Introduction

The ACH Network processed 35.2 billion payments valued at $93 trillion in 2025, with Same Day ACH growing 16.7% year-over-year. Person-to-person payments alone surged 19.8% to nearly 470 million transactions. This explosive growth in electronic fund transfers has made Regulation E compliance a baseline requirement—and a harder one to execute at scale.

Reg E compliance challenges banks, credit unions, fintechs, neobanks, and money transmitters alike. The consequences extend well beyond regulatory fines, touching customer trust, sponsor bank relationships, and operational efficiency.

Regulatory scrutiny has intensified, particularly around P2P platforms like Zelle and Venmo. Institutions that struggle with dispute handling, provisional credit timelines, or consumer correspondence accuracy face examination findings, enforcement actions, and lasting reputational damage.

This article covers what Regulation E requires, where institutions consistently fall short, and what practical solutions look like for banks and fintechs operating in today's payments environment.

Key Takeaways

- Regulation E (implementing EFTA) protects consumers through required disclosures, error resolution timelines, and liability limits on unauthorized transfers

- Applies broadly to banks, fintechs, neobanks, prepaid card providers, and P2P payment platforms

- Error resolution timelines and provisional credit obligations are the most compliance-intensive requirements

- Common mistakes include delaying investigations pending documentation, misapplying the 60-day rule, and sending inaccurate consumer correspondence

- Best practices include centralized dispute intake, documented workflows, staff training, and ongoing monitoring

What Is Regulation E and Who Does It Apply To

Regulation E implements the Electronic Fund Transfer Act (EFTA) of 1978, codified at 12 CFR Part 1005 and enforced by the Consumer Financial Protection Bureau (CFPB). Its primary purpose is protecting individual consumers engaging in electronic fund transfers by establishing clear rights, liabilities, and responsibilities across all parties involved in these transactions.

Coverage Scope

Regulation E applies strictly to consumer accounts (not business accounts) and covers:

- Debit card purchases and ATM withdrawals

- ACH transfers and direct deposits

- Online bill payments and telephone-initiated transfers

- P2P payments that meet the EFT definition

- Payroll card accounts and prepaid card transactions

Key exclusions:

- Credit card transactions (covered under the Fair Credit Billing Act)

- Business accounts and commercial transfers

- Wire transfers primarily used between financial institutions

- Checks, drafts, and paper instruments

Who Has Compliance Obligations

Understanding what's covered is only half the picture. The more pressing question for most organizations is whether they're considered a "financial institution" under the rule — and therefore obligated to comply.

Under 12 CFR 1005.2(i), a "financial institution" includes any entity that directly or indirectly holds a consumer account or issues an access device and agrees to provide EFT services. This definition includes:

Traditional institutions:

- Banks and savings associations

- Credit unions and thrifts

Modern fintech entities:

- Fintech companies offering consumer accounts

- Prepaid card issuers (subject to the 2019 Prepaid Accounts Rule)

- Neobanks and embedded finance platforms

- Money transmitters facilitating consumer EFTs

- Nonbank P2P payment providers that hold consumer accounts or issue access devices

Critical point for fintechs: Companies operating under sponsor bank models must understand which entity bears Reg E obligations contractually and operationally. Regardless of how those obligations are allocated in a contract, regulators may still hold the sponsor bank responsible for program failures. Fintechs must therefore build processes that fully satisfy sponsor bank compliance standards — not just their own internal thresholds.

Core Regulation E Compliance Requirements

Consumer Disclosures

Before a consumer's first EFT, financial institutions must provide written disclosures covering:

- Available EFT types and any transfer limitations

- Applicable fees for transfers or account maintenance

- Consumer liability limits for unauthorized transactions

- Error resolution procedures and how to report issues

- Institution's contact information and business days

Change-in-terms notice: Institutions must provide at least 21 days' notice before adverse changes take effect (such as increased fees or stricter transfer limits). The only exception is when immediate changes are necessary for security purposes.

