Introduction

Most fintech founders discover the same uncomfortable truth early: regulators don't grade on a curve for startups. A 10-person payments company faces the same Bank Secrecy Act obligations as a regional bank. A seed-stage crypto wallet carries the same AML program requirements as an established exchange. The rules apply based on what your product does, not how many people work there.

This is a compliance problem that's genuinely different from anything most founders have dealt with before. Data privacy and SOC 2 are table stakes for any tech company. Fintech adds several more layers on top — all of them active from your first transaction:

- Licensing obligations across states and jurisdictions

- Financial crime prevention programs (AML/BSA)

- Consumer protection rules (UDAAP, Reg E)

- Designated officer requirements (BSA Officer, MLRO, CAMLO)

This guide breaks down which frameworks apply to your business model, what gaps actually cost you in practice, and how to build a defensible program — without hiring a full compliance department first.

Key Takeaways

- Fintech compliance is activity-based — AML, KYC, and licensing obligations trigger based on what your product does, not your funding stage or headcount

- Applicable frameworks depend on your business model, the services you offer, and where your customers are located

- Compliance gaps surface at the worst moments: investor due diligence, sponsor bank reviews, and regulatory examinations

- Building a program doesn't require a full compliance department — but it does require a named, accountable person with genuine expertise

- Fractional compliance leadership gives seed-to-Series B fintechs access to CCO, BSA Officer, MLRO, and CAMLO expertise — no full-time hire required

What Is Startup Compliance — and Why Fintech Is a Special Case

The moment your product touches payments, money transmission, lending, crypto, or banking-as-a-service, you're operating in a regulated industry. That status doesn't phase in gradually — it applies from your first transaction.

Most startups manage compliance through data privacy frameworks, SOC 2 certification, and employment law. Significant obligations, but ones that scale with company size. Fintech doesn't work that way.

Why the Startup Defense Doesn't Work in Fintech

Regulators do not apply a startup exemption. FinCEN requires MSB registration within 180 days of establishment. FINTRAC requires registration before operating. The FCA requires authorization or registration before a firm provides payment services or issues e-money.

The compliance trigger is product activity — not headcount, ARR, or funding round.

Many fintech founders arrive with a tech startup mental model: ship fast, fix compliance later. In fintech, that approach leads to forced wind-downs, regulatory findings, and sponsor bank rejections — often before the product has any real traction.

This guide is written for three audiences:

- Seed-stage fintechs mapping what applies to them before launch

- Series A/B companies preparing for bank partnerships or investor due diligence

- Embedded finance and crypto firms dealing with overlapping regulatory regimes across multiple jurisdictions

The Regulatory Frameworks Every Fintech Startup Must Know

There's no single fintech compliance checklist. The right combination of frameworks depends on your business model, geography, and the type of financial service you offer. Think of it as a decision tree — your obligations branch based on what you do and where you do it.

BSA/AML and KYC Requirements

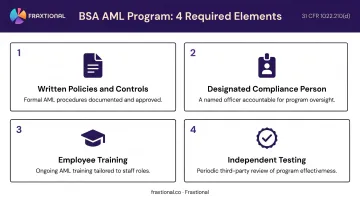

For US-based fintechs operating as money services businesses, the Bank Secrecy Act creates four minimum AML program requirements under 31 CFR 1022.210(d):

- Written policies, procedures, and internal controls tailored to your risk profile

- A designated compliance person responsible for day-to-day AML program management

- Employee training on AML obligations and red flags

- Independent testing of the program's effectiveness

The BSA Officer requirement isn't just a title to assign. FinCEN expects this person to actually perform the role — overseeing SAR filings, managing transaction monitoring, and being accountable when regulators ask questions.

KYC obligations flow directly from AML requirements: Customer Identification Programs (CIP), beneficial ownership verification, and ongoing due diligence for higher-risk customers.

Cross-border equivalents:

- UK: FCA-regulated firms must appoint a qualified MLRO with sufficient seniority, skills, and time. The FCA has stated explicitly that firms cannot rely solely on external consultants for this function

- Canada: FINTRAC requires a designated compliance officer with authority and resources, plus a full compliance program including written policies, risk assessment, training, and a two-year effectiveness review

Money Transmitter Licensing and EMI Authorization

Any startup transmitting, exchanging, or holding funds on behalf of customers needs a license. In the US, that means state-by-state Money Transmitter Licenses (MTLs) — there's no single federal license. State requirements and fees vary significantly; NMLS maintains state-specific checklists and fee schedules and is the authoritative source for current requirements.

In the UK and EU, firms need FCA authorization or registration as an Electronic Money Institution or payment institution before operating.

Operating without required licenses isn't a gray area. It can mean forced wind-down, civil money penalties, and permanent reputational damage with sponsor banks.

