Introduction

Customer risk rating sits at the core of any AML/CFT compliance program. For many fintech, crypto, and embedded finance companies, it's also one of the first things to break under pressure — and when it breaks, the result is regulatory findings, sponsor bank friction, or worse.

The tension is real: investors and product teams push for frictionless signup flows, while regulators expect documented, defensible risk assessments for every customer relationship.

Early-stage firms often end up with informal scoring, inconsistent criteria, or no documented methodology at all. Those gaps become exposed quickly — during sponsor bank reviews, investor due diligence, or regulatory examinations.

This article covers what customer risk rating is, which factors drive the score, how to structure risk tiers, and how to build a CRR framework that holds up to scrutiny. It also tackles the most common failure points — stale data, model risk, inconsistent overrides — and what to do about them.

Key Takeaways

- CRR determines whether simplified, standard, or enhanced due diligence applies to each customer

- Five core risk factors shape every rating: geography, customer type, industry, transaction behavior, and PEP/sanctions exposure

- Three standard risk tiers (low, medium, high) drive different CDD obligations and review frequencies

- Documented, consistent methodology is non-negotiable; informal approaches don't survive examiner scrutiny

- Automated scoring works at scale, but medium- and high-risk cases need human review

What Is Customer Risk Rating and Why Does It Matter?

Customer risk rating (CRR) is the documented, risk-based process of evaluating each customer's potential involvement in money laundering, terrorist financing, or fraud — and assigning a risk tier that determines how much due diligence the institution must perform.

That tier assignment is what makes CRR foundational. It drives everything downstream: which customers receive simplified CDD, which require standard CDD, and which trigger Enhanced Due Diligence with senior management approval.

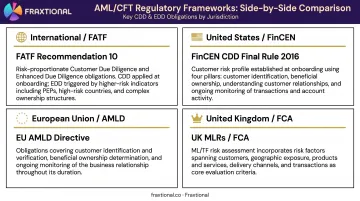

The Regulatory Mandate

CRR isn't optional. Across every major jurisdiction, regulators require a risk-based approach to customer assessment:

- FATF Recommendation 10 — requires institutions to understand the purpose and nature of customer relationships and apply CDD measures proportionate to assessed risk, with enhanced measures for higher-risk scenarios

- FinCEN CDD Final Rule (May 2016) — explicitly requires covered financial institutions to develop a customer risk profile and conduct ongoing monitoring to identify suspicious transactions

- EU AMLD (Directive 2015/849) — Article 13 mandates CDD measures including customer identification, beneficial ownership, purpose of relationship, and ongoing monitoring on a risk-sensitive basis

- UK MLRs / FCA expectations — regulated firms must identify and assess ML/TF risks considering customers, geography, products, transactions, and delivery channels

This applies to banks, fintechs, money transmitters, and crypto firms operating across these jurisdictions.

Entity-Level vs. Customer-Level Risk

Compliance teams across fintech, BaaS, and crypto frequently conflate two distinct assessments. They serve different purposes:

| Assessment | Scope | Function |

|---|---|---|

| Entity-level ML/TF risk assessment | The business as a whole | Identifies broad financial crime risks — products, markets, typologies relevant to your operating model |

| Customer-level risk rating (CRR) | Each individual or entity customer | Applies the entity framework to evaluate specific relationships against those risk dimensions |

The entity assessment sets the weightings in your CRR model. The customer rating operationalizes it for every relationship you onboard. Both are required — and regulators expect to see how one informs the other.

Key Risk Factors That Shape a Customer's Risk Profile

No single data point determines a customer's risk tier. Five dimensions interact to produce the overall score — and weakness in how you assess any one of them creates gaps across the whole framework.

Geographic Risk

Customers from — or transacting with — jurisdictions flagged by FATF, FinCEN, or national authorities require heightened scrutiny.

