The NMLS (Nationwide Multistate Licensing System) is the centralized platform through which mortgage loan originators, money transmitters, and other non-bank financial services providers submit license applications, track regulatory history, and maintain compliance across U.S. jurisdictions. According to the CSBS 2024 Annual Report, NMLS currently maintains records for more than 550,000 MLOs and over 34,000 companies holding state licenses — numbers that underscore how foundational this system has become.

What's less understood is who it applies to, how each step works, and what trips people up. This article breaks down the full NMLS licensing process — from pre-licensing education through ongoing maintenance — with particular attention to the nuances that catch newer market entrants off guard.

Key Takeaways

- NMLS is a filing and tracking platform; state regulators make all licensing decisions

- The SAFE Act of 2008 mandates that MLOs register through NMLS and meet minimum education, testing, and background check standards

- Getting licensed requires 20 hours of pre-licensing education, a passing score on the SAFE MLO Test (75% minimum), background checks, and state-specific filings

- NMLS extends well beyond mortgage — money transmitters, consumer lenders, and other non-bank financial services companies must register in many states

- Active licenses require 8 hours of continuing education annually, with renewal typically due by December 31

What Is the NMLS Licensing Process?

If you're building a fintech, payments, or money services business in the US, NMLS will come up — often sooner than expected.

NMLS (Nationwide Multistate Licensing System) is a web-based registry that standardizes how state regulators handle initial applications, renewals, and ongoing compliance for financial services licenses. It covers all 50 states, D.C., Puerto Rico, the U.S. Virgin Islands, and Guam.

What NMLS Actually Does

The system assigns every licensed company, branch, and individual a permanent unique identifier — their NMLS number. That number creates a single, transparent record visible to regulators and consumers alike, making it harder for misconduct to go undetected across state lines.

NMLS does not grant or deny licenses. State regulatory agencies retain all licensing authority. NMLS is the submission and tracking mechanism — nothing more.

This distinction matters practically. A complete NMLS filing is not the same as an approved license, and an NMLS ID number is not proof of active licensure. The NMLS unique identifier page states this directly: the identifier is not valid until a state license or federal registration has actually been issued.

Who NMLS Covers

Most people associate NMLS with mortgage loan originators. That's accurate but incomplete. According to CSBS, NMLS manages licensing and renewal for:

- Mortgage companies and individual MLOs

- Money services businesses and money transmitters

- Consumer finance companies

- Debt collection agencies (in participating states)

For fintech startups, payments companies, and embedded finance businesses, that scope is worth taking seriously. Many founders assume NMLS is a mortgage industry issue — until a sponsor bank or state regulator makes clear it applies to them too.

Why the NMLS Licensing Process Is Required

The requirement traces directly to 12 U.S.C. § 5101 — the SAFE Act (Secure and Fair Enforcement for Mortgage Licensing Act of 2008). Congress designed the system with four explicit goals: increase uniformity, reduce regulatory burden, enhance consumer protection, and reduce fraud.

What the SAFE Act Requires

Under 12 U.S.C. § 5103, any individual acting as a loan originator must obtain and maintain either federal registration or state licensure, plus a unique NMLS identifier. The statute covers employees of both banks and non-bank lenders.

The SAFE Act enforces three categories of standards for state-licensed MLOs:

- Competency — minimum pre-licensing education and a standardized exam

- Ethical fitness — criminal background checks and credit review

- Ongoing accountability — annual continuing education and license renewals

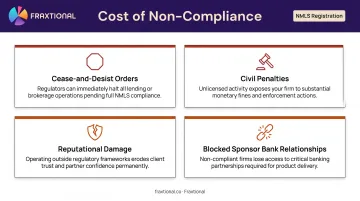

Consequences of Non-Compliance

Operating without proper NMLS registration carries real consequences. For early-stage companies in particular, the risks extend well beyond regulatory fines:

- Cease-and-desist orders that halt operations immediately

- Civil penalties imposed by state regulators

- Reputational damage that follows a company's public record

- Blocked sponsor bank relationships — banks conducting fintech due diligence check NMLS status, and an incomplete record can kill a partnership before it starts

How the NMLS Licensing Process Works

The process moves through six sequential stages. Each must be completed before proceeding to the next.

