Introduction

Nearly every fintech product you interact with — neobank accounts, embedded debit cards, instant payment features — runs on banking infrastructure the fintech doesn't own. At the center of that infrastructure sits a sponsor bank.

Most founders understand they need one. Far fewer understand how the relationship actually operates, what obligations it creates, or why so many fintechs fail to secure one in the first place.

Sponsor banks aren't passive infrastructure providers. They're regulated institutions that retain ultimate liability for everything their fintech partners do, and they vet applicants accordingly.

This guide covers what sponsor banks are, how the relationship works in practice, what due diligence looks like from the bank's side, and what fintechs need to demonstrate before approaching one.

Key Takeaways

- A sponsor bank gives fintechs access to regulated infrastructure (FDIC-insured accounts, payment rails, card network access) under its banking charter — no separate license required.

- The relationship is not passive: the bank retains regulatory accountability and monitors its fintech partners.

- Sponsor banks run thorough due diligence before approving any partnership, focusing heavily on compliance maturity and leadership credibility.

- Most application delays and rejections trace back to weak AML/BSA programs, missing KYC frameworks, or no designated compliance officer on the team.

What Is a Sponsor Bank?

A sponsor bank is a federally or state-chartered financial institution that partners with a non-bank fintech, giving that fintech access to regulated banking services — deposit accounts, payment rails, and card network infrastructure — all operating under the bank's charter.

Fintechs need this arrangement because they cannot, on their own, hold customer deposits, issue cards, or access payment networks like ACH, RTP, or FedNow. A banking license is required for all of the above. Sponsor banks fill that gap, allowing fintechs to build financial products within a compliant, regulated structure.

What a Sponsor Bank Is Not

Most founders misread this relationship. A sponsor bank is not:

- A silent or passive partner that simply provides infrastructure and steps back

- A technology vendor licensing you an API

- An entity that transfers regulatory responsibility to the fintech

- A buffer that absorbs compliance obligations on the fintech's behalf

The bank remains the regulated entity. As the 2024 OCC/FDIC/Federal Reserve joint statement makes clear, a bank remains responsible for compliance when it uses third parties to deliver deposit products. Regulatory accountability stays with the bank, always.

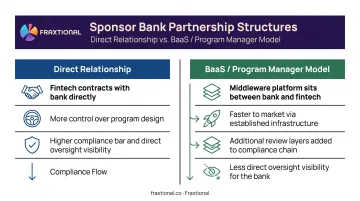

Two Main Structures

| Model | How It Works | Key Consideration |

|---|---|---|

| Direct relationship | Fintech contracts with the bank directly | More control, higher compliance bar |

| BaaS / program manager model | A middleware platform sits between the bank and fintech | Faster to market, but less direct oversight visibility |

Both structures carry active compliance obligations. The BaaS intermediary model doesn't reduce what the bank expects from the fintech — it adds another layer to the chain, which means more parties reviewing your program, not fewer.

How Does a Sponsor Bank Relationship Work?

The sponsor bank provides the regulatory foundation; the fintech provides the customer-facing product. Both parties carry active obligations throughout the life of the relationship.

The Sponsorship Structure

The sponsor bank holds the master charter and maintains regulatory relationships with bodies like the OCC, FDIC, Federal Reserve, or state banking departments. The fintech operates as a third-party program partner under the bank's supervision, bound by a formal program agreement that defines who owns which compliance and operational responsibilities.

Customer funds are typically held in pooled FBO (For Benefit Of) accounts at the sponsor bank. The bank is responsible for ensuring those funds are properly segregated and reconciled — a requirement under intense regulatory scrutiny since the Synapse collapse.

A court-appointed trustee found an $85 million shortfall between funds held at partner banks and balances owed to depositors. That gap illustrates exactly what happens when FBO ledger reconciliation breaks down.

Money Movement and BIN Sponsorship

Transactions initiated through the fintech's product route through the sponsor bank's payment rails. The bank processes and settles each transaction as the entity with network membership. The fintech handles the customer-facing experience.

