Introduction

Traditional KYC operates on a schedule. A customer gets reviewed at onboarding, then again in one, three, or five years depending on their risk tier. That gap is where risk hides.

A business owner can sell their stake to a politically exposed person. A customer can appear on an updated sanctions list. Transaction patterns can shift dramatically. None of these changes trigger a review under the periodic model — they just sit undetected until the next scheduled check rolls around.

Global financial crime compliance costs reached $213.9 billion in 2021, up from $180.9 billion the year prior. That figure reflects how much the industry is already spending — and how much is at stake when controls fail.

Perpetual KYC (pKYC) addresses this by monitoring customer data continuously and triggering updates when something meaningful changes — rather than waiting for a scheduled review cycle. This guide covers:

- What pKYC means and how it differs from periodic KYC

- The core benefits and what triggers a review

- Real implementation challenges

- How to build a program that actually works

Key Takeaways

- pKYC monitors and updates customer risk profiles continuously, not on a fixed review schedule

- Reviews are event-driven — triggered by sanctions hits, ownership changes, or unusual transactions — not by the calendar

- Done well, pKYC strengthens AML compliance, catches fraud earlier, and cuts both operational overhead and customer friction

- The real implementation hurdles are data quality, false positive fatigue, and fitting pKYC into legacy tech stacks

- Technology enables pKYC, but expert compliance leadership is what makes it governable and defensible

What Is Perpetual KYC?

Perpetual KYC (pKYC) is a continuous customer due diligence process where customer identity, behavior, and risk data are monitored and updated on an ongoing basis — not on a fixed cycle. ACAMS defines it as maintaining accurate client data through near-real-time updates based on changes in client behavior and circumstances.

How It Works

pKYC relies on automated data feeds and monitoring logic to watch for signals across multiple data sources. When a meaningful signal appears, the system either updates the customer's risk profile automatically or triggers a compliance review.

Common signals include:

- Adverse media hits or negative news coverage

- Sanctions list additions or updates

- Changes to business ownership or director structure

- Unusual transaction patterns deviating from expected activity

- Customer-reported updates such as a new address or legal name

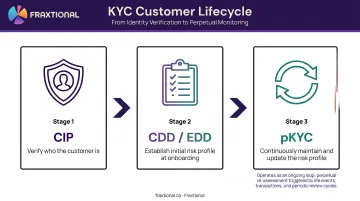

Where pKYC Fits in the Customer Lifecycle

pKYC does not replace onboarding due diligence. The sequence is:

- CIP (Customer Identification Program) — verifies who the customer is

- CDD/EDD — establishes the initial risk profile at onboarding

- pKYC — maintains and updates that profile continuously once the account is active

pKYC is the ongoing maintenance layer, not the foundation. It keeps the baseline risk profile accurate between formal reviews and works alongside CDD and EDD — it doesn't replace them.

Why It's Gaining Traction Now

Regulatory enforcement is a major driver. FATF Recommendation 10 requires financial institutions to conduct ongoing due diligence throughout the customer relationship, not just at onboarding. The EU's AMLD4 and FinCEN's CDD Rule carry similar expectations. As regulatory scrutiny has intensified, periodic review cycles alone no longer satisfy examiners — and the compliance costs of getting it wrong have made the case for continuous monitoring difficult to ignore.

Perpetual KYC vs. Periodic KYC

How Periodic KYC Works

Under a periodic model, customers are classified by risk tier at onboarding and reviewed on a fixed schedule — typically annually for high-risk customers, every three to five years for medium and low-risk tiers. The core weakness: risk profiles change faster than review cycles. By the time a scheduled review runs, the underlying information may already be months out of date.

ACAMS describes periodic KYC as a legacy operating model built around one-, three-, and five-year refresh cycles — framing pKYC as a continuum rather than a remediation cycle.

Side-by-Side Comparison

| Dimension | Periodic KYC | Perpetual KYC |

|---|---|---|

| Review frequency | Fixed schedule (annual / 3–5 years) | Event-driven (when something changes) |

| Risk detection speed | Slow — gaps can span years | Near real-time |

| Resource burden | Heavy batch processing at review time | Continuous, lower per-event cost |

| Customer friction | Blanket re-verification requests | Targeted outreach only when needed |

| Regulatory alignment | Baseline compliant | Aligned with FATF, AMLD, FinCEN expectations for ongoing monitoring |

| Risk profile accuracy | Snapshot at point of review | Living, continuously updated record |

The Role of Periodic Reviews in a Hybrid Model

Periodic KYC doesn't disappear entirely in a pKYC program. Scheduled reviews still serve a purpose as audit checkpoints. In a hybrid model, those checkpoints typically cover:

- Validating that automated risk decisions are producing accurate outcomes

- Confirming documentation is complete and current

- Verifying the pKYC system itself is functioning as intended

The reviews become lighter and more targeted — focused on exceptions, not the entire customer base.

