Introduction

PE-backed fintech, banking, and financial services portfolio companies operate in heavily regulated environments where a single compliance failure can destroy deal value overnight. A BSA/AML violation, sponsor bank termination, or regulatory enforcement action doesn't just trigger fines: it can render a business model non-viable, collapse valuations, or derail an exit entirely.

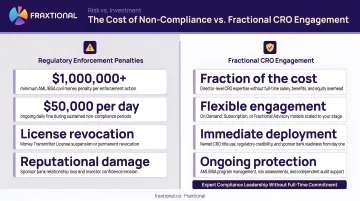

Regulatory enforcement against fintechs reached $19.3 billion globally in 2024, with individual penalties climbing into the billions for institutions like Binance ($4.3B) and TD Bank ($3B+). For PE firms, operational risk in regulated portfolio companies is a core value driver that demands specialized executive oversight.

Most PE firms lack the in-house expertise to assess or manage fintech compliance risk effectively. Operating partners skilled in finance and operations rarely possess the domain-specific knowledge required to navigate BSA/AML, UDAAP, Reg E, state money transmission licensing, or sponsor bank relationship management.

That gap leaves deal teams exposed on one of the most consequential risk factors in the portfolio. Median hold periods now stretch beyond 6.5 years, meaning portfolio companies must survive multiple regulatory examination cycles before any exit becomes viable.

This guide covers what an interim Chief Risk Officer actually does in a PE context, why regulated portfolio companies need one, and which deal lifecycle scenarios trigger demand. It also addresses what to look for when hiring and how the economics compare to a full-time hire.

Key Takeaways

- Interim CROs deliver director-level regulatory expertise to PE-backed fintech, banking, and crypto companies without the cost or commitment of a permanent executive

- Covers the full deal lifecycle: pre-deal due diligence, post-acquisition infrastructure builds, crisis management, and exit preparation

- Engages within days or weeks, compared to 3–6 months for a traditional executive search

- Selection criteria: BSA/AML, UDAAP, Reg E expertise; PE portfolio experience; credibility with sponsor banks and regulators

- Delivers strong ROI: regulatory penalties, sponsor bank terminations, and failed exits far exceed interim CRO engagement costs

What Is an Interim CRO in the Private Equity Context?

Defining the Role: Chief Risk Officer, Not Chief Revenue Officer

In financial services and fintech, CRO stands for Chief Risk Officer—the senior executive accountable for identifying, managing, and mitigating regulatory, compliance, operational, and financial risk across the organization. According to the Basel Committee on Banking Supervision, a bank's CRO should be independent of individual business lines and report directly to the CEO and board of directors.

Interim or fractional means the CRO is engaged for a defined period or on a part-time basis, providing director-level oversight without a permanent employment commitment. Interim CROs are typically dedicated full-time to one company for a fixed engagement window, while fractional CROs work part-time across multiple clients simultaneously.

Both models eliminate long-term equity dilution and severance exposure while delivering the same depth of oversight as a full-time hire.

Core CRO Responsibilities in PE Portfolio Companies

In PE-backed fintech and financial services companies, the CRO's mandate includes:

- Building and maintaining the risk framework: BSA/AML program, UDAAP compliance, Reg E, privacy, cyber risk

- Managing regulatory relationships: Serving as the primary point of contact for regulators, examiners, and auditors

- Overseeing internal controls: Ensuring transaction monitoring, sanctions screening, and SAR filing obligations are met

- Sponsor bank management: Acting as the compliance counterpart for sponsor bank partners who require evidence of robust risk controls

The Federal Reserve defines the U.S. CRO role as responsible for overseeing the measurement, aggregation, and monitoring of risks, with direct reporting to the risk committee and global CRO.