For card programs, the sponsor bank provides the BIN (Bank Identification Number): the identifier embedded in card numbers that routes authorization requests through Visa or Mastercard. As Visa describes it, the BIN sponsor is the issuing bank that owns the number needed to access the network, holds cardholder funds, and manages risk and regulatory compliance.

Without BIN sponsorship from a licensed bank, a fintech simply cannot issue branded payment cards.

Oversight and Monitoring

The sponsor bank doesn't enable the fintech and step back. It monitors transaction flows, compliance controls, and customer onboarding practices on an ongoing basis. This typically involves:

- Shared reporting dashboards or regular data submissions

- Daily, weekly, or monthly transaction reporting obligations

- Periodic policy reviews and compliance program audits

- KYC and AML program assessments

The frequency and depth of this oversight varies significantly between banks. Misalignment between a fintech's expectations of autonomy and the bank's actual oversight requirements is one of the most common sources of friction in these partnerships.

What Compliance Obligations Do Sponsor Banks Impose on Fintechs?

Sponsor banks hold ultimate regulatory accountability. But the contract they sign with a fintech transfers specific, enforceable compliance obligations — and banks are increasingly willing to walk away from partners who can't meet them.

The enforcement record makes this concrete. In 2024 alone, the Federal Reserve issued an enforcement action against Evolve Bancorp for deficiencies in risk management and BSA/AML programs tied to fintech partnerships. The Fed fined Green Dot $44 million for consumer compliance breakdowns and BSA/AML deficiencies. Banking Dive tracked consent orders against Thread Bank, Lineage Bank, Piermont Bank, Sutton Bank, and others — all tied to fintech partner oversight failures.

Banks aren't facing these actions because they ignored their fintechs. They're facing them because regulators hold the bank accountable for what happens inside those partnerships.

The Core Compliance Obligations

KYC and Customer Identification (CIP)

Fintechs must implement a Customer Identification Program that meets the bank's minimum standards. The fintech typically owns day-to-day verification; the bank retains the right to review, audit, and override those controls.

BSA/AML Transaction Monitoring

Fintechs must maintain ongoing transaction monitoring to detect suspicious activity. Key obligations include:

- Filing Suspicious Activity Reports (SARs) where required

- Conducting OFAC sanctions screening on customers and transactions

- Maintaining documented escalation procedures

Who holds SAR filing responsibility — the fintech or the bank — varies by program agreement. Clarify this before signing anything.

Reporting and Data Obligations

Sponsor banks require regular compliance reporting: transaction data, onboarding metrics, flagged cases, and audit-ready documentation. Fintechs that can't produce clean, structured data on demand create regulatory exposure for both parties.

Designated Compliance Leadership

Because regulators hold the sponsor bank responsible for its fintech partners' failures, banks increasingly require fintechs to have a named compliance leader before approving a partnership. That means a CCO, BSA Officer, or CAMLO on record — someone who understands the obligations and can be held accountable.

This isn't a formality. Fintechs without credible, named compliance leadership are frequently rejected outright.

What Sponsor Banks Look for When Vetting Fintechs

Sponsor banks conduct formal due diligence before approving any relationship. The 2021 interagency fintech due diligence guidance outlines what banks assess:

| Due Diligence Area | What Banks Evaluate |

|---|---|

| Business experience | Operational history, references, regulatory track record |

| Financial condition | Capacity to perform, financial viability |

| Legal and regulatory compliance | BSA/AML, consumer protection, applicable laws |

| Risk management and controls | Policies, procedures, internal controls, audit evidence |

| Information security | Data protection, business continuity, incident response |

| Contractual readiness | Clear roles, audit rights, exit and termination planning |

Specific Compliance Signals Banks Assess

Banks focus hard on whether the fintech has:

- A documented, functional AML/BSA program

- A working KYC/CIP framework with clear procedures

- A named compliance officer with demonstrable accountability

- Evidence that leadership actually understands its regulatory obligations

They'll also review regulatory history, complaints, and adverse media on the fintech and its principals. Prior findings don't automatically disqualify a fintech — concealed ones do.