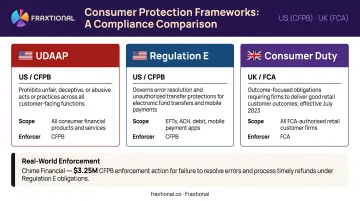

Consumer Protection Regulations

Consumer protection obligations affect product design, marketing copy, and customer service workflows — not just legal disclosures.

| Framework | Jurisdiction | What It Covers |

|---|---|---|

| UDAAP | US (CFPB-enforced) | Unfair, deceptive, or abusive acts or practices in any customer-facing function |

| Regulation E | US (CFPB) | Error resolution and unauthorized transfer protections for EFTs, prepaid, P2P, mobile payments |

| Consumer Duty | UK (FCA, effective July 2023) | Outcome-focused obligations for firms serving retail customers |

The CFPB's 2024 enforcement action against Chime illustrates just how broadly these obligations reach: a $3.25M civil penalty plus at least $1.3M in redress for failing to provide timely refunds after account closure. The violation was operational, not AML-related — a reminder that consumer protection touches every team, not just legal.

Data Privacy: GDPR, UK GDPR, and PIPEDA

Privacy obligations follow your customers, not your incorporation address. A US-incorporated fintech serving EU residents is subject to GDPR. One serving UK residents faces UK GDPR under the Data Protection Act 2018. Canadian operations or customers trigger PIPEDA.

Key obligations across these frameworks:

- Lawful basis for processing personal data

- Privacy notices and consent management

- Data subject rights (access, deletion, portability)

- 72-hour breach notification to supervisory authorities under GDPR Article 33

- Cross-border data transfer restrictions

PCI DSS for Payment-Handling Startups

PCI DSS applies to any fintech that stores, processes, or transmits cardholder data — including companies using third-party processors like Stripe or Adyen.

Using a compliant processor reduces your compliance scope (potentially qualifying you for SAQ A), but it doesn't eliminate your obligation to attest to compliance annually and validate your vendor controls. PCI DSS v4.0.1 is the current active standard as of 2025.

The Real Cost of Compliance Gaps

Compliance gaps don't sit quietly in the background. They surface at the exact moments that matter most.

Three High-Stakes Moments

Investor due diligence. Gaps delay closings, create conditions on term sheets, and in some cases kill rounds entirely. Investors conducting proper diligence on a fintech will ask for AML program documentation, compliance officer credentials, licensing status, and regulatory correspondence. Missing any of these creates a negotiating problem.

Sponsor bank reviews. Banks evaluating fintech partnerships review legal and regulatory compliance, risk management controls, information security, and operational resilience (the framework federal banking agencies explicitly recommend). A fintech without a demonstrable AML program, a named BSA Officer, and consumer protection controls typically doesn't make it past initial review.

Regulatory examinations and enforcement. The enforcement record here is real:

- FinCEN assessed $29,280,829.20 against Bittrex in 2022 for BSA violations

- The FCA fined Starling Bank £28,959,426 in 2024 for financial crime systems and controls failures

These aren't anomalies. LexisNexis Risk Solutions reported in 2023 that 98% of financial institutions saw financial crime compliance costs increase. The downside of an enforcement action extends beyond the penalty itself to legal defense, remediation, deal delays, and lost banking relationships.

The Founder Liability Dimension

One risk fintech founders consistently underestimate: in regulated financial services, certain compliance failures, particularly AML violations, can result in personal liability for designated compliance officers and executives, not just corporate penalties.

Holding a BSA Officer or MLRO title without the capacity and expertise to perform the role creates personal exposure, including civil money penalties and potential disqualification from future regulated roles.

How to Build a Compliance Program From the Ground Up

The goal isn't bank-level infrastructure on day one. It's implementing the controls that regulators, partners, and investors require at your current stage — while avoiding decisions that become expensive to unwind later.

Step 1: Map Your Regulatory Obligations

Before launch, analyze three things:

- Business model: What financial activity does your product facilitate?

- Geography: Where are you incorporated, and where do your customers reside?

- Distribution: Are you direct-to-consumer, B2B, or embedded?

This mapping determines which regulators have authority over your activities. Doing it post-launch means you're responding to regulatory questions rather than building a defensible position.

Step 2: Conduct a Risk Assessment and Gap Analysis

A compliance risk assessment identifies inherent risks in your product (money laundering exposure, consumer harm potential, data breach risk), evaluates current controls against those risks, and ranks gaps by likelihood and impact.

This document serves a practical purpose beyond internal planning. A well-structured risk assessment creates documented evidence that you identified risks and addressed them deliberately — that distinction matters in enforcement scenarios and investor reviews.

Good output from this exercise includes a risk prioritization matrix and a remediation roadmap that separates high-urgency gaps from lower-priority items. Fraxtional structures these deliverables to hold up in board reviews, bank evaluations, and third-party audits.