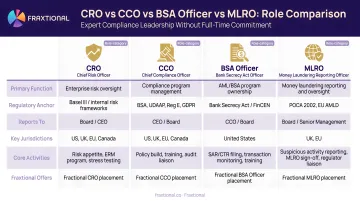

CRO vs. Adjacent Compliance Roles

The CRO is distinct from—but sometimes bundled with—other compliance leadership roles:

| Role | Primary Focus | Regulatory Definition |

|---|---|---|

| Chief Risk Officer (CRO) | Enterprise-wide risk governance and independent oversight | Must have sufficient stature, independence, resources, and board access to oversee all material risks |

| Chief Compliance Officer (CCO) | Compliance program management and regulatory adherence | Ensures the firm operates with integrity and in compliance with laws and policies |

| BSA/AML Officer | Bank Secrecy Act and Anti-Money Laundering program administration | Must be a designated qualified individual with appropriate authority and independence (OCC Bulletin 2025-37a) |

| MLRO/CAMLO | Money laundering reporting and AML strategy (UK/EU/Canada) | Responsible for coordinating AML program and serving as regulatory point of contact |

In practice, these boundaries often blur for smaller fintech organizations. An interim CRO may carry multiple mandates depending on the company's regulatory footprint and jurisdictions. OSFI guidance explicitly warns, however, that bundling roles must not compromise the independence the CRO position requires.

Why PE-Backed Fintech and Financial Services Companies Need Interim CRO Leadership

Regulatory Complexity That Generalist Operators Can't Handle

Fintech, banking, and crypto portfolio companies operate under overlapping regulatory regimes: BSA/AML, OFAC sanctions, state money transmission licensing, UDAAP, Reg E, and privacy law. Enforcement scrutiny far exceeds what most industrial or consumer businesses face. U.S. regulators issued 42 BSA/AML-related enforcement actions in 2024, up from 29 in 2023.

Unlike operational headaches in other sectors, a compliance failure in a regulated fintech is an existential event. The consequences:

- Binance: $4.3 billion penalty for willful failure to implement effective AML programs and unlicensed money transmission

- TD Bank: $3 billion+ global resolution, including a $1.3B FinCEN penalty for failing to file over 6,000 SARs

- Canaccord Genuity: $80 million penalty, the largest BSA fine ever levied on a broker-dealer

Most PE operating partners simply don't possess the domain expertise to assess or remediate these risks.

The Sponsor Bank Dependency Problem

Most fintech and embedded finance companies depend on sponsor banks for their ability to operate—and regulators now require evidence of robust compliance infrastructure as a condition of those partnerships. The June 2023 Interagency Guidance on Third-Party Relationships places ultimate responsibility on the bank's board for third-party risk management, pushing sponsor banks to actively offboard fintech partners that lack institutional-grade controls.

Recent examples:

- Blue Ridge Bank: Following an OCC consent order, the bank offboarded about a dozen of its roughly 50 BaaS partners to reduce fintech exposure

- Lineage Bank: The FDIC ordered the bank to develop a plan for orderly termination of significant third-party fintech partners within 60 days

- Evolve Bank & Trust: The Federal Reserve issued a cease-and-desist order citing unsafe practices for failing to have an effective risk management framework for fintech partnerships

A portfolio company without credible compliance leadership can lose its sponsor bank relationship overnight, effectively shutting down operations.

Common Post-Acquisition Failure Modes

PE due diligence frequently misses deep-seated compliance gaps. Common failure modes include:

Unregistered Money Transmission: Fintechs operating without MSB registration face criminal liability. Paxful was fined $3.5 million for failing to register, while Brink's Global Services paid $37 million for the same violation.

BSA/AML Program Gaps: Inadequate customer due diligence and SAR filing failures are epidemic. TD Bank's $1.3B FinCEN penalty resulted from willfully failing to file over 6,000 SARs.

Undisclosed Regulatory Exposure: In a landmark 2025 case, White Deer Management's junior diligence team overlooked historical sales agent agreements with Iran when acquiring Unicat—only avoiding prosecution through voluntary disclosure under the DOJ's M&A Safe Harbor policy.

