This guide is for fintech startups, payment companies, crypto firms, and embedded finance businesses entering or operating in Florida. The stakes are high: operating without a license isn't a paperwork issue — it's a criminal offense. Unlicensed money transmission can trigger felony charges and civil penalties up to $25,000 or the value of funds involved, plus OFR administrative fines.

What follows is a practical checklist covering what you need, how to apply, and what comes after approval.

Key Takeaways

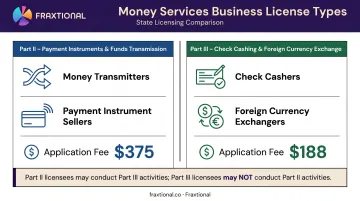

- Florida MTLs fall under Part II (money transmitters, payment instrument sellers) or Part III (check cashers, foreign currency exchangers) of Chapter 560

- Financial thresholds: $100,000 minimum net worth and a surety bond of $50,000–$2,000,000 depending on transaction volume

- Compliance prerequisites: written AML program, FinCEN MSB registration, and fingerprinting for all control persons

- Submit applications through the OFR's REAL portal; fees are $375 (Part II) or $188 (Part III)

- Post-licensing: designate a compliance officer within 90 days, submit annual financial audits within 120 days of fiscal year-end, maintain 5-year records

- FinCEN MSB registration does not substitute for Florida's state-level license — both are required

What Is the Florida Money Transmitter License?

Under Florida Statutes §560.103(24), a money transmitter is any corporation, LLC, LLP, or qualified foreign entity that receives currency, monetary value, a payment instrument, or virtual currency — then transmits it to another person or location as an intermediary.

The definition covers transmission by wire, electronic transfer, courier, internet, or bill payment services. It also applies to any entity with the ability to unilaterally execute or indefinitely prevent a transaction.

The Two License Types

Chapter 560 establishes two license categories:

| License Type | Activities Covered |

|---|---|

| Part II – Payment Instruments & Funds Transmission | Money transmitters, payment instrument sellers |

| Part III – Check Cashing & Foreign Currency Exchange | Check cashers, foreign currency exchangers |

A Part II licensee may also conduct Part III activities without paying additional licensing fees. A Part III licensee, however, may not directly engage in Part II activities — they can only act as an authorized vendor for a licensed Part II entity.

Who Issues It

The OFR (Office of Financial Regulation) supervises money services businesses and authorized vendors under the Financial Services Commission, which holds rulemaking authority. This is a state-level license, distinct from federal FinCEN MSB registration. Most money transmitters operating in Florida will need both.

Who Needs a Florida Money Transmitter License?

The licensing trigger is broad. §560.204 prohibits any person from selling or issuing payment instruments, or acting as a money transmitter for compensation, without a Part II license — unless exempt.

Any entity located in, doing business in, or transmitting money from or into Florida that acts as an intermediary for funds transfers falls under this requirement. That includes:

- Mobile payment apps

- Remittance and wire transfer services

- Virtual currency platforms

- Bill payment facilitators

- Embedded finance businesses that hold or move customer funds

Key Exemptions Under §560.104

§560.104 exempts the following from licensing:

- Federally chartered banks, credit unions, and trust companies

- Edge Act and agreement corporations

- U.S. government agencies and Florida governmental entities

- Authorized vendors of a licensed money transmitter (though they remain subject to Chapter 560 obligations)

Federal registration with FinCEN and CFTC oversight are not exemptions. The OFR assesses Florida's licensing trigger independently of federal status — §560.104 does not list federal registration as a basis for exemption, and §560.125 imposes penalties regardless of whether an entity is federally registered.

If your business model sits in a gray area, get a formal determination before assuming an exemption applies. Misreading the trigger is one of the most common — and costly — mistakes FinTechs make at the Florida licensing stage.

Florida Money Transmitter License Requirements Checklist

Before you touch the OFR's application portal, assemble every document below. Incomplete applications draw deficiency notices, and the OFR typically issues a 30-day cure window — time you can't afford to lose.