Error Resolution Procedures

The error resolution process operates on two core timelines under §1005.11(c):

Standard 10-business-day investigation:

- Investigate and determine if an error occurred

- Report results to consumer within 3 business days of completion

- Correct any confirmed error within 1 business day

Extended 45-calendar-day investigation:

- Available only if institution provides provisional credit within 10 business days

- Must notify consumer within 2 business days of granting provisional credit

- Consumer receives full use of funds during investigation

Extended timelines for special circumstances:

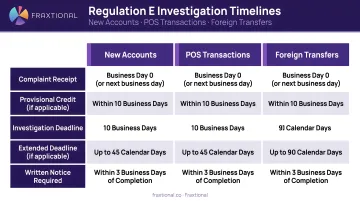

| Account/Transaction Type | Investigation Window | Provisional Credit Window |

|---|---|---|

| New accounts (first 30 days) | 20 business days | 90 calendar days |

| Point-of-sale debit transactions | 45 calendar days | 90 calendar days |

| Foreign-initiated transfers | 45 calendar days | 90 calendar days |

Provisional credit obligations: If investigation cannot be completed within 10 business days, the institution must:

- Credit the alleged error amount plus applicable interest within that window

- Notify consumer of provisional credit within 2 business days

- Provide full use of funds during the extended investigation period

- If provisional credit is reversed after investigation, notify the consumer and honor checks/preauthorized transfers for 5 business days without overdraft fees

Consumer Liability Limits

Regulation E establishes a tiered liability framework based on when consumers report unauthorized transfers:

- $50 maximum if reported within 2 business days of discovering loss or theft

- Up to $500 if reported between 2 and 60 days after discovering loss

- Unlimited liability for transfers occurring more than 60 days after the statement showing the unauthorized transfer was sent

Critical clarification: Even when consumers report outside these windows, institutions must still investigate and cannot simply deny claims based on untimely notice alone. Consumer negligence (such as writing a PIN on a card) cannot be used to impose greater liability than Regulation E permits.

Periodic Statements and Receipts

Two required documentation outputs apply here:

- Terminal receipts — Required for transactions over $15 at electronic terminals; must show amount, date, type, terminal location, and merchant identification

- Periodic statements — Required at least monthly when EFTs occur (quarterly if no activity); must include enough detail—amount, date, type, terminal location, and third-party identification—for consumers to identify each transaction

Record Retention

Under §1005.13, institutions must retain compliance records for at least two years from the date disclosures are made or action is required. This includes:

- Initial and change-in-terms disclosures

- Error notices and investigation documentation

- Provisional credit notifications

- All consumer correspondence

During examinations, regulators typically request error resolution files and provisional credit notifications first — gaps in these records are among the most common findings in Reg E enforcement actions.

Regulation E Error Resolution: Timelines, Provisional Credit, and the Investigation Process

What Qualifies as a Reg E Error

Under §1005.11(a)(1), an "error" includes:

- Unauthorized EFTs initiated without consumer permission

- Incorrect EFTs to or from the consumer's account

- EFTs omitted from a periodic statement

- Computational or bookkeeping errors by the institution

- Receipt of incorrect cash amount from an electronic terminal

- EFTs not properly identified on receipts or statements

- Consumer requests for documentation or clarification

What does NOT trigger error resolution:

- Routine balance inquiries

- Requests for tax or recordkeeping information

- Requests for duplicate documentation

What Triggers the Investigation

Once the consumer's notice enables the institution to identify their name, account number, and reason for the dispute, the investigation clock starts. Two requirements catch institutions off guard:

Critical requirements:

- Oral notice alone is sufficient — the investigation clock starts immediately

- Institutions may request written confirmation within 10 business days but cannot hold the investigation pending that confirmation

- Institutions cannot require consumers to file police reports, sign fraud affidavits, or contact merchants before opening a claim

- The investigation must begin "promptly upon receipt of an oral notice"

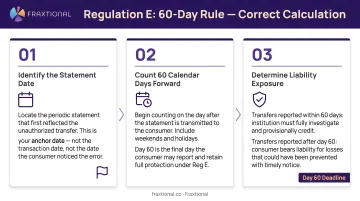

The 60-Day Rule (Frequently Misapplied)

The 60-day window runs from the date the periodic statement was sent, not from the date the consumer discovered the error or reported it. This distinction is frequently misapplied, leading to incorrect liability calculations and wrongful denials.

How institutions should apply the rule:

- Identify the statement on which the alleged error first appeared

- Count 60 days forward from the date that statement was transmitted

- Determine whether the consumer's notice fell within that window

Important limitation: Even if notice is received after 60 days, the institution must still comply with §1005.6 liability rules before imposing liability on the consumer for an unauthorized EFT.

Conducting the Investigation

A reasonable investigation goes beyond pulling transaction records. It typically includes:

- Reviewing account histories and transaction records

- Examining any available third-party documentation

- Contacting merchants or third parties when necessary

- Obtaining terms and conditions for subscription or trial charges

- Determining whether a transaction may be a merchant dispute rather than a Reg E error

Common pitfall: Prior authorized transactions with the same merchant do not by themselves justify denying a new unauthorized transaction claim. Each claim must be investigated on its own merits.