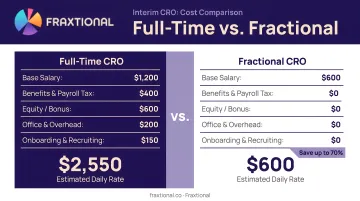

The Economic Case for Fractional Leadership

Full-time CRO compensation in PE-backed fintech companies is substantial. Median base salaries reached $245,000 in 2025—a 16% increase from 2023—while PE-backed CRO roles command $300,000–$450,000 base, excluding bonus and equity.

Interim and fractional CROs deliver equivalent expertise at a fraction of the cost. Rates vary by market:

| Role | Daily Rate | Market |

|---|---|---|

| Regulatory consultant | $2,000–$5,500 | US |

| Interim CRO/CCO (scale-up) | £1,000–£1,500 | UK/EU |

| Interim CRO/CCO (enterprise/PE-backed) | €1,700–€2,300 | EU |

At these rates, a 100-day post-close remediation sprint costs far less than the nine-figure penalties regulators levy for compliance failures. It also eliminates the long-term equity dilution and severance risk that come with a full-time hire.

When to Deploy an Interim CRO: Key Scenarios Across the Deal Lifecycle

Unlike general interim CEOs — typically deployed reactively — interim CROs can and should be deployed proactively at multiple points throughout the PE deal lifecycle. Regulatory risk compounds when left unaddressed.

With median hold periods reaching 3.4 years and averages exceeding 6.5 years, portfolio companies face prolonged regulatory scrutiny before exit. Getting ahead of that exposure — rather than reacting to it — is what separates clean exits from distressed ones.

Pre-Deal Compliance Due Diligence

Timeline: 2–4 weeks before deal close

An interim CRO can conduct a commercial and compliance due diligence sprint to assess:

- Credibility of the target's existing compliance program

- BSA/AML gaps and regulatory exposure

- Status of ongoing regulatory investigations

- Stability of sponsor bank relationships

- Capability of existing compliance leadership to execute post-close

Output: A risk-adjusted view of the target that informs deal pricing, reps and warranties scope, and post-acquisition priorities. PE firms with strong financial modeling capabilities rarely have the fintech compliance depth to conduct this assessment accurately — and that gap produces costly surprises post-close.

Post-Acquisition Risk Infrastructure Build

Timeline: 6–12 months

Many acquired fintechs lack the compliance infrastructure institutional investors and sponsor banks require. The interim CRO's mandate:

- Assess existing controls against regulatory expectations

- Identify gaps in BSA/AML, KYC/KYB, UDAAP, Reg E, privacy, and cyber risk

- Build or rebuild the compliance program to institutional standards

- Establish transaction monitoring, sanctions screening, and SAR filing workflows

- Document policies, procedures, and risk frameworks

The fractional model fits this phase well. The portfolio company gets continuous director-level oversight through the critical build phase without locking in a permanent C-suite hire before the program has matured enough to define what that hire should look like.

Regulatory Crisis and Turnaround Management

Timeline: Immediate deployment, typically 6–12 months

Crisis scenarios include enforcement actions, covenant breaches triggered by compliance failures, or imminent sponsor bank termination. The interim CRO functions like a Chief Restructuring Officer:

- Assumes direct ownership of the compliance situation from day one

- Communicates with regulators or bank partners on behalf of the company

- Implements corrective action plans and remediates control gaps

- Restores credibility with regulators, sponsor banks, and investors

Speed matters more here than in any other scenario. A permanent hire takes 3–6 months to recruit and onboard — time a company in crisis simply doesn't have. An experienced interim CRO can step in within days and begin stabilizing the situation immediately.

