Introduction

Users expect to open a fintech account in minutes. Regulators expect KYC verification, AML checks, and risk assessments before a single transaction clears. That gap — between what users want and what compliance requires — is where most fintech onboarding breaks down.

According to Signicat's 2022 Battle to Onboard research, which surveyed 7,600 adults across 14 European markets, 68% of consumers had abandoned a financial application — and the average user quit after just 18 minutes and 53 seconds, down from 26 minutes in 2020. That's direct revenue lost before a single account opens.

This article covers the root causes of onboarding failure, how compliance requirements create unnecessary friction, and six practical strategies to build an onboarding flow that converts — without regulatory shortcuts.

Key Takeaways

- Onboarding drop-off is a revenue problem — users abandon in under 19 minutes when friction spikes

- KYC, AML, and KYB requirements set a compliance floor you can't remove, but the flow around them is fully designable

- Progressive profiling, risk-tiered flows, and inline verification are the most effective tools for reducing drop-off

- Without dedicated compliance expertise, early-stage fintechs routinely build flows that fail on both conversion and regulatory grounds

What Is Fintech Onboarding?

Fintech onboarding is the full journey from a user's first sign-up to becoming an active, verified account holder. It covers registration, identity verification, account linking, and activation. Unlike SaaS onboarding, the compliance steps aren't optional — KYC, KYB, and AML checks are legally required before users can transact.

The Standard Onboarding Stages

Most fintech onboarding flows move through five stages:

- Sign-up/registration — email, phone, basic personal details

- Identity verification — KYC (individual) or KYB (business)

- Risk assessment — transaction volume, geography, business model

- Account setup — preferences, funding, product configuration

- Activation — first meaningful transaction or product action

Friction can enter at any stage. In practice, it usually enters at stage two.

Consumer vs. B2B Onboarding

Consumer fintech onboarding (individual KYC) is demanding but manageable. Most users have a phone and a government ID, so the process is largely self-serve. B2B onboarding is a different challenge. Verifying a business means confirming legal entity status, UBO structures, source of funds, and control-person data. Documents require offline preparation and multiple stakeholders. That's why B2B onboarding abandonment runs materially higher than consumer flows, and why the design stakes are much greater.

Why Fintech Onboarding Fails: The Root Causes

Most onboarding failures trace back to the same handful of avoidable decisions.

Front-Loading Everything

The most common mistake: asking for everything at once before the user has seen any product value. ID, SSN, business registration, beneficial ownership structures, bank details — all on screen before page two.

Incognia's Fintech Onboarding Friction Index, which studied 10 popular fintech mobile apps, found average onboarding required 14 screens, 16 fields, and 29 clicks. Average completion time was 6 minutes — with some apps hitting 11 minutes before a user was even inside the product.

No Explanation for Sensitive Data Requests

When a user hits a screen asking for their Social Security number or a photo of their passport with no explanation, it reads as invasive. The compliance rationale that's obvious to your team is invisible to your user. Drop-off spikes at exactly these moments.

Verification Waits With No Feedback

After document submission, many platforms go silent. No status bar, no ETA, no next step. The Incognia study found some apps, including Robinhood and Acorns, told users account validation could take 2 to 3 days — with no interim status updates. For a user who just handed over sensitive documents, silence feels like something went wrong.

One Flow for Everyone

A gig worker applying for a spending account, a startup founder opening a business account, and a high-net-worth individual moving significant assets all face identical onboarding flows in many fintech products. Their risk profiles and documentation requirements are completely different. Applying the same friction to every user punishes the low-risk majority — the ones most likely to abandon.

No Save-and-Resume

This one hits B2B flows hardest. Business registration documents, UBO confirmations, and source-of-funds evidence don't live in a user's back pocket. When they have to stop mid-flow to gather documents and find no way back in, they just don't return.

The Compliance Layer: Where Onboarding Actually Breaks Down

The Compliance Floor Problem

KYC, AML, and KYB requirements establish a minimum data collection threshold that product teams can't simply remove. The challenge isn't eliminating this floor — designing around it is. Every decision to skip a compliance step trades short-term conversion for long-term regulatory exposure. The goal is proportionate, intelligent design, not less compliance.

