Industry data from Datos Insights shows AML models routinely generate 90%–95% false-positive rates. That's not a technology problem — it's a calibration problem. Most institutions have monitoring systems in place. The real differentiator is how well those systems are tuned.

This article explains exactly how to tune a transaction monitoring system for AML compliance: what you need before you start, the five-step process, the key parameters that drive outcomes, and the mistakes that convert a functional program into a regulatory liability.

Key Takeaways

- Tuning adjusts alert thresholds, rules, and parameters so your system catches genuine suspicious activity without overwhelming investigators.

- A well-tuned program requires a performance baseline, customer segmentation, data-driven threshold calibration, and structured testing.

- Key parameters: alert threshold levels, lookback windows, segmentation criteria, and scenario/typology coverage.

- Schedule formal reviews at least annually if your TM system qualifies as a model under SR 11-7; material changes require off-cycle reviews.

- Documentation is not optional — regulators expect working papers justifying every parameter decision.

How to Tune Transaction Monitoring for AML Compliance

Step 1: Establish a Performance Baseline

Before changing anything, measure what you have. Pull your current alert volumes, true positive rates (alerts that led to SARs or active investigations), and false positive rates across every active monitoring scenario.

This data tells you two things immediately:

- Which scenarios are over-alerting — generating high volumes with few or no SARs

- Which scenarios may be under-detecting — producing low alert counts that warrant scrutiny of whether thresholds are set too high

Flag any scenario that has produced zero SARs over the past 12 months. That's not necessarily evidence of a clean book of business — it may mean the threshold is miscalibrated and genuine activity is passing undetected. These are your highest-priority targets for tuning.

Step 2: Segment Your Customer and Transaction Population

A single threshold applied across all customers will always be wrong for most of them. Segmentation is how you fix that. Divide your customer base into meaningful, risk-based groups using criteria such as:

- Customer type — individual retail, small business, corporate

- Risk rating — low, medium, high (tied to your CDD/KYC records)

- Transaction product — wire transfers, cash deposits, ACH, crypto

- Geography — domestic vs. cross-border, high-risk jurisdictions

Higher-risk segments — money service businesses, crypto-related accounts, high-volume international transfer customers — should carry lower thresholds that trigger alerts at lower activity levels. Lower-risk segments receive higher thresholds that filter out ordinary behavior.

Segmentation criteria must reflect your institution's actual risk profile per your most recent enterprise-wide risk assessment. Creating too few segments, or the wrong segments, can lump high-risk activity into low-risk categories — which is precisely the structural flaw that drew FCA criticism in multiple enforcement actions.

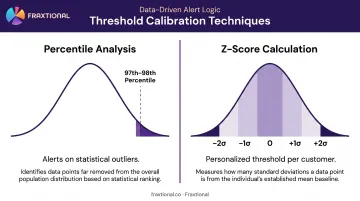

Step 3: Recalibrate Thresholds Using Data Analysis

Use historical transaction data to identify the distribution of activity within each segment. Two statistical approaches provide a defensible, data-driven basis for threshold values:

- Percentile analysis — setting thresholds at the 97th or 98th percentile of normal activity for a given segment, so the system alerts on outliers rather than ordinary transactions

- Z-score calculations — measuring how many standard deviations a transaction is from that customer's own historical mean, creating a personalized alert threshold rather than a universal dollar figure

Z-scores are worth understanding clearly. If a customer's average monthly wire transfer is $8,000 with a standard deviation of $2,000, a $20,000 transfer sits six standard deviations above their mean: a meaningful signal. A flat $15,000 threshold applied to all customers would miss that transfer entirely, while generating noise for customers whose normal activity exceeds that amount.

Neither percentile analysis nor z-scores are explicitly mandated by FFIEC or FinCEN. They're defensible internal techniques because they're grounded in your actual data, documented with clear rationale, and validated before implementation. That documentation becomes your evidentiary foundation in any examiner review.