Step 1: Complete Pre-Licensing Education

Before sitting for the exam, aspiring MLOs must complete a minimum of 20 hours of NMLS-approved pre-licensing education. The federal curriculum breakdown:

| Category | Required Hours |

|---|---|

| Federal law and regulations | 3 hours |

| Ethics | 3 hours |

| Non-traditional mortgage products | 2 hours |

| Electives | 12 hours |

| Total | 20 hours |

Some states require additional hours. Washington, for example, requires 22 total hours — the standard 20 plus 4 hours of Washington-specific law (the curriculum adjusts elective hours accordingly). Tennessee and Pennsylvania require state-specific law content, though their requirements fit within the 20-hour total.

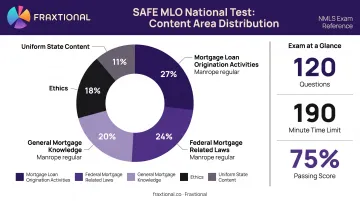

Step 2: Pass the SAFE MLO Test

The SAFE MLO National Test consists of 120 multiple-choice items (115 scored, 5 unscored), with a 190-minute time limit and a minimum passing score of 75%.

Content areas tested:

- Mortgage Loan Origination Activities — 27%

- Federal Mortgage Related Laws — 24%

- General Mortgage Knowledge — 20%

- Ethics — 18%

- Uniform State Content — 11%

Retake policy: Three consecutive attempts are permitted, each at least 30 days apart. After three consecutive failures, candidates must wait at least 6 months before testing again.

Step 3: Background Check, Fingerprinting, and Credit Review

All NMLS applicants must submit fingerprints through an NMLS-approved provider for an FBI criminal history check and authorize NMLS to pull an independent credit report. Existing fingerprints on file may be reused if less than three years old; new prints must be submitted within 180 days of authorization.

State regulators — not NMLS — evaluate both the criminal background and credit results. Adverse findings don't automatically disqualify an applicant, but they must be disclosed accurately. Note: Certain criminal history is automatically disqualifying by federal law (12 U.S.C. § 5104). Credit history is reviewed for financial responsibility on a case-by-case basis.

Step 4: Meet State-Specific Requirements

Federal minimums set the floor. Every state where an individual or company wants to operate adds its own layer. Common state-specific requirements include:

- Surety bonds (amounts vary widely by state and license type)

- Net worth minimums

- State-specific education hours

- Proof of experience

- In-state office requirements

- Additional documentation submitted directly to the state regulator

Requirements vary significantly across states:

- Maryland (money transmitter): electronic surety bond of $150,000 submitted through NMLS

- Washington (money transmitter): net worth calculated at $10,000 per $1,000,000 of prior-year transmission volume

- California DFPI (money transmitter, out-of-state control persons): FD-258 fingerprint cards on cardstock and Form JUS 203 mailed to the California DOJ, with a $49 fee per applicant

The NMLS State Resource Center's Licensing Checklists, Requirements, and Fees page is the authoritative source for state-by-state requirements.

Step 5: Submit the Application, Secure Sponsorship, and Maintain the License

Applications are filed through NMLS using the appropriate form for each license type:

- MU4 — Individual License/Registration and Consent form

- MU1 — Company form; branches use MU3

- MU2 — Control persons (branch managers, owners) complete within company filings

- State application fees are paid at submission; processing begins once the application is deemed complete

In most states, an individual MLO's license is only active while sponsored by a licensed employer through NMLS. Changing jobs requires updating sponsorship — any gap creates a lapse. Companies must also hold separate entity licenses in each state they operate.

Annual maintenance requirements:

- 8 hours of continuing education (3 hours federal law, 2 hours ethics, 2 hours non-traditional mortgage products, 1 elective hour)

- Renewal window: November 1 through December 31 in most states

- Reinstatement period: January 1 through end of February, for states that permit late reinstatement

- Employment changes, address updates, and control person changes must be reflected in NMLS records promptly

Key Factors That Affect the NMLS Licensing Process

Multi-State Complexity

Expanding across multiple states multiplies every requirement — fees, bond amounts, education mandates, and processing timelines all vary independently. A company pursuing licenses in 10 states isn't doing one process 10 times; it's managing 10 distinct regulatory relationships simultaneously.