Multi-Jurisdictional Fragmentation

A fintech operating across multiple jurisdictions must maintain materially different verification flows and data-handling rules for each market:

- US: BSA/AML, PATRIOT Act CIP requirements

- UK: FCA rules, MLRO obligations

- Canada: FINTRAC/PCMLTFA requirements

- EU: GDPR, AML Directives

The BIS Project Mandala framework describes how these disparate regulatory frameworks introduce uncertainty, slow cross-border transactions, and complicate data collection — all of which surface directly in the onboarding flow.

The cost of getting this wrong is significant. LexisNexis Risk Solutions reported $206.1 billion in global financial-crime compliance costs for financial institutions in 2023 , with $61 billion in the US and Canada alone. Multi-jurisdictional complexity is a major driver of that number.

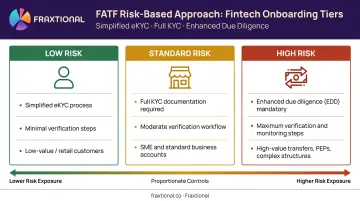

The Risk-Based Approach

FATF defines a risk-based approach (RBA) as identifying, assessing, and understanding money laundering and terrorist financing risks , then applying mitigation measures proportionate to those risks. In practical onboarding terms: low-risk users face lighter verification, high-risk users receive enhanced due diligence (EDD), and everyone in between gets calibrated accordingly.

This isn't just a UX preference — it's the authoritative regulatory framework. Correct RBA implementation means defining your risk tiers before building your flow, so the verification depth each user encounters matches their actual risk profile, not a default worst case.

KYB Complexity in B2B Flows

KYB verification requires confirming legal entity status, beneficial ownership structures (typically individuals holding 25%+ ownership), and sometimes source of funds. Unlike consumer KYC, this demands documents most business owners don't have on hand, and often requires input from multiple people within the organization.

Poor orchestration is where B2B flows collapse. Asking for UBO data before confirming entity status, or requesting source-of-funds evidence before the user understands why, is the single largest driver of B2B onboarding abandonment.

The Early-Stage Compliance Gap

Many seed and Series A fintechs design their onboarding flows without adequate compliance expertise on the team. The result is one of two failure modes: over-collection that frustrates low-risk users, or under-collection that creates regulatory exposure.

This is where fractional compliance leadership becomes practical. A fractional CCO, BSA Officer, or CAMLO from a firm like Fraxtional can design a compliant onboarding architecture, including CIP program design, risk classification criteria, and AML policy documentation, without the cost or commitment of a full-time executive hire. One Series A founder put it directly: the fractional team "wrote our policies and procedures, and completely embedded with our full-time team in a way that was seamless."

6 Strategies to Improve Your Fintech Onboarding Experience

1. Progressive Profiling (Not Progressive Disclosure)

Progressive profiling means deferring data collection to the point of actual need — not just showing or hiding form fields on a single screen.

- Collect email to create an account

- Request SSN only when a brokerage or high-value account is opened

- Require proof of address before the first transaction, not at registration

This is meaningfully different from rearranging your existing form. It requires compliance and product teams to agree upfront on what's needed at each product milestone.

2. Inline Verification and Real-Time Feedback

Redirecting users to external verification platforms kills momentum. Embedding document capture (camera/OCR), biometric checks, and live validation directly into the onboarding flow keeps the experience intact.

Equally important: instant feedback on document quality. "Your ID image is too blurry — try again" prevents the delayed-rejection cycle where a user submits a document, waits two days, gets rejected, and never returns.

3. Transparent Microcopy Around Compliance Steps

Replace generic labels with human, contextual copy:

| Generic (Avoid) | Contextual (Use) |

|---|---|

| "Upload ID" | "We need a photo of your passport to verify your identity — required by law to protect your account" |

| "SSN required" | "Your Social Security number lets us confirm your identity and meet federal reporting requirements" |

| "Additional verification needed" | "Because you're transferring over $10,000, we need one more document to complete your verification" |

Each sensitive data request should include a one-line rationale. The compliance reason is there — just make it visible.

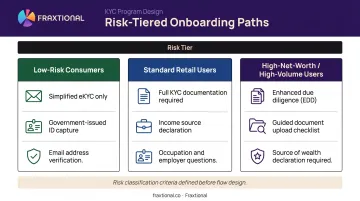

4. Risk-Tiered Onboarding Flows

Build separate paths for different risk segments:

- Low-risk consumers: simplified eKYC, email + ID verification

- Standard retail users: full KYC with income or occupation questions

- High-net-worth or high-volume users: enhanced due diligence with clear guidance on what's needed and why

This requires compliance and product to define risk classification criteria before a single screen is designed — not after.