Consumer Correspondence Requirements

Institutions must provide written notification at three key points:

- When provisional credit is granted (within 2 business days of granting it)

- When the investigation concludes, regardless of outcome

- When provisional credit is reversed after the investigation finds no error

Denial and reversal notices carry additional requirements. The written explanation must cover investigation findings, disclose the consumer's right to request documentation relied upon, and confirm the institution will honor certain items for 5 business days after notification.

Enforcement trigger: Mislabeling provisional credit as "final" strips the institution of its ability to reclaim that credit. Omitting the consumer's right to review documentation is a direct Reg E violation.

Common Regulation E Compliance Mistakes That Trigger Enforcement

Requiring Documentation Before Starting Investigations

CFPB Supervisory Highlights consistently cite institutions for requiring consumers to provide written affidavits, police reports, or complete formal fraud declarations before starting investigations.

The investigation clock starts the moment the institution receives minimal oral or written notice: the consumer's name, account number, and a brief explanation of why they believe an error occurred. Additional documentation can be requested, but it cannot delay the investigation start.

Siloed Investigation Management

When Reg E errors are routed to different departments based on error type—ACH team, fraud team, deposit operations, electronic banking—there is high risk of:

- Investigation delays and missed deadlines

- Inconsistent consumer outcomes

- Documentation gaps and failed handoffs

- Timeline tracking failures

The fix is a centralized dispute intake function that assigns investigations to the appropriate team while maintaining unified timeline tracking and consumer communication.

Deadline management is where siloed structures most commonly break down — and miscalculating the timeframes themselves compounds the problem.

Misapplying the 60-Day Rule

Institutions frequently count 60 days backward from the consumer's notification date rather than forward from the statement transmittal date. This error leads to:

- Over-denying valid claims that were actually timely reported

- Miscalculating consumer liability exposure

- CFPB examination findings

To illustrate correct application:

- Statement showing unauthorized EFT mailed: January 15

- 60-day window: January 15 to March 15

- Consumer reports on March 10: Timely

- Consumer reports on March 20: After 60 days, but still requires investigation under §1005.6

Consumer Correspondence Accuracy Problems

Errors in written correspondence create independent Reg E violations — separate from any underlying investigation failures.

Labeling provisional credit as "final" in correspondence strips the institution of its right to reclaim that credit if the investigation later finds no error — a common and costly mistake.

Denial letters create a second exposure point when they fail to:

- Provide detailed explanation of findings

- Offer the consumer the option to review relied-upon evidence

- Notify the consumer of the 5-business-day grace period for honored items

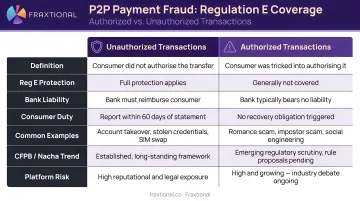

P2P and Scam-Related Disputes

With the growth of Zelle, Venmo, Cash App, and similar platforms, institutions must navigate the distinction between:

Unauthorized EFTs (covered):

- Transfers initiated by fraudsters using stolen credentials

- Fraudulently obtained account access information via phishing or spoofing

- Transfers the consumer did not authorize or initiate

Authorized-but-fraudulently-induced transactions (historically excluded but now under active CFPB scrutiny):

- Consumer authorized the transfer but was deceived about the recipient or purpose

- Consumer willingly provided account credentials to someone they believed was legitimate

The CFPB has clarified that credential-based fraud is "unauthorized" under Regulation E, triggering full liability protections. Private network rules stating transfers are final and irrevocable do not reduce consumer protections against liability for unauthorized EFTs.

Regulation E Compliance Solutions and Best Practices for Fintechs

Building a Scalable Reg E Program

The foundation of effective Regulation E compliance requires five core elements:

