For fintechs, crypto firms, money transmitters, and BaaS participants at seed or growth stages, the practical question isn't whether to comply — it's how to build a credible, defensible compliance function without the overhead of a full compliance department.

Managed AML services exist to answer that question. This article covers what they are, what they include, who they're right for, and what to evaluate before choosing a provider.

Key Takeaways

- Managed AML services mean outsourcing compliance functions — monitoring, investigations, CDD, and regulatory reporting — to a specialized provider

- Core functions typically span KYC/CDD, transaction monitoring, alert review, SAR/STR filing, and sanctions screening

- Key advantages: operational scalability, access to deep regulatory expertise, and improved audit readiness without growing headcount

- The spectrum runs from analyst-level operational support to fractional BSA Officers, MLROs, and CAMLOs with full named accountability

- Provider selection hinges on jurisdictional depth, leadership level, QA practices, and engagement flexibility

What Are Managed Services for AML Compliance?

Managed AML services involve outsourcing part or all of an organization's anti-money laundering compliance operations to a specialized third-party provider. That includes the functions — transaction monitoring, investigations, customer due diligence, regulatory reporting — that would otherwise require dedicated in-house staff.

The key distinction from buying AML software is that managed services deliver people, processes, and workflows, not just technology. Engagements operate under defined service-level agreements covering turnaround times, quality standards, and accountability mechanisms.

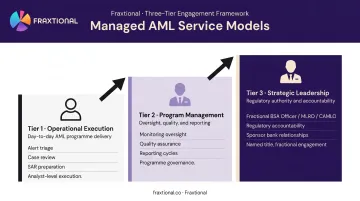

The Spectrum of Service Models

The range of what providers actually offer spans three distinct tiers:

- Operational execution — Teams of analysts handling alert triage, case review, and SAR preparation

- Program management — Compliance managers overseeing monitoring programs, QA, and reporting cycles

- Strategic leadership — Fractional BSA Officers, MLROs, or CAMLOs who own the AML program, carry named regulatory accountability, and manage relationships with regulators and sponsor banks

The difference between a provider supplying analyst capacity and one deploying a credentialed fractional BSA Officer is significant. Both are "managed services," but they carry very different levels of ownership and regulatory defensibility.

How This Differs from BPO

Business Process Outsourcing typically transfers routine, repeatable tasks to a lower-cost provider focused on volume and efficiency. Managed AML services are different — the provider takes ongoing ownership of compliance outcomes, not just task execution. That distinction matters when a regulator asks who is accountable.

Accountability pressure is only part of the story — cost pressure is driving the shift too. UNODC estimates that money laundering represents 2–5% of global GDP annually, roughly $800 billion to $2 trillion, though the clandestine nature of financial crime makes precise figures difficult to pin down.

Meanwhile, LexisNexis Risk Solutions reported that financial crime compliance costs for US and Canadian firms reached $56.7 billion in 2022, up 13.6% year over year. That trajectory is pushing organizations toward more efficient delivery models.

What Does a Managed AML Compliance Service Include?

A comprehensive managed AML service typically covers these core components:

Customer Due Diligence and KYC

Under FinCEN's CDD Final Rule, covered institutions must identify and verify beneficial owners of legal entity customers, including natural persons owning 25% or more. In practice, this means:

- Collecting and verifying customer identity at onboarding

- Assigning risk ratings based on customer profile, geography, and transaction type

- Screening against sanctions lists and PEP databases

- Triggering enhanced due diligence or periodic reviews when risk factors change

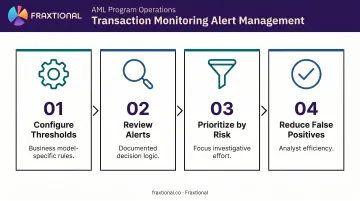

Transaction Monitoring and Alert Management

Monitoring systems generate alerts based on risk-based rules and detection scenarios. The managed service handles:

- Configuring thresholds and detection logic suited to the client's specific business model

- Reviewing generated alerts with documented decision logic

- Prioritizing alerts by risk level to focus investigative effort where it matters

- Reducing false positive volume that burns out in-house analysts

Case Investigation and SAR/STR Filing

When alerts escalate to cases, specialist analysts examine transaction histories, customer behavior, and external data to determine whether activity meets the suspicion threshold. The jurisdictional naming conventions matter here:

| Jurisdiction | Report Name | Volume (Latest) |

|---|---|---|

| United States | SAR (filed to FinCEN) | 4.7 million in FY2024 |

| United Kingdom | SAR (filed to NCA/UKFIU) | 850,000+ per year |

| Canada | STR (filed to FINTRAC) | 633,882 in 2024–25 |

Full case files are prepared with supporting evidence and filed in line with jurisdictional standards: BSA in the US, POCA in the UK, and PCMLTFA in Canada.