Risk Appetite Alignment

Compliance quality alone isn't sufficient. Some sponsor banks won't partner with fintechs in high-risk verticals — including:

- Crypto and digital assets

- Cannabis-adjacent finance

- Cross-border remittances

- Gambling and gaming payments

This holds regardless of compliance program strength. Fintechs need to qualify on both compliance maturity and the bank's strategic risk appetite.

How Fintechs Can Secure a Sponsor Bank Partnership

Securing a sponsor bank requires presenting yourself as a credible, low-risk partner — not shopping for the best deal. The compliance infrastructure needs to exist before you approach a bank, not as a condition you agree to build afterward.

What to Prepare Before Outreach

Banks expect to see a complete compliance package, not just a product deck. Before initiating contact, a fintech should have:

- A documented AML/BSA program: written policies, risk assessment, and procedures tailored to your product and customer base

- A functioning KYC/CIP framework with clear onboarding flows and documented verification standards

- Named compliance leadership: a CCO, BSA Officer, or equivalent who can engage directly with the bank's risk team

- A clear product description and customer profile so the bank understands exactly who you're serving and what transaction flows look like

- A financial model demonstrating viability — banks are taking on third-party risk and need confidence you'll still be operating in 18 months

Fraxtional, which works specifically with fintech and crypto companies on sponsor bank readiness, has seen how preparation quality drives outcomes. One client reported: "We had an AML policy, but it didn't hold up during a sponsor bank review. Fraxtional fixed it within days and helped us avoid a delay in onboarding."

Another noted: "Our sponsor bank required us to appoint a BSA Officer. Fraxtional came in, cleaned up our AML framework, and helped us pass review faster than we expected."

Well-prepared fintechs typically move through onboarding in under 60 days. Those building compliance from scratch mid-process should expect two to three months or longer.

Finding the Right Bank Fit

Knowing what to prepare is only half the equation. The other half is identifying banks whose risk appetite actually matches your product. Not all sponsor banks support all product types — some won't work with early-stage companies, and others have exited specific verticals under regulatory pressure. Before investing time in outreach and due diligence, research:

- The bank's existing fintech portfolio and product focus

- Whether the bank has a history of regulatory enforcement related to BaaS programs

- Whether its risk appetite aligns with the fintech's customer profile and product type

Many early-stage fintechs work with compliance advisors who maintain active sponsor bank relationships and know what a strong due diligence package looks like. Fraxtional's sponsor bank relationship services connect fintechs to pre-qualified banks based on product type and risk profile fit, with support through legal negotiation, compliance Q&A, and go-live.

Frequently Asked Questions

What does a sponsor bank do?

A sponsor bank provides a fintech with access to regulated banking infrastructure — payment rails, deposit accounts, and card network access — under its banking charter. It remains the regulated entity responsible for compliance oversight of the fintech partner and retains ultimate liability for the partnership's regulatory outcomes.

What is the difference between a sponsor bank and a regular bank?

A regular bank serves end consumers and businesses directly. A sponsor bank partners with non-bank fintechs as the licensed intermediary that makes their products legally and operationally possible — while typically still serving direct customers through a separate BaaS business line.

How does a fintech get approved by a sponsor bank?

Fintechs go through formal due diligence where the bank evaluates their compliance program, KYC/AML controls, compliance leadership, technology infrastructure, financial health, and business model. Approval hinges on compliance maturity and alignment with the bank's risk appetite — not just product viability.

What compliance requirements do sponsor banks impose on fintechs?

Core obligations include implementing a KYC/CIP program, maintaining BSA/AML transaction monitoring, conducting OFAC screening, filing SARs where required, and providing regular compliance reporting to the bank. Requirements are defined in the program agreement and are non-negotiable.

What is BIN sponsorship and how does it work?

BIN sponsorship is when a sponsor bank provides a fintech with a Bank Identification Number, allowing it to issue branded payment cards through Visa or Mastercard under the bank's network membership. Without a BIN sponsor, a fintech has no mechanism to route authorization requests through card networks and cannot issue cards.

Can a fintech work with multiple sponsor banks?

Yes. Fintechs do work with multiple sponsor banks to support different product types or geographies. Each relationship carries its own due diligence process, program agreement, compliance obligations, and ongoing oversight requirements — so operational complexity scales with each addition.