Business Entity and Formation Documents

- Legal entity type confirmed: corporation, LLC, LLP, or qualified foreign entity

- Legal name and any fictitious/trade names

- State and date of formation

- Articles of incorporation or operating agreement

- Florida registered agent for service of process

Control Person Disclosures and Background Checks

§560.103(10) defines control persons to include officers (president, CEO, CFO, COO, CLO, compliance officer), directors, and any individual or entity owning or controlling 25% or more of voting securities, partnership interests, or LLC membership interests.

For each control person, prepare:

- Full legal name, SSN or TIN

- Business and residential addresses

- 5-year employment history

- Material litigation history

- Criminal conviction history

- Prior license actions in any jurisdiction

All control persons must submit fingerprints electronically via live-scan through a Florida Department of Law Enforcement-authorized vendor. This requirement does not apply to publicly traded corporations or entities exempt under §560.104(1).

Financial Requirements

Net worth:

- Minimum $100,000 (assets minus liabilities under GAAP)

- +$10,000 per additional Florida location

- Maximum cap of $2,000,000

This must be maintained at all times — not just at application.

Surety bond or security device (§560.209):

- Range: $50,000 to $2,000,000

- Amount determined by anticipated transmission volume, number of locations, and financial condition

- A collateral cash or securities deposit with a federally insured institution may substitute in whole or in part

Audited financial statements must be prepared under U.S. GAAP and cover the most recent fiscal year.

AML Program and Federal Compliance Documents

- Written AML program meeting 31 C.F.R. §1022.210 — internal policies, designated compliance officer, employee training, and independent testing

- FinCEN MSB registration under 31 C.F.R. §1022.380 (initial registration due within 180 days of establishment)

- Sample authorized vendor contracts and payment instrument forms, if applicable

How to Apply: Step-by-Step

All materials are submitted electronically through the OFR's REAL portal at real.flofr.com. There is no paper filing option.

Step 1: Access the Application Form

Download form OFR-560-01 ("Application for Licensure as a Money Services Business," effective 02-2023) from the OFR's Money Transmitters page. Review the portal instructions before starting — PDFs are required for most attachments.

Step 2: Determine License Type and Complete the Application

Select the correct filing:

- Part II — money transmission or payment instrument activities ($375)

- Part III — check cashing or foreign currency exchange ($188)

- Combined Part II + III — single application at the Part II fee of $375

Complete all fields: legal name, FEID, address, IRS identification, organizational history, prior regulatory or criminal actions, and a full list of accounts through which money transmission will be conducted.

Step 3: Assemble Supporting Documents

Gather these before opening the portal — incomplete submissions trigger deficiency notices:

- Audited financial statements

- Written AML program

- Surety bond or proof of collateral deposit

- Fingerprint submission confirmations for all control persons

- Sample vendor contracts or payment instruments (if applicable)

- SEC filings from the preceding year (publicly traded entities only)

- $38 per-location fee documentation for each branch office or authorized vendor location

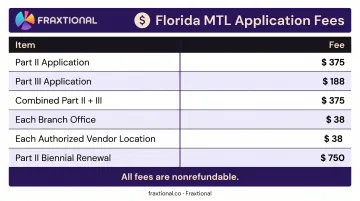

Step 4: Pay Fees and Submit

All fees are nonrefundable:

| Item | Fee |

|---|---|

| Part II application | $375 |

| Part III application | $188 |

| Combined Part II + III | $375 |

| Each branch office | $38 |

| Each authorized vendor location | $38 |

| Part II biennial renewal | $750 |

Submit through the portal and retain your confirmation number. Submission triggers OFR review — Step 5 begins immediately after.

Step 5: Respond to OFR Review and Await Approval

Monitor for deficiency notices and respond within the OFR's prescribed timeframe. The OFR will conduct state and federal criminal background checks on all control persons.

Once approved, the Part II license expires April 30 of the second year following issuance, with subsequent two-year renewal periods. The OFR does not publish average processing timelines — contact the OFR directly for current estimates.

Post-Licensing Compliance Obligations

Getting licensed is not the finish line. Florida law imposes ongoing obligations that, if missed, can result in fines of $1,000 to $10,000 per violation under §560.114, license suspension, or revocation.

Compliance Officer Requirement

A designated compliance officer must be named within 90 days of business establishment, responsible for overseeing all state and federal obligations including AML.

