Introduction

Florida ranks among the most active financial services markets in the United States, and any business receiving or transmitting money on behalf of customers in the state—whether through digital payments, remittances, cryptocurrency exchanges, or embedded finance—must hold a Florida Money Transmitter License (MTL) issued by the Florida Office of Financial Regulation (OFR). Operating without one carries serious consequences: civil fines, cease-and-desist orders, and potential felony exposure under Chapter 560, Florida Statutes.

In March 2026, the OFR imposed a $155,000 administrative fine on Patriot Software for engaging in unlicensed money transmission activities while an application was pending. This enforcement action underscores a critical reality: Florida actively polices its money transmission sector, and compliance delays are expensive — and avoidable.

If you're building a fintech, operating a crypto exchange, or launching an embedded finance product in Florida, this guide breaks down exactly what the MTL requires — from application mechanics to ongoing obligations.

This article covers:

- Legal definition and scope of the Florida MTL

- Who qualifies and who is exempt

- The step-by-step application process

- Financial and AML requirements

- Ongoing obligations post-licensing

- Common pitfalls and enforcement risks

Key Takeaways

- Statutory definition: Florida's MTL covers any entity transmitting currency, monetary value, payment instruments, or virtual currency on behalf of others under Part II of Chapter 560

- Unique application system: Florida uses its own REAL System—not the NMLS portal used by 44 other states—so the process differs significantly from multistate applications

- Financial thresholds: $100,000 minimum net worth, a surety bond of $50,000 to $2 million (calculated at 2% of projected volume), and permissible investments equal to 100% of outstanding transmissions

- Realistic timeline: 3 to 6 months with no expedited review; incomplete applications or weak AML programs are the most common delays

- Post-licensing obligations: Biennial renewal, annual audited financials, OFR examinations, and parallel FinCEN MSB registration required

What Is a Florida Money Transmitter License?

Under F.S. § 560.103(24), the Florida MTL applies to any corporation, LLC, limited liability partnership, or qualified foreign entity that receives currency, monetary value, a payment instrument, or virtual currency to act as an intermediary between parties.

The defining test is unilateral control: if your business can unilaterally execute or indefinitely prevent a transaction, a license is required. That threshold — not transaction volume or business model — is what triggers the obligation.

Regulatory Framework

The MTL is a state-level license issued by the Florida Office of Financial Regulation (OFR) under Part II of Chapter 560, which governs Payment Instruments and Funds Transmission.

It does not replace federal FinCEN MSB registration — that is a separate, parallel federal obligation that must be satisfied independently.

Part II vs. Part III Activities

Chapter 560 divides money services activities into two parts:

- Part II: Money Transmitters and Payment Instrument Sellers

- Part III: Check Cashers and Foreign Currency Exchangers

A single Part II license authorizes both payment instrument sales and funds transmission activities without additional fees. For fintechs running multiple payment services — say, a wallet product alongside a remittance offering — this dual coverage under one license avoids duplicative applications and costs.

Who Needs a Florida MTL — and Who Is Exempt?

Any business transmitting money or monetary value on behalf of customers in Florida needs a license—regardless of where the company is headquartered. Florida's licensing obligation follows the customer's location, not where the business is incorporated or physically based.

Common Business Types That Require Licensing

- Fintech P2P transfer platforms

- Remittance and wire services

- Cryptocurrency exchanges with unilateral transaction control

- Payment facilitators that hold or move customer funds

- Bill payment services

- Digital wallet providers

Statutory Exemptions (Very Narrow)

F.S. § 560.104 provides only three exemptions:

- Banks, credit unions, and federally or state-chartered depository institutions

- The U.S. government and its agencies

- Florida state government and its political subdivisions

Critical Compliance Gap: Federal Exemptions Don't Apply

Florida does not recognize federal regulatory exemptions. Entities regulated by the CFTC or SEC that are excluded from FinCEN MSB registration are NOT automatically exempt from Florida's licensing requirement.

In a September 2023 OFR declaratory ruling (In Re: Intercam Futures, Inc.), a CFTC-registered firm was required to obtain a Florida license regardless of its federal regulatory status. For CFTC- or SEC-regulated firms operating in Florida, this means maintaining a separate state license even where federal registration is already in place.