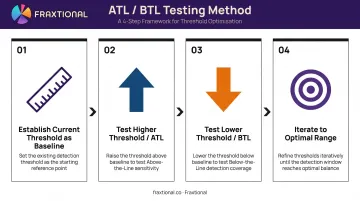

Step 4: Run Above-the-Line / Below-the-Line (ATL/BTL) Testing

ATL/BTL testing is the practical method for finding the optimal threshold range before committing to changes.

Here's how it works:

- Start with your current threshold as the baseline

- Test a higher threshold (above the line) — identify which alerts would be dropped and review whether any represent genuine suspicious activity

- Test a lower threshold (below the line) — identify what new alerts would appear and determine whether additional volume is productive or noise

- Iterate until you identify a range where alert quality is optimized

The review of dropped alerts is the critical step. If alerts lost to a higher threshold include activity that would have led to a SAR, raising the threshold isn't a calibration improvement: it's a coverage gap.

No regulatory guidance prescribes an acceptable false positive rate. Institutions must use their own testing results, risk appetite, and investigative capacity to determine what's appropriate. That rationale must be documented thoroughly.

The FinCEN assessment of U.S. Bank is instructive here: U.S. Bank conducted below-threshold testing that revealed alert caps were causing missed suspicious activity, then terminated that testing rather than removing the caps. The result was a $185 million penalty and 1,528 late-filed SARs covering over $318 million in suspicious activity.

With threshold ranges confirmed, the work shifts to locking in those decisions through documentation and independent validation.

Step 5: Document, Validate, and Implement

All tuning decisions must be captured in working papers presentable to auditors and examiners. Documentation should include:

- Analysis performed and data sources used

- Each threshold tested, with rationale for rejecting alternatives

- Final parameter decisions and the reasoning behind each

- Segments or scenarios adjusted, with explanations

- Independent validation outcomes and findings

Under SR 11-7 model risk management guidance, if your TM system qualifies as a model, validation must be independent from the team that developed or tuned the parameters. That means a second-line compliance function or an external party.

The 2021 interagency statement from the Federal Reserve, FDIC, and OCC confirmed that complex AML transaction monitoring systems may qualify as models, with full validation requirements applied as a result.

Insufficient documentation is itself a matter requiring attention (MRA) risk. The FCA's Financial Crime Guide makes this explicit: firms that cannot articulate the rationale for threshold choices have a control failure, not just an administrative gap.

When Should You Tune Your Transaction Monitoring System?

Tuning is an ongoing obligation, not a one-time project. The appropriate cadence depends on your jurisdiction and whether your system qualifies as a model:

| Framework | Frequency Requirement |

|---|---|

| SR 11-7 (US) | At least annual review for systems qualifying as models |

| FFIEC BSA/AML Manual | Periodic evaluation of filtering criteria and thresholds |

| FINTRAC (Canada) | AML program effectiveness review at minimum every 2 years |

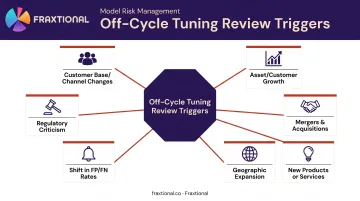

Beyond scheduled reviews, certain events require an off-cycle tuning review:

- Significant asset or customer growth

- Mergers or acquisitions

- Launch of new products or services

- Geographic expansion or entry into higher-risk markets

- Material change in false positive or false negative rates

- Regulatory criticism of existing parameters

- Shifts in the customer base or transaction channels

Criminal tactics also shift over time. Typologies and transaction channels evolve — and thresholds calibrated to last year's patterns may already be blind to current risks. The FCA's enforcement action against HSBC explicitly cited failure to recalibrate alert systems and thresholds as a contributing factor to a £64 million fine. That outcome is reason enough to treat periodic reviews as a genuine risk management obligation — not a compliance checkbox.

What You Need Before Tuning Your TM System

Effective tuning depends entirely on the quality of inputs. Attempting to calibrate thresholds without clean data, a current risk assessment, or the right expertise produces results that are harder to defend and more likely to miss the mark.