For early-stage fintechs and money transmitters, maintaining a full-time compliance officer is often cost-prohibitive. Fraxtional provides fractional BSA Officer and CCO placements where a named Director can be placed on regulatory filings and directly manages interactions with the OFR, FinCEN, and sponsor banks.

This model is accepted by sponsor banks and regulators, and typically costs far less than a full-time hire, with clients reporting 50–70% savings compared to a full-time executive.

Ongoing Reporting Requirements

- Annual financial audit: Submit to the OFR within 120 days after fiscal year-end

- Quarterly reports: File within 45 days after each quarter ends (§560.118, OFR-560-04)

- Material change notices: Report within 30 days — covers new control persons, address changes, criminal charges, bankruptcy filings, or license actions in other states

Recordkeeping

Maintain all books, accounts, transaction records, and AML documentation for a minimum of 5 years.

Permissible Investments

Under §560.210, licensees must hold permissible investments with an aggregate market value at least equal to the outstanding face amount of all transmitted funds and payment instruments. Eligible asset types include:

Under §560.210, licensees must hold permissible investments with an aggregate market value at least equal to the outstanding face amount of all transmitted funds and payment instruments. Eligible asset types include:

- Cash

- Certificates of deposit (CDs)

- U.S. government securities

- Money market funds

Virtual currency transmitters must hold the equivalent type and amount of virtual currency until each transmission obligation is completed.

Common Mistakes and Misconceptions

Assuming Federal Registration Is Enough

FinCEN MSB registration and Florida's Chapter 560 license are separate, parallel requirements. §560.125 does not carve out an exception for federally registered entities, and the OFR applies its licensing trigger independently. Operating in Florida without a state license while relying solely on FinCEN registration exposes the business to felony-level penalties.

Misreading the "Intermediary" Definition

Many payment technology companies and software platforms assume they don't "receive" money and therefore don't need a license. Florida's definition is broader than that. Any intermediary with the ability to unilaterally execute or prevent a transaction — even momentarily controlling funds — likely triggers the requirement. If your platform touches funds at any point in the transaction flow, treat yourself as in-scope until a qualified legal review confirms otherwise.

Underestimating Post-Licensing Obligations

Applicants often focus on getting the license approved and neglect what comes after. Florida's Chapter 560 imposes ongoing obligations that continue for the life of the license:

- Maintain a functioning AML program with documented policies and procedures

- Designate a qualified compliance officer responsible for day-to-day oversight

- Track permissible investments to satisfy net worth and liquidity requirements

- Complete annual audits and submit them to the OFR on time

Missing any of these can trigger OFR examinations, violation notices, or license revocation. Building the compliance infrastructure before approval — not after — is the more defensible approach.

Frequently Asked Questions

What is the difference between a 220 and 440 money transmitter license in Florida?

"220" and "440" are informal industry shorthand — not official OFR designations. The official terms are Part II (money transmitters and payment instrument sellers) and Part III (check cashers and foreign currency exchangers). A Part II licensee may also conduct Part III activities without additional fees.

Does a Florida money transmitter license cover all locations and online operations in the state?

The license covers the principal place of business and all Florida branch offices and authorized vendor locations, each requiring a $38 per-location fee. Online-only operations transmitting money into or from Florida are also subject to the licensing requirement, regardless of where the company is headquartered.

What net worth is required for a Florida money transmitter license?

The minimum is $100,000 under GAAP, plus $10,000 for each additional Florida location, up to a maximum of $2,000,000. This net worth must be maintained at all times, not just at the time of application.

How long does it take to get a money transmitter license in Florida?

The OFR does not publish a fixed processing timeline — contact them directly for current estimates. Delays most commonly arise from incomplete applications, slow deficiency responses, or background check processing, so a thorough submission matters.

Does a FinCEN MSB registration replace the Florida money transmitter license?

No — FinCEN registration is a separate federal requirement and does not substitute for Florida's state-level license under Chapter 560. Both are required for most money transmitters, and the OFR assesses the licensing trigger independently of federal registration status.

What are the penalties for operating as a money transmitter in Florida without a license?

Under §560.125, unlicensed transmission above $300 is a third-degree felony, rising to a first-degree felony at $100,000 or more in a 12-month period. Civil penalties can reach the greater of $25,000 or the value of funds involved, plus OFR administrative fines up to $1,000 per day under §560.114.