Exit Preparation

Timeline: 12–18 months before planned exit

Buyers increasingly conduct deep compliance due diligence. A portfolio company that cannot demonstrate a mature, well-documented compliance program will receive a lower valuation multiple or face deal-breaking conditions. The interim CRO focuses on:

- Ensuring all regulatory registrations and licenses are current

- Confirming BSA/AML and risk frameworks are fully documented and defensible

- Producing a clean compliance track record narrative

- Preparing the compliance team and documentation for buyer scrutiny

Starting this work 12–18 months out matters because compliance gaps don't close quickly. Issues surfaced by a buyer's diligence team at the 11th hour are far more damaging — to deal terms and to negotiating leverage — than the same issues identified and resolved a year earlier.

What to Look for in an Interim CRO for a PE Portfolio Company

Regulatory Specialization Over Generalism

The most effective interim CROs bring deep, specific expertise in the applicable regulatory regimes:

- BSA/AML: Program design, SAR filing, transaction monitoring, CDD/EDD

- UDAAP: Unfair, deceptive, or abusive acts or practices (CFPB enforcement)

- Reg E: Electronic Funds Transfer Act compliance

- State money transmission licensing: Multi-state registration and compliance

- Privacy law: CCPA, GDPR, consumer data protection

- Cyber risk: Information security and breach response

Cross-border experience (U.S., UK, EU, Canada) is essential for global fintech portfolios. Avoid generalist risk advisors who lack hands-on regulatory compliance experience in the specific business model—embedded finance, crypto, payments, or lending.

PE Environment Experience and Sponsor Bank Credibility

The most impactful interim CROs have:

- Worked inside PE-backed companies — they understand reporting cadence, investor expectations, and decision-making pace

- Established credibility with sponsor banks and regulators, so trust restoration in a crisis starts from day one

- Navigated high-pressure timelines tied to deal cycles, audits, or regulatory deadlines

In a crisis, the CRO's track record with regulators and banks matters as much as their technical expertise.

Hands-On Operator, Not Slide-Deck Consultant

Effective interim CROs in PE contexts build programs, write policies, run training, engage directly with examiners, and implement corrective actions. They don't simply produce reports and leave execution to an overwhelmed internal team.

Look for evidence of:

- Policy and procedure authorship

- Direct regulator and examiner interaction

- SAR preparation and filing oversight

- Transaction monitoring system implementation

- Audit and examination preparation

When evaluating candidates, ask for specific examples from each area above. A strong interim CRO should be able to name the programs they built, the examiners they faced, and the outcomes they delivered.

The Economics of Interim CRO Engagements

Cost Comparison: Full-Time vs. Interim

Full-Time CRO Compensation (2025–2026 data):

- Median base salary: $245,000 (16% increase from 2023)

- PE-backed CRO base range: $300,000–$450,000

- Total compensation (including bonus/equity): Can exceed $2M+ at large firms

Interim/Fractional CRO Rates:

- U.S. regulatory consultants: $2,000–$5,500/day

- UK/EU interim CRO (scale-up): £1,000–£1,500/day

- EU interim CRO (enterprise/PE-backed): €1,700–€2,300/day

The fractional model eliminates long-term equity dilution, severance exposure, and the cost of a failed permanent hire.

The Cost of Inaction

A single enforcement action or compliance failure typically exceeds the total cost of a multi-year fractional CRO engagement:

- Binance: $4.3B penalty

- TD Bank: $3B+ global resolution

- Canaccord Genuity: $80M penalty

- Paxos Trust: $26.5M settlement for AML failures and insufficient diligence

Beyond fines, the cost of a sponsor bank termination—loss of the banking relationship that enables the business model—is existential. For most PE-backed fintech and crypto firms, a single quarter of fractional CRO coverage costs less than one day of regulatory counsel during an active enforcement investigation.

Engagement Model Flexibility

Interim CRO engagements can be structured as:

- Short-term advisory sprints: Due diligence, crisis response (2–4 weeks)

- Mid-term program builds: Post-acquisition infrastructure (6–12 months)

- Ongoing fractional arrangements: Continuous oversight spanning the full hold period

This flexibility allows PE firms to right-size the compliance investment to the risk profile and stage of the portfolio company. Fraxtional structures engagements around each portfolio company's licensing obligations, transaction volumes, and regulatory history — so the investment scales with actual risk exposure, not a fixed retainer.