Key Benefits of Perpetual KYC

Stronger Risk Detection and Earlier Intervention

Periodic checks leave detection windows — sometimes years long — where a customer's risk profile can escalate without anyone noticing. pKYC closes those windows by updating profiles the moment a relevant event is detected.

Concrete examples of what pKYC catches early:

- A business changes ownership to a politically exposed person (PEP) mid-relationship

- A customer appears on an updated OFAC or EU sanctions list between scheduled reviews

- Transaction volumes or patterns shift in ways inconsistent with the customer's stated business purpose

The FCA's £28.9 million fine against Starling Bank in 2024 illustrates the enforcement risk here. The FCA found that Starling had not screened customers against the full list of sanctioned individuals and entities — a controls failure that ongoing, event-driven monitoring is specifically designed to prevent.

Because pKYC is event-driven, compliance resources concentrate on customers where something has actually changed. Risk decisions become more targeted and evidence-based, rather than spreading analyst time evenly across a portfolio on a fixed schedule.

Reduced Compliance Gaps and Better Regulatory Alignment

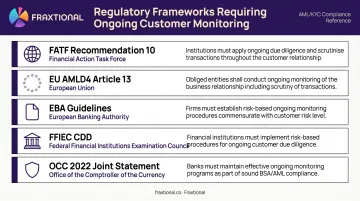

Regulators already expect ongoing monitoring. The relevant frameworks are consistent on this point:

- FATF Recommendation 10 — requires ongoing CDD and transaction scrutiny throughout the customer relationship, with records kept up-to-date especially for higher-risk customers

- EU AMLD4, Article 13 — requires ongoing monitoring including transaction scrutiny and keeping customer data current

- EBA Guidelines — firms should monitor business relationships with risk-sensitive frequency and intensity

- FFIEC CDD — banks must maintain risk-based procedures for ongoing monitoring and risk-based updating of customer information

- OCC (2022 Joint Statement) — banks should apply a risk-based approach to CDD with no assumption of uniform risk by customer type

pKYC also reduces the human error and inconsistency that come with manual periodic reviews. When every analyst works from the same continuously updated signals, the audit trail is cleaner and easier to defend.

Operational Efficiency and Cost Reduction

Automated continuous monitoring eliminates periodic review campaigns — the scheduled, resource-heavy exercises that consume significant analyst time regardless of whether customer risk has shifted. LSEG data indicates average annual spend on global KYC compliance reaches approximately $48 million per institution — a figure that reflects just how resource-intensive the current model is.

In practice, pKYC shifts how compliance teams spend their time:

- High-risk, actively changing cases get immediate analyst attention

- Low-risk customers with no meaningful changes no longer consume review capacity on a fixed schedule

- Alert queues reflect actual risk rather than calendar-driven volume

Firms like Fraxtional apply this same logic to compliance leadership: providing CCO, BSA Officer, MLRO, and CAMLO oversight without the fixed overhead of full-time executive hires — expert capacity deployed where and when it's needed.

Improved Customer Experience

For most customers, pKYC means the relationship simply continues without interruption. Updates happen in the background; outreach only occurs when a specific change warrants clarification. This removes the friction of blanket re-verification requests — and the confusion customers feel when those requests arrive with no clear reason.

What Triggers a Perpetual KYC Review?

pKYC reviews are triggered by meaningful data changes, not the calendar. Triggers typically fall across three pillars:

1. Self-Reported Data Changes

- Customer updates their registered address, legal name, or business structure

- Changes to stated business purpose or expected transaction activity

- New beneficial owners added or removed

2. External Data Signals

- Adverse media hits — negative news coverage linking the customer to financial crime, fraud, or enforcement actions

- Sanctions list additions (OFAC, EU, UN, HMT)

- Company registry filings showing changes in directors, ownership, or corporate structure

- PEP status changes — a customer or associated party becomes politically exposed

3. Transaction Behavior Anomalies

- Transaction volumes that deviate significantly from the customer's expected activity profile

- New counterparties or geographies inconsistent with the stated business

- Patterns that align with known money laundering typologies

The transaction data pillar is where AML risk becomes most concrete. A transaction monitoring alert cannot be properly investigated without access to a current, validated customer profile. pKYC creates the direct connection between KYC records and transaction monitoring that the periodic model lacks — and a stale customer profile means investigators are working blind.

That said, not all signals carry the same weight. A well-configured pKYC system applies risk-based thresholds: a sanctions hit or beneficial ownership change escalates immediately; a routine address update may simply update the record without triggering a full review. Without this calibration, analysts get buried in low-priority alerts while high-risk changes wait in the queue.

Challenges of Implementing Perpetual KYC

Data Quality and Source Reliability

pKYC is only as accurate as the data feeding it. Company registries can lag behind real-world changes by weeks or months. Unverified media sources can generate false signals. Poor source data leads directly to inaccurate risk scoring.

Firms need a documented hierarchy of trusted data sources and rigorous validation logic before they can rely on automated risk updates.