1. Clear written policy

- Defines what constitutes a Reg E error versus an inquiry or merchant dispute

- Establishes investigation procedures and timeline requirements

- Outlines provisional credit criteria and reversal procedures

- Specifies roles and responsibilities across teams

2. Centralized error intake and case management

- Single point of entry for all consumer error notices

- Unified timeline tracking system

- Consistent consumer communication templates

- Clear escalation paths for complex cases

3. Standardized investigation procedures

- Documentation checklists for each error type

- Required review of account history and transaction records

- Merchant/third-party contact protocols

- Decision-making criteria and approval workflows

4. Trained frontline and operations staff

- Understanding of what triggers a Reg E investigation

- Knowledge of timeline requirements and provisional credit rules

- Consumer communication requirements and correspondence accuracy

- Recognition of common compliance pitfalls

5. Monitoring and audit function

- Periodic testing of whether errors are handled within required windows

- Review of consumer correspondence for accuracy and completeness

- Assessment of provisional credit provisioning and reversals

- Tracking of examination findings and corrective actions

Third-Party and Sponsor Bank Oversight

Fintechs operating under sponsor bank models must understand which entity bears Reg E obligations contractually and operationally. Regardless of contractual allocation, regulators may hold the sponsor bank responsible for program failures.

Third-party service provider (TPSP) oversight essentials:

If a payment processor, core banking system, or dispute management platform handles dispute intake or investigation workflow, the fintech or sponsor bank must ensure:

- Contracts clearly assign responsibility for dispute resolution and customer complaints

- Agreements explicitly require regulatory examination access

- Ongoing monitoring of the third party's compliance with consumer laws

- Customer complaint response rates are tracked and measured

- Subcontractor reliance is identified and assessed

The 2023 Interagency Guidance on Third-Party Relationships makes clear that using a vendor does not transfer compliance responsibility. Institutions must maintain active oversight, conduct periodic reviews, and demonstrate vendor management controls during examinations.

Compliance Leadership for Growing Fintechs

Early-stage and growing fintech companies often struggle to staff full compliance functions capable of building and maintaining Regulation E programs. The operational complexity involves centralized intake, timeline tracking, provisional credit management, and consumer correspondence — all requiring dedicated expertise that many startups cannot afford to hire full-time.

Fractional compliance leadership provides director-level expertise in Reg E, BSA/AML, UDAAP, and related obligations without the cost and commitment of a full-time Chief Compliance Officer (CCO) or Chief Risk Officer (CRO) hire. This model is especially valuable when:

- Preparing for sponsor bank due diligence where Reg E compliance infrastructure is scrutinized

- Addressing regulatory examination findings or consent order requirements

- Building compliance programs ahead of investor reviews or Series A/B fundraising

- Transitioning from startup to regulated entity with consumer account obligations

Firms like Fraxtional offer embedded compliance leadership that functions as part of the internal team: drafting policies, training staff, implementing case management systems, and representing the company to banks, regulators, and investors. Most clients use the fractional model to get an experienced compliance program running in weeks — not the months a full-time search typically requires.

Frequently Asked Questions

What does Regulation E require financial institutions to do?

Regulation E requires financial institutions to provide consumer disclosures before the first EFT, follow strict error investigation timelines (10 or 45 business days depending on whether provisional credit is issued), limit consumer liability for unauthorized transfers to $50-$500 based on reporting timing, and maintain compliance records for at least two years.

What types of electronic fund transfers does Regulation E cover?

Regulation E covers debit card purchases, ACH transfers, ATM withdrawals, direct deposits and withdrawals, online bill payments, telephone-initiated transfers, P2P payments meeting the EFT definition, and payroll card transactions — though credit card transactions and business accounts fall outside its scope.

Which financial institutions does Regulation E apply to?

Regulation E applies to banks, credit unions, and any entity that holds a consumer account or facilitates EFTs. This includes fintech companies, prepaid card issuers, neobanks, money transmitters, and nonbank P2P payment providers offering consumer-facing products.

Does Regulation E apply to Zelle and other person-to-person payment apps?

Yes. P2P transfers through Zelle, Venmo, Cash App, and similar apps that meet the EFT definition are covered. The CFPB has confirmed that unauthorized transfers (including those made with stolen credentials) are protected — though authorized-but-fraudulently-induced transactions remain a contested area.

What are common compliance mistakes with Regulation E?

Common errors include:

- Requiring police reports or affidavits before opening an investigation

- Misapplying the 60-day statement rule by counting from the notification date instead of the statement date

- Routing disputes across departments, causing timeline failures

- Sending correspondence that mislabels provisional credits or omits consumers' review rights

What are the best compliance solutions for Regulation E?

Strong Reg E programs typically include:

- Centralized dispute intake with unified timeline tracking

- Written error resolution procedures and documentation checklists

- Regular staff training on investigation requirements and consumer correspondence

- Periodic audits to test timeline adherence and third-party processor oversight

- Fractional compliance leadership for companies without dedicated compliance teams