The reality? Most organizations treat bank relationship management as a treasury function—rate comparisons, fee negotiations, and portal access. But the most resilient ones treat it as a compliance and risk management discipline: actively managed, regularly reviewed, and proactively defended.

This article covers five insights drawn from treasury and compliance best practices to help financial professionals and fintech leaders manage bank relationships with the rigor they deserve.

Key Takeaways

- Insight 1: Bank selection is a compliance checkpoint—gaps in your regulatory posture surface here before they become deal-breakers

- Insight 2: Statement format determines your negotiating power. Machine-readable formats like EDI 822 or ISO 20022 camt.086 expose billing errors and enable cost comparisons

- Insight 3: Bank account management is continuous compliance—KYC, signatories, FBAR, and access reviews require ongoing attention, not one-time setup

- Insight 4: API connectivity should solve a business problem first—not chase technology for its own sake

- Insight 5: Automated bank account verification is the most underused fraud defense. Manual processes leave gaps that criminals actively target

Insight #1: Bank Selection Is a Wake-Up Call—and a Compliance Checkpoint

The RFP Process Forces Internal Clarity

The bank selection process is often triggered by dissatisfaction: high fees, poor service, or limited product capability. Conducting an RFP forces organizations to audit their own banking stack, identify redundancies, and clarify what they actually need. That internal clarity is often as valuable as the bank you end up choosing.

According to the 2024 AFP Bank Relationship Management Survey, 98% of organizations prioritize a bank's financial stability when choosing a primary relationship, while 92% value customer service responsiveness. Over 40% of organizations work with 2-5 banks, and 66% cite economies of scale as the primary driver for consolidating or expanding banking relationships.

Core Evaluation Criteria

When evaluating a new bank, treasury and compliance teams should assess:

- Portal usability and security: Multi-factor authentication, role-based access, and efficient account visibility

- ERP/TMS integration: API connectivity, automated reconciliation, and real-time data feeds

- Geographic and product coverage: Multi-currency accounts, international wires, and regional payment rails

- Scalability: Capacity to grow with transaction volume without service degradation

- Industry specialization: Familiarity with fintech, crypto, and money transmission business models

- Fraud controls: Positive pay, dual authorization, and automated account verification

- Fee transparency: Competitive pricing with machine-readable billing data

A bank that saves $500 per month but lacks positive pay can expose you to hundreds of thousands in fraud losses. Price is one input, not the deciding factor.

The Compliance Dimension Often Missing from Standard Frameworks

For fintechs, crypto firms, and money transmitters, sponsor banks want evidence of a mature compliance program before they onboard you. The FFIEC BSA/AML Examination Manual requires banks onboarding Money Services Businesses (MSBs) to:

- Apply Customer Identification Program (CIP) requirements

- Confirm FinCEN registration and state licensing

- Conduct a basic BSA/AML risk assessment

- For higher-risk MSBs, review the BSA/AML program, independent testing results, written procedures, agent management practices, and employee screening

These aren't box-checking exercises — they signal to the bank whether your compliance infrastructure can be trusted. Sponsor banks expect fintechs to demonstrate operational discipline, transparent funds flow with daily reconciliation capabilities, and a tailored compliance structure with clear division of onboarding logic and transaction monitoring responsibilities.

Organizations with fractional compliance leadership—such as a part-time BSA Officer or Chief Compliance Officer through a service like Fraxtional—often move through bank due diligence faster because they arrive with documented, credible compliance infrastructure that sponsor banks trust.

Internal Alignment Is Critical

A bank transition touches more than treasury. Legal, compliance, and finance teams must be looped in before any change begins. Failure to coordinate can result in:

- Missed payments due to stale account information

- Compliance lapses from undocumented account closures

- Tax reporting errors from incomplete FBAR filings

- Operational delays from insufficient signatory documentation

Treat bank selection as a cross-functional initiative, not a treasury-only decision.

Insight #2: Your Statement Format Shapes Your Negotiating Power

Data Access Is the Starting Point

The format your bank delivers fee and transaction data in determines how much you can automate, analyze, and act on. Without machine-readable data, you're stuck with manual PDF reconciliation—time-consuming, error-prone, and impossible to scale once you have more than one or two banking relationships. The format you accept shapes what you can actually do with your data.

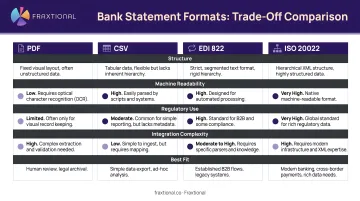

Four Primary Statement Formats and Their Trade-Offs

PDF Statements:

- Official and legally binding

- Manual extraction required for analysis

- Difficult to compare across banks or track trends

- Not suitable for organizations with automation goals

CSV (Comma-Separated Values):

- Free and filterable in Excel or analytics tools

- Inconsistent formatting across banks

- Limited standardization—requires custom mapping

- Better than PDF but not ideal for multi-bank environments

EDI 822 (ANSI X12 Account Analysis):

- Machine-readable electronic version of paper account analysis

- Developed by ASC X12, the Accredited Standards Committee chartered in 1979

- Transmits balances, service charges, and adjustment details

- U.S.-focused standard with limited multi-currency support

- Requires specialized software or TMS integration

BSB / ISO 20022 camt.086:

- International standard supporting multiple currencies, currency translations, and detailed tax information

- Developed by TWIST (v3.1) and adapted into ISO 20022 camt.086

- Uses AFP Global Service Codes (over 900 8-digit codes) for standardized billing

- Analytics-ready and automation-friendly

- Requires enrollment and bank support

- Global standard for multi-bank, multi-currency operations

Organizations with more than two banking relationships or automation goals should prioritize EDI 822 or camt.086 enrollment immediately. Banks cannot backfill historical data, so delayed enrollment means lost visibility into prior periods.