Data and Documentation Requirements

Before beginning any tuning exercise, you need at minimum:

- 12 months of historical alert data — dispositions included (escalated, closed as false positive, or led to a SAR)

- A current enterprise-wide risk assessment — segmentation must reflect your documented risk profile, not assumptions

- Up-to-date customer segmentation data — tied to your CDD/KYC records and reflecting actual customer risk ratings

Without alert disposition data, you cannot calculate true positive rates. Without a current risk assessment, segmentation decisions lack a defensible basis. Both gaps will show up immediately under examiner scrutiny.

Skill and Oversight Requirements

Tuning a transaction monitoring system requires someone who understands both the statistical methods being applied and the regulatory expectations they must satisfy. That combination is less common than most institutions expect.

Many fintechs, crypto firms, and growing financial institutions engage a fractional BSA Officer or MLRO — such as those available through Fraxtional — to lead or oversee this process. Director-level judgment goes well beyond running percentile calculations. It means interpreting results against your risk profile, making defensible threshold decisions, coordinating independent validation, and producing working papers that hold up under examination. Without that oversight, the documentation gaps become the first thing examiners find.

Key Parameters That Affect Transaction Monitoring Tuning Results

Transaction monitoring tuning isn't a single-lever problem. Each parameter interacts with the others — adjusting one without accounting for the rest can fix one gap while opening another.

Alert Threshold Levels (Amount and Frequency)

The dollar amount or transaction count at which an alert fires is the most direct lever in tuning. Set too high and suspicious activity falls below the line. Set too low and volume buries genuine risk in noise.

The enforcement record is clear on what threshold miscalibration costs. The FCA fined Santander UK £107.8 million in 2022 partly because its automated transaction monitoring didn't use anticipated customer turnover, and Business Banking alerts were treated as medium risk regardless of the customer's actual risk rating. The underlying system wasn't broken. The thresholds were — and the regulatory consequences reflected that directly.

Lookback Window (Time Period for Aggregation)

The time period over which transactions are aggregated determines whether the system can detect structuring and layering patterns. A 5-day lookback window misses deposits broken up over 10 days, even if the individual transactions would have flagged at a longer horizon.

Lookback windows must be long enough to detect aggregated structuring behavior, but calibrated to your transaction volumes and investigator capacity. Longer windows surface more patterns, though they also create larger datasets per alert for investigators to review.

Key tradeoffs to balance when setting lookback windows:

- Detection coverage — shorter windows miss multi-day structuring patterns

- Alert volume — longer windows increase the dataset size investigators must review per alert

- Transaction velocity — high-volume platforms need tighter windows to avoid alert backlogs

Customer Segmentation Criteria

A cash deposit threshold appropriate for a retail customer will generate constant false positives for a cash-heavy small business, or fail to flag suspicious activity in a high-risk account. Segment-based thresholds improve true positive rates in high-risk populations while reducing alert noise in low-risk ones.

Metro Bank's 2024 FCA fine — £16.7 million — included findings that more than 60 million transactions worth over £51 billion were not monitored at all due to data and reconciliation failures. Segmentation that excludes accounts from monitoring entirely is the extreme version of this problem.

Scenario Coverage and Typology Mapping

Thresholds cannot compensate for missing scenarios. If your TM system has no rules configured for the money laundering typologies relevant to your business, no amount of threshold tuning will catch that activity.

Before tuning thresholds, map your active monitoring scenarios against current guidance for your jurisdiction:

- US — FinCEN's 2021 AML/CFT priorities and FinCEN advisories on ransomware, pig-butchering scams, and crypto kiosk abuse

- UK/EU — FCA financial crime guidance and FATF virtual asset red flags covering transaction patterns, anonymity tools, and geographic risks

- Canada — FINTRAC financial entity and virtual currency indicators covering structuring, wire transfers, and privacy coin activity

The FCA fined HSBC £63.9 million in 2021 with a specific finding that HSBC failed to consider whether its transaction monitoring scenarios covered relevant risks. A well-tuned rule for the wrong scenario adds no compliance value.