Ongoing Monitoring and Regulatory Reporting

Beyond transaction review, managed services also cover:

- Adverse media screening and sanctions rescreening

- Risk score updates triggered by new customer information

- Performance reporting delivered to compliance leadership under SLA tracking

- Audit-ready documentation for each case and filing

Strategic Compliance Leadership

Operational execution only goes so far. More comprehensive engagements include fractional BSA Officers, MLROs, or CAMLOs who own program oversight, regulatory relationships, and policy development alongside the day-to-day work. These roles can be named on regulatory filings and interact directly with sponsor banks and regulators on the organization's behalf.

Fraxtional, for example, deploys director-level BSA Officers, MLROs, and CAMLOs who embed directly into client operations and assume named accountability across monitoring, SAR/STR workflows, and case governance. The model gives organizations access to experienced compliance leadership without carrying a full-time executive on headcount.

The Key Benefits of Outsourcing AML Compliance

Scalability Without Headcount Risk

Alert volumes don't arrive in neat, predictable patterns. Remediation events, new product launches, and rapid customer growth all create surges that a fixed internal team struggles to absorb. Managed services allow organizations to expand capacity quickly — or pull back — without committing to permanent hires.

This flexibility is particularly valuable for fintechs experiencing rapid growth or entering new regulated markets.

Access to Specialized Expertise

Effective AML compliance requires hands-on familiarity with multiple regulatory frameworks: BSA/AML for US operations, FCA expectations for UK-regulated firms, FINTRAC requirements in Canada, FATF standards for international activity. Few startups or Series A companies can staff that depth in-house — and fewer can afford to.

Managed providers carry this expertise as part of their core offering. Fraxtional's team holds ACAMS certifications and specialized credentials in digital asset compliance, covering the full range of frameworks clients encounter across jurisdictions.

Cost Control and Budget Predictability

The US Bureau of Labor Statistics reported a median annual wage of $78,420 for compliance officers in May 2024, with the top 10% earning above $130,030. But salary is only part of the cost. The full picture includes:

- Recruiting and onboarding costs

- Ongoing training and certification

- QA coverage during peak periods

- Continuity risk when staff turns over

Managed service pricing — whether fixed-fee, subscription, or retainer — replaces that unpredictable cost structure with a defined, controllable budget line.

Improved Audit Readiness

Structured documentation, standardized case files, and SLA-tracked reporting create a complete, defensible audit trail. When a regulator or sponsor bank asks for documentation, the records are organized and available — not assembled reactively from scattered files.

In 2024, the OCC entered a formal agreement with Axiom Bank, N.A. following BSA/AML violations. The order required a SAR look-back covering 18 months and mandated controls confirming that third parties performing BSA/AML functions receive sufficient ongoing training. Documented oversight of third-party BSA/AML functions is now an explicit regulatory expectation — not a best practice.

Managed AML Services vs. Building In-House: Which Is Right for You?

The honest answer depends on your stage, transaction volume, and regulatory obligations — not a universal rule.

In-house teams offer maximum control and institutional knowledge. They make sense when:

- Compliance is a core differentiator for your business model

- Transaction volumes are large and predictable

- The business can justify a full function with dedicated leadership, analysts, QA, and coverage

Managed services are the stronger fit when:

- Alert volumes are variable or unpredictable

- The company is entering a new regulated market without established compliance infrastructure

- A credentialed BSA Officer, CAMLO, or MLRO is required to satisfy sponsor bank or regulator requirements — and a full-time executive salary isn't justified

- The organization is at seed or Series A stage and needs expert compliance leadership without a permanent hire

Common triggers Fraxtional sees in practice:

- A sponsor bank requiring a named BSA Officer before going live

- An audit or examination revealing gaps in an existing AML framework

- A funding round where investor due diligence surfaces compliance readiness as a concern

The Hybrid Model

Many organizations land somewhere in between — retaining a lean internal compliance function for governance and strategy while outsourcing operational execution or supplementing with fractional leadership. This preserves institutional knowledge while accessing external scale and specialist depth.

For organizations navigating this middle ground, Fraxtional's engagement models are built for exactly this path. Clients typically progress through three stages as their regulatory obligations mature:

- On Demand Advisory — a discrete AML review or gap assessment

- Subscription Advisory — an ongoing retainer during a growth or pre-audit phase

- Fractional Advisory — a named BSA Officer, CAMLO, or MLRO with full title use and dedicated oversight

Risks and Considerations When Using Managed AML Services

Regulatory Accountability Cannot Be Outsourced

This is the most important point in this entire article. The OCC is explicit: engaging a third party does not remove a bank's responsibility to comply with applicable law. FINTRAC similarly confirms that a service provider may submit reports, but the reporting entity remains ultimately responsible.