Alert Fatigue and False Positives

A continuous monitoring system that isn't properly tuned will flood analysts with low-value alerts — and when alert queues are unmanageable, genuine risks get missed. McKinsey has noted that traditional rule-based AML systems can produce false positive rates as high as 90% — a problem pKYC can either solve or worsen depending on how well it's configured.

Strong risk-based scoring, clear escalation thresholds, and human oversight are necessary to keep alerts meaningful.

Privacy, Data Retention, and Consent

Continuous monitoring must comply with applicable data protection law:

- GDPR and UK GDPR require a lawful basis for processing, purpose limitation, and data minimization

- CCPA gives California consumers rights over their personal information

- Firms must have clear legal bases for ongoing monitoring, defined data retention policies, and transparency with customers about how and why you're using their data

Monitoring everything indefinitely without a legal basis isn't pKYC — it's a privacy liability.

Legacy Technology and Integration Complexity

Many financial institutions run on systems not built for real-time data ingestion. Connecting continuous monitoring feeds, unstructured data sources like adverse media, and automated risk scoring into existing infrastructure requires careful technical planning. This challenge is particularly acute for BaaS banks and older fintechs with fragmented data environments.

That said, technology is rarely the root cause of pKYC failures. Across Fraxtional's advisory work with FinTech and BaaS clients, structural breakdowns are far more common:

- Weak or undocumented policy frameworks

- Unclear escalation ownership when alerts fire

- Absent or improperly designated BSA Officers

- Transaction monitoring systems misconfigured at deployment

Setting Up a pKYC-Ready Compliance Program

Technology doesn't make a pKYC program work on its own. The foundation has to be a well-designed compliance framework with documented policies, a risk-based approach to trigger thresholds, and clear ownership across departments.

Governance Requirements

A pKYC-ready program needs:

- Written procedures for continuous monitoring and CDD

- Documented trigger thresholds and escalation paths

- Cross-department protocols connecting compliance, IT, and operations

- Regular reviews of the pKYC policy itself — the framework needs to evolve as the business does

FinCEN has been direct: failure by leadership to devote sufficient staff and structure to BSA/AML compliance creates cascading program failures. This isn't an observation about technology — it's about governance.

The Compliance Leadership Gap

Many fintechs, crypto firms, and early-stage financial institutions want to implement pKYC but lack the in-house expertise to design, govern, and evolve the program. A fractional compliance leader — a CCO, BSA Officer, MLRO, or CAMLO — can provide the regulatory knowledge and program design expertise to build a pKYC framework without the cost of a full-time executive hire. Fraxtional places named compliance officers in exactly this role.

Fraxtional's compliance directors offer:

- ACAMS-certified professionals with direct experience across US BSA/AML, FCA/MLRO, and FATF-aligned frameworks

- Named compliance officers who can represent the firm to regulators, sponsor banks, and auditors

- Hands-on program design, not sideline advisory

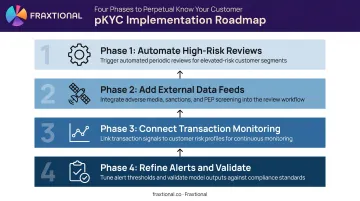

Build Toward pKYC in Phases

Firms don't need full real-time monitoring on day one. A practical phased approach:

- Automate highest-risk customer tier reviews and establish written CDD procedures

- Add external data feeds: sanctions screening, adverse media, and company registries

- Connect transaction monitoring signals to customer risk profiles

- Refine alert thresholds, reduce false positives, and validate through internal audit

Each phase builds on the last, so teams can validate what's working before adding the next layer of complexity.

Frequently Asked Questions

What is perpetual KYC?

Perpetual KYC (pKYC) is a continuous, technology-driven approach to customer due diligence that monitors and updates customer risk profiles in near real-time. Rather than relying on scheduled periodic reviews, it triggers updates when meaningful changes in customer data or behavior are detected.

Do I need to do KYC every year?

The required frequency depends on customer risk tier and applicable regulations — high-risk customers often require annual reviews under current regulatory guidance. pKYC replaces fixed cycles with event-driven updates, meaning reviews happen when something actually changes rather than on a set calendar schedule.

What does KYC mean?

KYC (Know Your Customer) is the process financial institutions use to verify customer identity, assess risk, and monitor activity to detect money laundering, fraud, and other financial crimes — covering both initial onboarding and the ongoing relationship.

What triggers a perpetual KYC review?

Reviews are triggered by meaningful changes such as adverse media hits, sanctions list updates, changes in business ownership or corporate structure, unusual transaction behavior, or updates to customer-reported information like address or legal name.

What are the biggest challenges of implementing pKYC?

The main challenges are poor data quality generating inaccurate signals, false positive alert fatigue for compliance analysts, data privacy obligations under GDPR and CCPA, and the technical complexity of integrating continuous monitoring into legacy systems.

How does pKYC improve AML compliance?

pKYC keeps customer risk profiles current between formal reviews, directly aligning with FATF and regulatory expectations for ongoing monitoring. It also connects KYC data to transaction monitoring, so analysts assess anomalies against a current profile rather than stale onboarding data.