Negotiating Power Through Data Visibility

Pushing for machine-readable formats is a negotiating lever. It gives treasury and finance teams the visibility to:

- Compare costs across banks and identify outliers

- Surface billing errors and duplicate charges

- Benchmark service fees against industry standards

- Identify opportunities to renegotiate pricing or eliminate unused services

For fintechs managing multiple banking partners, this data access often reveals what's actually driving cost increases—whether it's fee creep, billing errors, or services that no longer match your transaction mix. That's the kind of leverage that changes the conversation with your bank.

Insight #3: The Bank Account Lifecycle Is an Ongoing Compliance Obligation

Opening an Account Is Just the Beginning

Every stage of the account lifecycle—from opening to closing—carries regulatory obligations that must be actively managed. For fintechs operating under sponsor bank agreements, gaps in account management can be interpreted as compliance failures that jeopardize the relationship.

Key Lifecycle Stages

Account Opening:

- KYC requirements apply regardless of bank

- 31 CFR 1020.220 requires banks to obtain name, date of birth (for individuals), address (principal place of business for corporations), and identification number (taxpayer ID)

- Standard documents include corporate registration, physical addresses, and tax IDs—prepare these in advance

- On February 13, 2026, FinCEN issued Order FIN-2026-R001, granting relief from the 2016 CDD Rule—covered institutions no longer need to identify and verify beneficial owners at every new account opening, provided they do so initially and update based on risk or factual changes

Account Closing or Modification:

- Always verify with Legal and Tax that the account is no longer needed

- Changes can have organization-wide consequences for cash management, tax reporting, and regulatory filings

- Document the closure decision and retain records

Adding and Removing Signatories:

- Best practice: replace the full signatory card rather than amend it

- Conduct regular signatory reviews (quarterly or semi-annually)

- Maintain up-to-date bank mandates to prevent compliance gaps

Document Management:

- Store legal agreements and banking documents securely—retrieval speed matters during audits

- Region-specific requirements dictate how long you maintain and refresh documents

- Audit trails should be defensible to regulators and sponsor banks

Access Review and Services Audit

Sound document management extends to system access. Review treasury portals and TMS systems regularly to confirm:

- Only authorized personnel retain access

- Services that are unused can be removed

- New services that could add value are identified

FBAR Reporting Obligations

Any U.S. company with a financial interest in or signature authority over foreign accounts exceeding $10,000 in aggregate value must file FinCEN Form 114 annually. The deadline is April 15, with an automatic extension to October 15. Many TMS systems can generate these reports—confirm this capability in advance.

Enforcement Examples

- Metropolitan Commercial Bank (2023): Fined $30 million by the Federal Reserve and NYDFS for CIP violations and deficient third-party risk management related to a prepaid card program that facilitated over $300 million in illicit state unemployment benefits

- Brink's Global Services (2025): Assessed a $37 million FinCEN penalty for failing to register as an MSB, lacking an effective AML program, and failing to conduct KYC on non-customer currency originators

The enforcement pattern is consistent: when account lifecycle controls break down, regulators don't just cite the specific gap—they question the entire compliance program. Treat each lifecycle stage as a standing obligation, not a one-time checklist item.

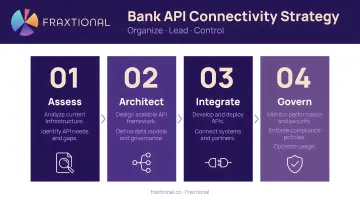

Insight #4: Bank Connectivity and APIs Are Means, Not Ends

Technology Should Solve a Business Problem

The goal of any API or bank connectivity initiative is not the technology itself, but the business function it enables—whether that's real-time balance visibility, automated payment verification, or faster reconciliation.

A 2025 Coalition Greenwich study found that about a quarter of large companies globally are using APIs, and nearly half intend to do so within three years. Deloitte's 2024 Global Corporate Treasury Survey indicates that 49% of respondents prioritize creating a scalable corporate treasury, with a willingness to outsource treasury technology and bank administration.