When Fraxtional provides a fractional BSA Officer or MLRO, those executives assume named, personal accountability for the compliance function: they can appear on regulatory filings and manage regulator interactions directly. The client organization, however, retains ultimate legal responsibility for its AML program.

That distinction matters when selecting a provider. Weak case management, poor documentation, or missed escalations by the vendor become your regulatory exposure — not theirs.

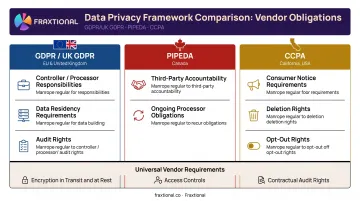

Data Privacy and Security

Transferring customer PII and transaction data to a third party creates obligations across multiple frameworks:

- GDPR/UK GDPR — controller/processor responsibilities, data residency, and audit rights

- PIPEDA (Canada) — organizations remain accountable for personal information transferred to third parties for processing

- CCPA (California) — consumer notice, deletion, and opt-out rights

Before signing, organizations should confirm encryption in transit and at rest, data residency agreements, access controls, and contractual audit rights over vendor systems.

Quality Consistency and Vendor Governance

High analyst turnover, inconsistent case review standards, and inadequate QA frameworks are where managed AML programs most commonly break down. Before engaging any provider, ask specifically about:

- QA sampling rates and how case feedback is delivered

- Escalation procedures when cases reach suspicion threshold

- Performance reporting cadence and SLA terms

- How quickly the provider can scale capacity up or down

What to Look for in a Managed AML Compliance Provider

Regulatory Depth and Jurisdictional Coverage

The provider should demonstrate hands-on experience with the specific frameworks that govern your business. That means knowing the difference between BSA obligations for a US money transmitter, FCA registration requirements for a UK cryptoasset firm, FINTRAC MSB obligations in Canada, and EU AMLR requirements for CASPs. Generic "global compliance" claims aren't sufficient — ask for specifics.

Leadership Level and Named Accountability

There's a meaningful difference between a provider supplying analyst capacity and one delivering director-level compliance leadership. For organizations that need a credentialed BSA Officer, CAMLO, or MLRO to satisfy regulatory or sponsor bank requirements, the engagement must include named leadership.

Fraxtional's fractional compliance model provides director-level BSA Officer, MLRO, and CAMLO services that sit inside your existing team structure. Every client engagement is Director-led. Clients work directly with that Director — not a junior analyst — which matters when a sponsor bank is asking questions or a regulator is reviewing your program.

Engagement Flexibility and QA Practices

The right provider should be able to grow with you. Specific questions to ask:

- Can the engagement model flex from short-term advisory to ongoing fractional leadership?

- What does QA sampling look like, and how are case-level feedback and corrections handled?

- What happens when an analyst leaves — is there a documented knowledge transfer process?

- Can you audit the provider's work product, not just receive summary reports?

If a provider hesitates on any of these, that's the answer. Strong providers have documented processes for each — not because they expect problems, but because accountability is built into how they operate.

Frequently Asked Questions

What are AML managed services?

AML managed services involve outsourcing some or all anti-money laundering compliance functions to a specialized third-party provider. The provider delivers people, processes, and defined workflows under service agreements — covering transaction monitoring, case investigations, customer due diligence, and regulatory reporting — rather than simply supplying software.

What is the difference between an MSP and BPO?

A Managed Services Provider takes ongoing ownership of a compliance function with defined quality standards and accountability for outcomes. Business Process Outsourcing transfers routine, repeatable tasks to a lower-cost provider without the same level of specialized expertise or program-level responsibility.

What is an example of a managed AML service?

One common model is a fintech outsourcing SAR filing, transaction monitoring alert review, and KYC to a specialized provider. A more embedded approach is retaining a fractional BSA Officer who owns the AML program, appears on regulatory filings, and manages sponsor bank relationships part-time.

Who needs managed AML compliance services?

Managed AML services suit fintechs, crypto firms, money transmitters, and embedded finance companies that carry regulatory obligations but can't justify a full in-house compliance team. This is especially common at seed, Series A, and rapid-growth stages.

Is AML compliance mandatory for fintechs?

Yes. AML obligations apply to most fintechs operating in the US, UK, Canada, and EU — including money transmitters, crypto firms, payment processors, and embedded finance platforms. Requirements vary by jurisdiction and license type, but the core obligations to know your customer, monitor activity, and report suspicion are consistent across all major markets.