FATF's February 2026 high-risk jurisdiction list currently identifies DPRK, Iran, and Myanmar as subject to a call for action, requiring EDD and, in some cases, countermeasures. FATF's grey list (jurisdictions under increased monitoring) is updated each plenary cycle and should feed directly into your geographic risk matrix as a dynamic input — not a static table you update annually.

FinCEN issues corresponding notices to US financial institutions when FATF updates these lists, providing a US-specific anchor for compliance programs.

Customer Type and Ownership Structure

Individual consumers and domestic sole traders carry lower inherent risk than complex legal entities with layered ownership or opaque control structures.

Key variables include:

- Beneficial ownership transparency — US rules (31 CFR 1010.230) require capturing any individual owning 25% or more of equity interests, plus one control-prong individual. EU AMLD Article 3(6) uses the same 25% threshold

- Shell companies and nominee arrangements — treat these as elevated-risk factors where ownership cannot be independently verified

- Non-profit organizations — FATF identifies terrorist financing risk in parts of the NPO sector, but a blanket high-risk classification is inappropriate; assess activity, geography, and funding flows individually

Industry and Business Activity

Certain sectors carry elevated inherent risk due to cash flow characteristics or anonymity exposure:

- Money services businesses — FFIEC guidance identifies MSBs as higher risk because unusual activity is harder to identify in cash-intensive flows

- Virtual asset service providers — FATF continues to publish updated standards specifically addressing illicit finance risks in crypto and VASP operations

- Gambling operators and real estate — both are FATF-designated non-financial businesses with specific CDD obligations and typology risk

Your CRR model should assign baseline sector risk scores, then adjust based on the customer's specific activity profile and jurisdiction.

Transaction Patterns and Product Usage

Anticipated versus actual transaction behavior is a primary driver of risk re-assessment. At onboarding, document the customer's expected activity across each of these dimensions:

- Transaction volumes and frequency

- Payment types (wire, ACH, card, crypto)

- Counterparty profiles and relationships

- Geographic flows of funds

Flag material deviations from this baseline for review. A customer who onboards as a domestic freelancer but starts receiving large international wire transfers within 60 days warrants scrutiny regardless of their original risk tier.

PEP Status, Sanctions Exposure, and Adverse Media

PEP status, sanctions exposure, and adverse media each feed into CRR differently — and conflating them leads to compliance gaps:

- Sanctions matches (OFAC SDN List, UN Consolidated List, EU Financial Sanctions List, UK Sanctions List) are absolute blockers — OFAC is explicit that US persons are prohibited from transacting with SDNs. Feed sanctions screening results into CRR, but treat confirmed matches as legal prohibitions, not just elevated risk scores

- PEPs — FATF Recommendation 12 governs PEP risk management; foreign PEPs and their close associates automatically require EDD regardless of other risk factors

- Adverse media — financial crime convictions, regulatory sanctions, fraud allegations, and law enforcement actions must be factored into the overall risk profile and documented in the customer file

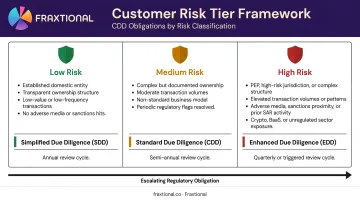

Risk Rating Levels: Low, Medium, and High Risk Explained

| Risk Tier | Typical Characteristics | CDD Standard | Review Cadence |

|---|---|---|---|

| Low | Domestic resident, transparent occupation, low-risk product, no adverse indicators | Simplified CDD | Annually or biennially |

| Medium | Medium-risk jurisdiction, moderately complex structure, domestic PEP, medium-risk product | Standard CDD | Every 6–12 months |

| High | Foreign PEP, FATF high-risk jurisdiction link, opaque ownership, cash-intensive/crypto business, adverse media | Enhanced Due Diligence (EDD) | Quarterly or more frequently |

Each tier carries distinct regulatory obligations that go beyond what the table captures. Simplified CDD under FATF Recommendation 10 is available for low-risk customers, but only where the risk assessment affirmatively supports that classification — not as a default for fast onboarding.