Four-Stage Strategy Framework

1. Plan:

- Define the specific business problem or use case the API will solve

- Assess costs, risks, and expected benefits

- Identify integration requirements and technical dependencies

2. Organize:

- Identify human and financial resources

- Ensure buy-in from key stakeholders across treasury, technology, and compliance

- Clarify roles and responsibilities

3. Lead:

- Formalize the initiative through a project mandate with clear goals, constraints, and delivery approach

- Assign ownership and accountability

- Set milestones and success criteria

4. Control:

- Measure what value was delivered

- Track KPIs (e.g., reconciliation time, error reduction, payment speed)

- Share results with internal and external stakeholders

- Commit to continuous improvement so the connection stays current with new banking innovations

Fintech-Specific Considerations

That four-stage framework matters even more for fintechs, where bank connectivity is often a core product dependency rather than a treasury optimization tool. Open Banking APIs enable Third Party Providers (TPPs) to query account information, initiate payments, and confirm funds availability. Plaid's open API connects over 6,000 financial apps to financial institutions.

That scope raises the stakes for thoughtful planning. The compliance implications go beyond technical integration:

- Data security: protecting customer account data transmitted via API

- Access controls: managing which third parties can query or initiate transactions

- Vendor risk: ensuring partners meet your bank's operational standards

The 2023 Interagency Guidance on Third-Party Relationships requires banks to evaluate a third party's ability to maintain the confidentiality, availability, and integrity of systems and data.

Insight #5: Automation Is Your Strongest Line of Defense Against Fraud and Broken Bank Relationships

Manual Processes Are the Enemy

Any step in bank account management that depends on human review—especially around supplier or vendor bank account changes—is a point of vulnerability that cybercriminals actively target. The FBI Internet Crime Complaint Center (IC3) received 24,768 Business Email Compromise (BEC) complaints in 2025, resulting in $3.04 billion in reported losses.

How Modern Fraud Works

Criminals use social engineering, deepfakes, and sophisticated impersonation to intercept or redirect payment instructions. FinCEN Alert FIN-2024-Alert004 warns that criminals use Generative AI and deepfakes to impersonate executives and authorize fraudulent transfers, bypassing manual identity verification.

The scale is hard to ignore. According to the 2024 AFP Payments Fraud Survey:

- 80% of organizations were targets of attempted or actual payments fraud in 2023

- ACH credits surpassed wire transfers as the most targeted payment type for BEC fraud, appearing in 47% of BEC incidents

The Layered Control Model

Effective fraud prevention requires multiple overlapping controls—not a single checkpoint. The most underused but highest-impact control is automated bank account ownership verification, which removes human judgment from the change approval process entirely.

Key Automated Controls:

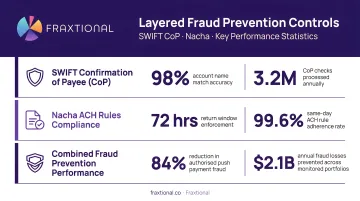

- SWIFT Payment Pre-validation: Verifies beneficiary account details against centrally hosted data before execution — reducing non-STP transactions by more than half

- Confirmation of Payee (CoP): Processes over 2 million name-checks daily in the UK; Pay.UK reports a 59% drop in misdirected payments and 20-40% reduction in financial losses since rollout

- Nacha WEB Debits Rule: Requires validation of first-use consumer account data via ACH prenotification, micro-entries, or commercially available validation services

Enterprise Community Data Sharing

Internal controls have limits. Industry networks like FS-ISAC give financial institutions and fintechs access to shared intelligence on emerging fraud patterns and known compromised accounts — closing blind spots that no internal program can see on its own. Organizations that participate in these networks consistently detect threats earlier than those that rely solely on internal monitoring.

Compliance Implications

For companies operating under BSA/AML frameworks—including fintechs with sponsor bank agreements—fraud control failures are not just financial losses. They are potential regulatory violations. The 2026 National Money Laundering Risk Assessment notes that AML control weaknesses, including insufficient CDD and internal controls, directly facilitate the laundering of fraud proceeds.

That's why ownership matters. Assigning a dedicated compliance officer—whether full-time or fractional through a provider like Fraxtional—to own the bank account change control process and fraud prevention program protects against both financial loss and the regulatory exposure that follows it.

Frequently Asked Questions

What is relationship management in banking?

Relationship management is the proactive, long-term practice of managing a company's banking partnerships—focused on optimizing services, managing costs, meeting compliance obligations, and ensuring the bank relationship supports broader financial and operational goals.

What does RM do in a bank?

A relationship manager (RM) is the primary point of contact between a bank and its clients. A relationship manager (RM) is the primary point of contact between a bank and its clients. They coordinate product access, monitor client needs, facilitate credit or treasury solutions, and advocate for the client internally within the bank.

What does a treasury management relationship manager do?

A treasury management RM helps corporate clients optimize cash management, payment flows, liquidity, and banking product usage—often serving as the liaison between the client's treasury team and the bank's product and operations groups.

What are the 5 C's of banking?

The 5 C's of credit are the core criteria banks use to assess creditworthiness: Character (credit history), Capacity (cash flow and repayment ability), Capital (savings and investments), Collateral (pledged assets), and Conditions (loan purpose and economic environment).

What are the 7 C's of banking?

The 7 C's build on the 5 C's by adding Currency (exchange rate stability) and Coverage (relationship breadth), focusing on risk, repayment ability, and relationship quality from the bank's perspective. This framework is not formally codified by U.S. federal banking regulators, so definitions vary by institution.