The "Unilateral Control" Carve-Out

Businesses that provide payment technology or infrastructure without directly holding funds or having authority to execute or block transactions may fall outside the licensing definition. Examples include:

- White-label payment software providers

- API platforms that route payment instructions without custody

- Technology vendors that never touch customer funds

If your business operates in this gray zone, request a determination from the OFR before operating. Operating without a required license exposes the company to cease-and-desist orders, civil penalties of up to $10,000 per violation, and potential criminal referral under F.S. § 560.114.

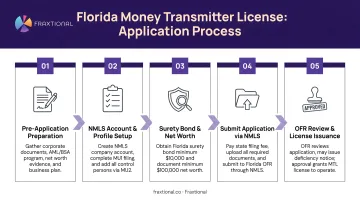

How to Apply for a Florida Money Transmitter License

The application is submitted through Florida's proprietary Regulatory Enforcement and Licensing (REAL) System—not through NMLS—and requires completing Form OFR-560-01 along with supporting documents. All fees are non-refundable and the OFR will not process your application until payment clears.

Step 1: Determine Eligibility

Assess whether your business model triggers the licensing definition—specifically whether you act as an intermediary with unilateral transaction control. If unclear, the OFR accepts written requests for declaratory statements before an application is filed. A declaratory statement gives you a documented regulatory position before you commit to the process.

Step 2: Prepare Core Application Documents

Required documents include:

- Articles of incorporation or organization

- Certificate of Good Standing from the Florida Division of Corporations

- Employer Identification Number (EIN)

- Registered agent details

- Audited financial statements for the most recent fiscal year

- Detailed business plan including flow of funds diagram

- Ownership and organizational structure disclosure

- Biographical summaries and employment history for all control persons

- Written AML program meeting 31 CFR § 1022.210 requirements

Step 3: Complete Background Checks for Control Persons

All control persons—including directors, officers, and anyone with 25% or more ownership—must submit fingerprints through an FDLE-approved Livescan vendor for state and federal criminal history checks. Past convictions, financial crimes, or prior regulatory violations may result in denial or conditional approval.

Pro tip: Initiate background checks early. Processing delays here are common and can extend your overall timeline.

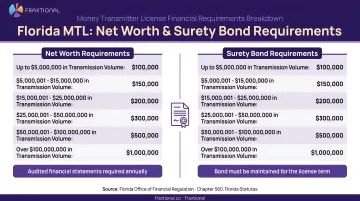

Step 4: Meet Financial Requirements and Obtain Surety Bond

Two financial thresholds must be documented before license issuance:

Net Worth Requirement:

- Minimum $100,000 for the main office

- Additional $10,000 per location up to $2 million

- Verified through audited financials

Surety Bond:

- Amount equal to 2% of projected first-year transmission volume

- Minimum $50,000, maximum $2 million

- Must be issued by an insurer authorized in Florida and pledged to the OFR

- Acceptable alternatives: certificate of deposit pledge agreement (Form OFR-560-05) or letter of credit

Step 5: Submit Application and Pay Fees

Fee Structure (F.S. § 560.143):

| Fee Type | Amount |

|---|---|

| Part II Application Fee | $375 |

| Branch Office (per location) | $38 |

| Authorized Vendor (per location) | $38 |

Plus per-person fingerprinting fees charged by the FDLE vendor.

After submission, the OFR may issue deficiency notices requesting additional information. Florida offers no expedited review track, so gaps in your submission directly extend the timeline. Total legal and compliance preparation costs typically range from $10,000 to $50,000, depending on business complexity.

With the application submitted, the next challenge is maintaining the license—annual renewals, permissible investments, and ongoing reporting each carry their own requirements.

Key Financial and Compliance Requirements

Permissible Investments Requirement

F.S. § 560.210 requires licensees to hold permissible investments with an aggregate market value equal to at least the total face amount of all outstanding money transmissions and payment instruments.

Qualifying investments include:

- Cash

- Certificates of deposit

- Investment-grade securities

- U.S. government obligations

- Money market mutual fund shares

Critical for crypto operators: Virtual currency is explicitly excluded from permissible investment calculations under Florida law. Licensees must hold virtual currency of the "same type and amount owed or obligated" until transmission is completed, but this does not satisfy the permissible investment requirement. Crypto-native businesses must maintain separate qualifying asset coverage.

AML Program Requirements

Your AML program must comply with 31 CFR § 1022.210 and F.S. § 560.1235, including:

- Written policies and procedures for detecting and preventing money laundering

- Designated compliance officer

- Employee training program

- Independent audit function

The OFR reviews the AML program during the initial application and will flag deficiencies as a basis for denial or delay. For early-stage fintech and crypto companies building these programs from scratch, many turn to an outsourced or fractional BSA Officer — someone who can own the compliance function without the commitment of a full-time hire.