CSBS reports that NMLS supports more than 70 different business activity definitions across the non-bank sector. That breadth of coverage means the administrative burden compounds quickly for any company with national ambitions. Early-stage companies routinely underestimate the compliance infrastructure needed to manage multi-state filings accurately.

For fintech companies and money transmitters at this stage, fractional compliance leadership is a practical alternative to full-time hires. Fraxtional's Money Transmitter Licensing service covers pre-filing strategy, state-by-state documentation, application management, and post-approval maintenance across jurisdictions.

The model gives companies access to director-level compliance experience without carrying a full-time executive on payroll.

Employment and Sponsorship Dynamics

An individual MLO's NMLS license exists only in connection with a sponsoring employer. This creates operational risk at two points:

- Job changes — sponsorship must be transferred; any gap technically lapses the license

- Company license lapses — if the employer's entity license lapses or is surrendered, the individual's active status is affected

Companies must also keep MU2 forms current for all relevant control persons. Outdated records are a common compliance gap that surfaces during regulatory examinations.

Timing and Processing Delays

State processing times vary from days to several months. California DRE, for instance, publishes live processing timeframes that can extend weeks beyond initial expectations. New York DFS gives applicants only 30 days to submit missing documents before an application is considered withdrawn.

Common delay causes include:

- Duplicate application submissions

- Unanswered questions on MU forms

- Missing course completion documentation

- FBI/DOJ fingerprint report delays

- Incomplete state-specific supporting documents

Starting well before a target launch date is the only reliable way to control timing.

Common Misconceptions About the NMLS Licensing Process

"Having an NMLS Number Means You're Licensed"

This is the most widespread misunderstanding. An NMLS unique identifier is assigned when an account is created — before any license is issued, and regardless of whether one is ever granted. The number tracks the individual or entity; it does not confirm active licensure.

The practical implication matters: to verify whether someone is actually licensed, consumers and businesses should check the NMLS Consumer Access portal, which shows current license status by state.

"NMLS Is a National License"

NMLS is a common platform, not a universal license. Registering once does not authorize operation in all states. Each state where a company or individual wants to do business requires a separate state-level application, approval, and ongoing compliance. A company operating in ten states needs ten approved licenses — with distinct requirements, timelines, and renewal obligations for each.

"NMLS Only Applies to Mortgage Professionals"

This assumption catches fintech founders and non-mortgage financial services companies off guard. Many states have expanded NMLS registration requirements well beyond mortgage. Depending on product and state footprint, obligations can apply to:

- Money transmitters and payment processors

- Consumer lenders and sales finance companies

- Collection agencies

- Embedded finance platforms

A payments startup or embedded finance company that never touches a mortgage loan can still carry significant NMLS obligations. Mapping your product to state-level licensing requirements early prevents costly surprises later.

Frequently Asked Questions

Do you need an NMLS license to be a mortgage advisor?

Yes. Any individual who originates mortgage loans as part of their job must obtain an NMLS license under the SAFE Act. This applies to mortgage advisors, loan officers, and loan originators at both bank and non-bank lenders.

What is the difference between a mortgage broker and a mortgage loan originator (MLO)?

An MLO is an individual who takes and processes mortgage loan applications. A mortgage broker is typically a company or individual that connects borrowers with lenders without funding loans directly. Both require NMLS licensing, but through different license types: individual MLO licenses for originators, and company licenses for broker entities.

How hard is the SAFE Mortgage Loan Originator (NMLS) exam?

The exam has 120 questions, requires a 75% passing score, and allows 190 minutes. Nationwide, fewer than half of first-time test-takers pass — structured pre-licensing education significantly improves those odds.

How much does a licensed MLO make in Florida?

According to BLS May 2023 data, Florida loan officers (SOC 13-2072) earned a mean annual wage of $91,520 and a median annual wage of $70,080. Compensation varies based on loan volume, experience level, and whether the MLO is salaried or commission-based.

Does an NMLS license work across all states?

No. NMLS is a common submission platform, not a universal license. Each state must independently review and approve an application before an individual or company can legally operate there.

How long does it take to get an NMLS license?

Timelines vary by state, ranging from a few weeks to several months. The main variables are how quickly an applicant completes pre-licensing education, passes the SAFE exam, clears background checks, and satisfies any state-specific documentation requirements.