How to Engage an Interim CRO for Your Portfolio Company

Define the Engagement Before the Search

Successful interim CRO deployments begin with clear scope definition:

- Which regulatory regimes apply? (BSA/AML, UDAAP, Reg E, state licensing, cross-border)

- What is the current compliance maturity level?

- What is the primary mandate? (Due diligence, build, crisis, exit prep)

- What is the target engagement duration?

PE firms that skip this step often end up with misaligned mandates and engagements that stall — a costly detour when deal timelines are already compressed.

Typical Deployment Timeline

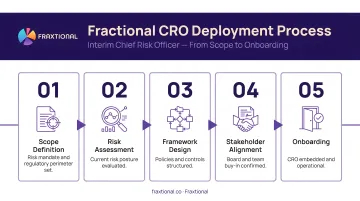

Unlike permanent executive searches (3–6 months), a qualified interim CRO can typically be deployed within days to a few weeks. The process:

- Scope definition: Clarify regulatory requirements and engagement mandate

- Candidate identification: Match expertise to regulatory regimes and business model

- Reference and credential validation: Verify track record with regulators and sponsor banks

- Engagement letter: Finalize terms and deliverables

- Onboarding: Begin assessment and stakeholder engagement

Fraxtional's pre-vetted director-level compliance experts can move from scope call to active engagement in as little as one to two weeks — useful when a portfolio company needs coverage ahead of a regulatory exam or closing deadline.

Set Clear Performance Milestones

Establish a 30/60/90-day milestone framework:

- Day 30: Complete compliance assessment, identify critical gaps, and prioritize remediation

- Day 60: Implement corrective actions, remediate high-priority gaps, and document progress

- Day 90: Deliver measurable compliance program improvements, stakeholder reporting, and transition plan

PE operating partners should review deliverables at each milestone gate — if Day 60 outputs don't reflect the original mandate, that's the right moment to recalibrate scope before the final sprint.

Frequently Asked Questions

What is a PE-backed portfolio company (PortCo)?

A PortCo is a company owned (fully or partially) by a private equity firm, typically acquired through a leveraged buyout or growth equity investment. The PE firm actively participates in governance and value creation until an exit event—IPO, strategic sale, or secondary transaction.

What is the typical exit timeframe for a private equity firm in an LBO deal?

Traditional LBO hold periods targeted 4–6 years, but hold periods have extended significantly. The median hold period reached 3.4 years at the end of 2024, while the typical portfolio company is now held on average for more than 6.5 years.

Why hire an interim CRO instead of waiting for a permanent one?

Regulatory risk doesn't wait for hiring processes to conclude. Enforcement actions, sponsor bank reviews, and buyer due diligence timelines are fixed. An interim CRO can be deployed immediately to manage risk while a permanent search proceeds in parallel—preventing value destruction during the transition.

What does an interim Chief Risk Officer actually do for a PE portfolio company?

An interim CRO steps in as the named compliance executive—assuming legal and regulatory accountability—and typically covers:

- Building and overseeing the BSA/AML, KYC, UDAAP, and Reg E framework

- Managing regulatory relationships and sponsor bank oversight

- Identifying and remediating compliance gaps

- Providing ongoing risk reporting to the board and PE firm

How long does an interim CRO engagement typically last in a PE context?

Duration varies by mandate:

- Due diligence sprints: 2–4 weeks

- Post-acquisition program builds: 6–12 months

- Fractional arrangements: the full PE hold period

Scope and timeline can be adjusted as the portfolio company's needs evolve.

What is the difference between a fractional CRO and an interim CRO?

An interim CRO is typically dedicated full-time to one company for a fixed engagement window, while a fractional CRO works part-time across multiple clients simultaneously. Both provide director-level expertise without a permanent hire commitment—the right model depends on the portfolio company's complexity and risk profile.