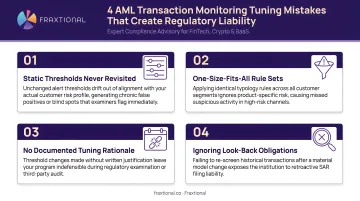

Common Mistakes When Tuning AML Transaction Monitoring

Most tuning failures aren't technical. They're operational. These four patterns consistently surface in examinations and enforcement actions:

Universal thresholds applied without segmentation — the most common structural flaw in TM programs, and the one most likely to draw regulatory criticism. What counts as unusual behavior is entirely relative to a customer's profile.

Threshold increases driven by alert volume, not alert quality — raising thresholds to reduce investigator workload without testing whether dropped alerts contained true positives. This mirrors the conduct FinCEN penalized U.S. Bank for, even when no formal alert cap exists.

Tuning treated as a one-time project — static parameters drift out of alignment as customer behavior shifts, new products launch, and typologies evolve. Institutions without a documented review cadence are exposed during examinations.

Missing rationale documentation — even well-executed tuning becomes a liability without working papers. Examiners expect to see data analyzed, thresholds tested, decisions justified, and independent validation completed. Absent documentation is an MRA risk on its own.

Conclusion

Tuning transaction monitoring is one of the highest-leverage activities in AML compliance. Done well, investigators spend time on genuine risk rather than noise, and regulators see a program built on data and documented judgment rather than static default settings.

The biggest failure points aren't technical — they're operational. The patterns that turn a functional TM system into a regulatory liability are consistent: poor segmentation, no review cadence, and undocumented threshold decisions. Each one is avoidable with the right ownership in place.

For institutions without in-house director-level AML expertise, fractional compliance leadership is a practical path forward.

Fraxtional places experienced BSA Officers and MLROs on a flexible basis. They can lead tuning engagements, oversee independent validation, and produce the working papers regulators will scrutinize — without the cost or commitment of a full-time hire.

Frequently Asked Questions

What is tuning in transaction monitoring?

Tuning is the process of adjusting an AML transaction monitoring system's thresholds, rules, and parameters so it generates alerts that accurately reflect genuine suspicious activity for your institution's specific risk profile — minimizing false positives without creating false negatives that let suspicious activity pass undetected.

What does transaction monitoring do?

Transaction monitoring continuously scans customer transactions against predefined rules and thresholds to identify patterns that may indicate money laundering, terrorist financing, or other financial crime. It generates alerts for compliance teams to investigate and, where warranted, report to regulators via SARs, STRs, or CTRs.

How often should transaction monitoring be tuned?

Under SR 11-7, model-qualifying systems require at least annual review; FFIEC guidance calls for periodic threshold evaluation; FINTRAC mandates effectiveness reviews at minimum every two years. Your actual cadence should reflect your jurisdiction, system complexity, and risk profile.

What triggers a transaction monitoring review outside the regular cycle?

Off-cycle reviews are warranted by:

- Rapid customer or asset growth, or M&A activity

- New high-risk products, services, or geographies

- A material shift in false positive or false negative rates

- Regulatory criticism of existing parameters

What is the difference between a SAR and a CTR in transaction monitoring?

A Currency Transaction Report (CTR) is a mandatory report filed for cash transactions above $10,000 in the US regardless of whether the activity appears suspicious. You file a Suspicious Activity Report (SAR) when a transaction or pattern (at any dollar amount) raises reasonable suspicion of money laundering or financial crime following an investigation.

What are the four pillars of a risk-based approach in transaction monitoring?

The four pillars are: (1) identifying and assessing inherent risks across customers, products, geographies, and channels; (2) designing controls proportionate to those risks; (3) implementing and operating those controls with regular tuning; and (4) reviewing and updating controls as risks evolve — always directing resources where risk is highest.