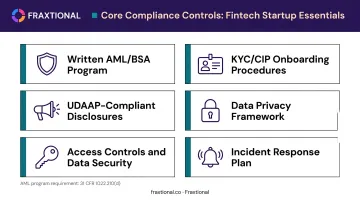

Step 3: Implement Core Controls and Policies

Every fintech startup needs these operational controls:

- Written AML/BSA program (for US MSBs, following the four elements under 31 CFR 1022.210(d))

- KYC/onboarding procedures with CIP and beneficial ownership verification

- UDAAP-compliant product disclosures and marketing review process

- Data privacy framework including consent management and breach response

- Access controls and data security measures

- Incident response plan with documented notification timelines

Policies that exist as documents but aren't reflected in how the business actually runs don't satisfy regulators or sponsor banks.

Step 4: Establish Documentation and Audit Readiness

Compliance documentation is what makes your program real to an auditor, investor, or bank partner. This means:

- Policy documents with version control and employee acknowledgment records

- Training completion logs

- Vendor due diligence files

- SAR/CTR filing records (where applicable)

- Evidence of control testing and independent review

- Regulatory correspondence, organized and accessible

A Series A fintech that can't produce these documents on short notice will lose time, and sometimes lose deals, while scrambling to assemble them under pressure.

Step 5: Build a Regulatory Monitoring Process

Regulations change, new guidance gets issued, and enforcement priorities shift. Without a monitoring process, compliance programs go stale.

Practical approaches for lean teams:

- Subscribe to FinCEN, FCA, FINTRAC, and relevant state regulator alerts

- Build quarterly compliance reviews into the operating calendar

- Work with advisors who actively track regulatory developments in your specific vertical

The Compliance Leadership Question: Who Owns Compliance at Your Startup?

Fintech compliance isn't just about having the right policies. Regulators and sponsor banks expect a designated, accountable individual with relevant expertise. A BSA Officer must be able to perform the role — filing SARs, overseeing transaction monitoring, interacting with regulators — not just hold a title.

Leadership Options by Stage

Pre-seed/seed: Founders often absorb compliance responsibilities initially, with external counsel on hand for specific regulatory questions. This works for a limited time, but it creates increasing risk as the product scales and regulated activity grows.

Series A: Bank partnerships are typically in play, and investors are asking substantive compliance questions. A full-time CCO is often cost-prohibitive at this stage. Going without expert coverage is no longer low-risk.

Series B and beyond: A dedicated compliance function is expected by regulators, banking partners, and institutional investors. The question shifts from "do we need this?" to "what does the right structure look like?"

The Fractional Compliance Model

For seed-to-Series B fintechs, fractional compliance leadership solves a real problem: getting named, regulator-recognized leadership without the cost and commitment of a full-time executive hire. Firms like Fraxtional provide CCO, BSA Officer, CAMLO, and MLRO services on a fractional basis — giving startups named compliance leadership that regulators and sponsor banks recognize, without the cost and commitment of a full-time executive hire.

- Proven experience in your specific model — payments, crypto, lending, or embedded finance

- Cross-border fluency if you operate across the US, UK, and Canada

- Willingness to serve as a named officer with regulators and sponsor banks

- Director-led delivery, not senior-to-junior handoff after the first meeting

Fraxtional works with clients across the US, UK, Canada, and EU. The team holds CAMS and Certified Bitcoin Professional credentials, and has been recognized as a Top 10 Best Fractional Compliance Firm in the US for 2024 and 2025.

Frequently Asked Questions

What compliance requirements do fintech startups need to meet from day one?

Fintechs handling money transmission, payments, or customer financial data typically face AML/KYC obligations, licensing requirements, and consumer protection rules from their first transaction. The compliance trigger is the activity itself, not company size or funding stage. Your specific business model and geography determine which rules apply.

When does a fintech startup need a BSA Officer or MLRO?

US money services businesses are required under FinCEN rules to designate a person responsible for day-to-day AML compliance — this is the BSA Officer function under 31 CFR 1022.210(d)(2). UK-regulated firms must appoint an MLRO. Both requirements apply based on regulated activity, not company size.

Can a startup be compliant without a full-time Chief Compliance Officer?

Yes. Many early-stage fintech companies use fractional compliance leadership to fulfill CCO, BSA Officer, and MLRO obligations. The role must carry genuine expertise and clear accountability — the person needs to actually perform the function, not just hold the title.

What do investors and sponsor banks check during compliance due diligence?

Investors and banks typically review the existence and adequacy of an AML program, evidence of KYC procedures, compliance officer credentials, regulatory licenses, policy documentation, and any prior regulatory findings or enforcement history. Having organized, accessible documentation shortens review timelines significantly.

How does multi-jurisdiction compliance work for fintechs operating in the US, UK, and Canada?

Each jurisdiction has its own regulator and registration requirements: FinCEN and state MTLs in the US, FCA authorization in the UK, FINTRAC registration in Canada. A fintech operating across all three must satisfy all applicable regimes simultaneously.

How much does compliance typically cost for an early-stage fintech startup?

Costs vary based on business model complexity, geographic scope, transaction volume, and staffing approach (in-house, consultant, or fractional). There's no single number — model the drivers against your specific situation, then weigh that cost against the penalties that come with AML failures.