5. Save-and-Resume With Re-Engagement Triggers

Allow users to exit mid-flow and return to their exact position, tied to an email captured at sign-up. This is non-negotiable for B2B onboarding where document preparation happens offline, over hours or days.

Nudges sent within an hour of drop-off improve completion rates — something like: "You're 70% done. Here's the one document you need to finish." No fintech-specific benchmark exists for this, but the underlying behavior is well-documented: the faster the re-engagement, the higher the recovery rate.

6. Mobile-First Design With Device-Native Capabilities

Most fintech sign-ups now start on a phone. Onboarding flows need to use what mobile devices actually offer:

- Camera for document scanning and selfie capture

- Biometrics for authentication

- Autofill for address and contact fields

- Single-action screens — one question, one step, one tap to proceed

Each additional friction point on mobile has an outsized abandonment cost compared to desktop. Design mobile flows as the primary experience, not a reduced version of the web flow.

What the Best Fintech Onboarding Flows Have in Common

The most effective fintech onboarding flows — Wise, Monzo, Chime, Mercury — share one structural principle: they separate the minimum viable sign-up from the full compliance verification process.

Get the user inside the product first. Complete verification in context, just before the first high-value action.

Wise applies this explicitly: its verification method and timing depend on factors like the amount being transferred, the currency, and the destination country. Low-value transfers need less verification. Higher amounts trigger additional steps. The compliance is there — it just appears when it's contextually relevant.

Framing Compliance as Value, Not Process

The best flows reframe compliance steps as product features:

- Identity verification = "protecting your funds"

- Document upload = "unlocking higher transfer limits"

- Enhanced checks = "enabling cross-border transfers"

This isn't spin — it's accurate. The compliance step genuinely delivers that benefit. Writing the copy that way changes how users experience it.

Building Compliance Into Design From the Start

The highest-converting onboarding flows are built by teams where compliance and product work together from the beginning. When compliance reviews a finished flow and raises objections at the end, the result is predictable: over-collection, added friction, and abandonment.

For early-stage fintechs that can't justify a full-time compliance executive, fractional leadership solves this structurally. Fraxtional embeds a Director-level CCO, BSA Officer, or CAMLO directly with the product team, so compliance input shapes the onboarding architecture from the first wireframe. That means:

- Fewer fields collected upfront (only what's required at each stage)

- Verification steps tied to actual risk triggers, not default caution

- KYC flows that satisfy regulators without frustrating users

Frequently Asked Questions

What is onboarding in fintech?

Fintech onboarding is the process by which a new user registers, verifies their identity (via KYC or KYB), links financial accounts, and becomes an active, compliant account holder. Unlike standard SaaS onboarding, regulatory verification steps are legally required and create inherent friction that cannot be eliminated. They can only be designed around.

What are the 5 stages of the onboarding process?

The five stages are: sign-up and registration, identity verification and compliance checks, account setup and personalization, activation via the first meaningful product action, and habit formation. Stage two is uniquely complex in fintech — regulatory requirements vary by jurisdiction, product type, and user risk profile.

What causes drop-off during fintech onboarding?

The main causes are front-loaded data demands, lack of transparency around why sensitive information is needed, long verification waits with no status feedback, and the absence of save-and-resume for multi-session flows. B2B onboarding is particularly vulnerable because business document collection requires offline preparation that a single session can't accommodate.

How does KYC/AML compliance affect the onboarding experience?

KYC and AML requirements create a mandatory data collection minimum that cannot be removed. It can, however, be designed around through risk-based verification (collecting less from low-risk users), progressive profiling (collecting data at the point of need), and transparent microcopy that explains why each step is required — so compliance doesn't feel like an obstacle.

What is a risk-based approach to fintech onboarding?

A risk-based approach means segmenting users by risk profile — geography, transaction volume, business type, and ownership complexity — then calibrating verification depth accordingly. Low-risk users see fewer steps; high-risk users receive enhanced due diligence. FATF's guidelines establish the standard framework for AML/KYC program design.

How can early-stage fintechs build compliant onboarding without a full compliance team?

Most seed and Series A fintechs engage fractional compliance officers — CCO, BSA Officer, or CAMLO — to design compliant onboarding architecture without the cost of a full-time hire. Fraxtional, for example, delivers Director-level compliance leadership across these roles, including CIP program design and AML policy documentation built to meet sponsor bank and regulatory standards.