Standard CDD applies at the medium tier: identity verification, beneficial ownership where applicable, purpose and nature of the relationship, and ongoing monitoring calibrated to the customer's profile.

At the high tier, EDD is mandatory: source of wealth and source of funds verification, senior management approval before onboarding or before continuing the relationship, and the most intensive monitoring cadence. FATF Recommendations 12 and 19 make these obligations non-negotiable for PEPs and high-risk country connections respectively.

Best Practices for Building an Effective CRR Program

Establish a Documented, Risk-Based Framework

Every element of your CRR methodology must be formally documented — which risk factors are assessed, how they are weighted, what thresholds define each tier, and who can approve exceptions. Undocumented or informal approaches will not survive an examination.

The FFIEC BSA/AML Examination Manual is direct on this point: examiners assess whether institutions have documented policies, procedures, and processes for CDD, including understanding customer relationships and maintaining risk profiles. If your CRR lives in a spreadsheet with no written methodology behind it, that's a gap.

Draw your risk factor weightings from the entity-level ML/TF risk assessment — not from industry templates. The factors that matter most for your program depend on your product set, customer base, and operating model.

Implement a Consistent Risk Scoring Methodology

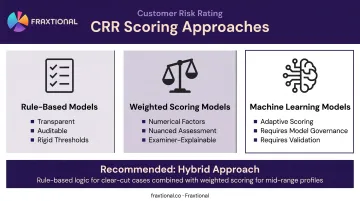

Three main approaches exist, each with trade-offs:

- Rule-based models — predefined thresholds (e.g., any customer from a FATF grey-list country = medium risk). Transparent and auditable, but rigid

- Weighted scoring models — numerical scores assigned to each risk factor, summed to a total. More nuanced, still explainable to examiners

- Machine learning models — FCA research confirms ML is used in AML and fraud detection in UK financial services, and OCC's revised model risk guidance (Bulletin 2026-13) addresses governance requirements for these systems

For most fintechs and crypto firms, a hybrid approach works best: rule-based logic for clear-cut cases (FATF black-list jurisdictions, confirmed PEPs), with weighted scoring for everything in between.

Model transparency matters. Compliance teams, investigators, and regulators must be able to explain why a customer received a given rating. OCC's model risk framework requires documentation of assumptions, validation methodology, and override governance — and black-box outputs that can't be explained create direct examination exposure.

Build in Ongoing Monitoring and Triggered Re-Assessments

CRR is not a one-time onboarding decision. Customer risk profiles must be reviewed at scheduled intervals and re-assessed immediately when material triggers occur.

Define in policy:

- Who is authorized to change a customer's risk rating

- What documentation is required for each rating change

- How rating changes feed back into transaction monitoring thresholds

- Which events constitute mandatory re-assessment triggers

The FFIEC BSA/AML Manual's CDD examination procedures address exactly this process — examiners will look for evidence that your review cycle and trigger framework are documented, followed, and auditable.

Maintain Comprehensive Records and Audit Trails

Retention requirements are consistent across key jurisdictions: US regulations (31 CFR 1010.430), UK MLRs 2017, FINTRAC in Canada, and EU AMLD Article 40 all require 5 years. What you retain matters as much as how long.

Each customer record should capture:

- Customer information collected and verified

- Risk factors assessed and their weighted values

- Rationale for the assigned rating

- EDD results where applicable

- CRR version, analyst overrides, and approval evidence

- Records of periodic reviews and refresh history

Invest in Staff Training and Cross-Functional Alignment

A CRR framework is only as effective as the people applying it. Compliance, onboarding, and operations staff all need to understand the risk criteria, red flags, escalation procedures, and how to apply the rating system consistently.