Dual Reporting Framework

AML program obligations don't end with written policies — they extend into active transaction monitoring and reporting at both the state and federal level.

State-level obligations:

- Currency Transaction Records for transactions exceeding $10,000

- Suspicious Activity Reports (SARs) filed with FinCEN for transactions of $2,000 or more

Federal-level obligations:

- FinCEN Form 107 registration within 180 days of commencing operations

- Biennial renewal required regardless of state licensing status

Ongoing Financial Maintenance

Net worth and surety bond requirements must be maintained continuously, not just at application. Two risks to watch as your business scales:

- Volume increases may trigger an OFR request for a higher bond amount

- Lapsed bond coverage is grounds for immediate license suspension

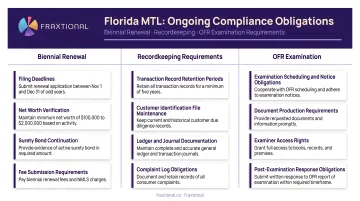

Ongoing Compliance Obligations for Florida MTL Holders

Biennial Renewal

The Florida MTL is valid for two years and must be renewed through the REAL System before the April 30 expiration date. The biennial renewal fee is $750.

At renewal, licensees must submit:

- Updated financial statements

- Confirmation of continued AML compliance

- Attestation of compliance with safe and sound practices under F.S. § 560.1115

Late renewals carry an additional $500 fee. If the license lapses beyond 60 days, a full new application is required.

Recordkeeping Obligations

F.S. §§ 560.211 and 560.1105 require licensees to maintain records for a minimum of five years:

- Daily transaction records

- Monthly financial institution statements

- Settlement records from authorized vendors

- Records of outstanding transmissions

- AML-related documentation

Willful failure to maintain required records is a third-degree felony.

OFR Examination Authority

F.S. § 560.109 grants the OFR broad examination powers:

- Must examine each licensee at least once every five years

- May conduct examinations without advance notice

- All books, records, compliance documentation, and financial reports must be available within three business days of written request

- Failed examinations can result in fines up to $10,000 per violation, suspension, or license revocation

OFAC and Federal Compliance Layer

Florida MTL holders carry concurrent federal obligations alongside state requirements:

- Screen all transactions in real time against OFAC sanctions lists

- Maintain active FinCEN MSB registration, renewed biennially

- File SARs for transactions of $2,000 or more that show indicators of money laundering

For companies operating at scale or in high-risk segments like cryptocurrency, these parallel state-federal obligations demand director-level compliance oversight. Fraxtional provides fractional CCO, BSA Officer, and CAMLO services — giving MTL holders experienced leadership without the cost of a full-time executive hire.

Frequently Asked Questions

What is a money transmitter in Florida?

Under F.S. § 560.103(24), a money transmitter is a corporation, LLC, or qualified foreign entity that receives currency, monetary value, payment instruments, or virtual currency as an intermediary. The definition specifically covers entities that can unilaterally execute or indefinitely prevent a transaction on behalf of another party.

Who needs to register as an MSB?

Federal MSB registration with FinCEN is required for money transmitters, currency dealers, check cashers, and other financial service providers operating above de minimis thresholds. State licensing and federal MSB registration are separate obligations that must both be satisfied.

How much does it cost to get a money transmitter license in Florida?

Core costs include:

- Application fee: $375 non-refundable

- Fingerprinting: charged per control person

- Surety bond premium: 1–5% of the required bond amount ($50,000–$2 million)

- Legal/compliance preparation: typically $10,000–$50,000 depending on business complexity

How long does it take to obtain a money transmitter license?

The typical timeline is 3 to 6 months from submission. Florida does not offer an expedited review option. Incomplete applications, inadequate AML programs, or complex ownership structures are the most common causes of delays.

How hard is it to get a money transmitter license?

The most challenging elements are meeting OFR's financial documentation thresholds and building an AML program that holds up to detailed scrutiny. Responding to deficiency notices within 30 days is also critical — delays at that stage are a common reason timelines extend beyond six months.

How do I register a money services business?

Florida state registration goes through the REAL System at the OFR Online Services Portal, not NMLS. Federal MSB registration is a separate filing with FinCEN using Form 107. Both are required if your business meets the applicable definitions under state and federal law.