, and sponsor banks. It's designed for firms that need the accountability of a designated officer without a full-time hire.

Three engagement models are available depending on the firm's stage and needs:

- On Demand Advisory — flat fee for discrete projects (risk assessments, policy builds, sponsor bank introductions)

- Subscription Advisory — monthly or weekly retainer with a dedicated Director for ongoing support

- Fractional Advisory — monthly retainer with named title use; the most cost-effective model for long-term designated officer requirements

In practice, one crypto wallet co-founder found that an existing AML policy failed a sponsor bank review; Fraxtional corrected the framework within days and prevented an onboarding delay. A Series B fintech CEO reported that the fractional model delivered more expertise at a lower cost than a full-time hire, with the Director supporting sponsor bank discussions directly.

For companies navigating licensing processes, regulatory examinations, or enforcement responses, Fraxtional's Directors can be named on regulatory filings and assume immediate accountability as the responsible compliance executive.

Frequently Asked Questions

What is an AML compliance officer?

An AML compliance officer is a senior professional responsible for designing and overseeing a financial institution's anti-money laundering program. They ensure the organization detects, prevents, and reports money laundering and financial crime in line with applicable laws and regulatory requirements across their operating jurisdictions.

What are the key responsibilities of an AML compliance officer?

Core duties include developing AML policies and procedures, conducting risk assessments, overseeing KYC/CDD processes, managing transaction monitoring, filing SARs/STRs, training staff, and liaising with regulators. The scope and depth of each responsibility varies by institution size, product complexity, and risk profile.

What is the difference between an AML compliance officer and an MLRO?

The AML Compliance Officer oversees the overall compliance framework, governance structure, and controls program. The MLRO holds a specific statutory responsibility under UK law: reviewing internal suspicious activity disclosures, deciding whether to file an external SAR with the NCA, and accepting personal criminal liability for failure to disclose — a distinction that matters most in FCA-regulated entities.

What qualifications does an AML compliance officer need?

Most roles require a background in compliance, finance, law, or banking, combined with professional certifications such as CAMS (from ACAMS) or CFCS (from ACFCS). Practical experience with AML risk frameworks, regulatory examinations, and financial crime typologies carries as much weight as credentials in most hiring decisions.

Do fintech startups and crypto firms need a dedicated AML compliance officer?

Most regulated entities — including fintechs and crypto firms — are legally required to designate an AML officer under BSA (US), PCMLTFA (Canada), or UK MLRs. Early-stage companies commonly satisfy this requirement through fractional compliance leadership, which provides the necessary regulatory accountability at a fraction of the full-time cost.

What happens if a company doesn't have an AML compliance officer?

Operating without a designated AML officer where one is required exposes the institution to enforcement actions, fines, license restrictions, and reputational damage. Regulators may also hold senior management personally accountable for AML program deficiencies — and personal liability for executives is a documented enforcement outcome, not just a policy warning.