For early-stage fintechs and crypto firms that can't justify a full-time Chief Compliance Officer or BSA Officer, fractional compliance leadership (a fractional BSA Officer, CAMLO, or MLRO) gets the CRR program designed and maintained to a regulatory standard. Fraxtional's fractional BSA Officers, for example, take direct ownership of BSA risk assessments, KYC/KYB effectiveness reviews, and sanctions oversight, bringing the institutional knowledge that early-stage teams typically lack without the cost of a full-time executive hire.

Common Challenges in Customer Risk Rating — and How to Overcome Them

Data Quality and Completeness

Incomplete, inaccurate, or stale customer data is the single largest driver of CRR model failures. Customers who provide minimal information at onboarding, or whose data isn't refreshed over time, create blind spots that undermine the entire scoring model.

Practical fixes:

- Build structured onboarding forms that collect all required CRR inputs at the point of customer acquisition

- Define periodic CDD refresh cycles by risk tier, and document them in policy

- Establish data governance controls that flag missing or expiring information for follow-up

Keeping Pace with Regulatory Change

AML/CFT regulations across the US, UK, EU, and Canada evolve continuously — new FATF guidance, updated AMLD directives, FinCEN rulemakings. CRR models must be reviewed and updated to reflect both regulatory changes and emerging financial crime typologies.

For resource-constrained fintechs, this is where compliance capacity gets tested most. Two review triggers to build into policy:

- Annual reviews: Scheduled model assessments tied to your compliance calendar

- Ad hoc reviews: Triggered by major regulatory publications (new FATF guidance, FinCEN rulemakings, updated AMLD directives)

Balancing Scalability with Accuracy

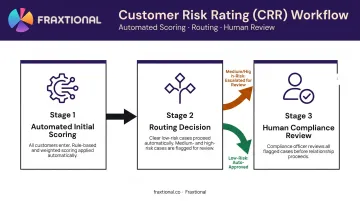

Manual CRR processes don't scale. But fully automated systems without human oversight miss nuanced risk signals — the FCA flagged this directly in its April 2026 findings, noting that stronger firms used independent third-line testing across onboarding and due diligence.

A tiered workflow solves this: automate the initial risk score for clear low-risk cases, and route medium- and high-risk assessments to a compliance officer before the relationship proceeds. That same tiered structure also determines how false positive risk gets managed.

Managing False Positives and Model Risk

Overly conservative models flood analysts with high-risk classifications, strain operations, and harm legitimate customers. Overly lenient models create compliance gaps. Neither is acceptable.

Calibrate risk thresholds at least annually against historical data. Back-test model outputs against SAR/STR filing history to check whether flagged customers actually produced suspicious activity, then adjust accordingly. OCC's model risk guidance provides the governance framework for this process if your CRR uses statistical or ML components.

Frequently Asked Questions

What is the customer risk rating?

Customer risk rating is the process financial institutions use to evaluate and categorize the money laundering, fraud, and financial crime risk associated with each customer — based on their identity, location, business activity, and transaction behavior — to determine how much due diligence that relationship requires.

What are the levels of customer risk rating?

The standard framework uses three tiers: low risk (simplified CDD, annual or biennial review), medium risk (standard CDD, review every 6–12 months), and high risk (mandatory Enhanced Due Diligence, senior management approval, and the most intensive ongoing monitoring).

What are the 4 pillars of KYC?

The four pillars are: Customer Identification Program (CIP), Customer Due Diligence (CDD), Enhanced Due Diligence (EDD), and Ongoing Monitoring. CRR sits within the CDD pillar, determining how much due diligence each customer relationship requires.

How often should customer risk ratings be reviewed or updated?

Review frequency is risk-driven: low-risk customers typically annually or biennially; medium-risk every 6–12 months; high-risk quarterly or more frequently.

What triggers a change in a customer's risk rating?

Common triggers include: significant unexplained changes in transaction activity, changes in ownership or business structure, new adverse media findings or sanctions matches, law enforcement inquiries, or the customer beginning to use a higher-risk product or entering a new jurisdiction.