Introduction

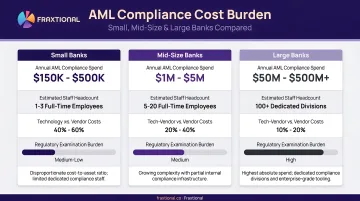

U.S. financial institutions spent an estimated $59 billion on BSA/AML compliance in 2023, and mid-size banks face a uniquely difficult challenge: the same regulatory requirements as large institutions, but with far fewer resources to absorb the cost. LexisNexis documented a 13.6% year-over-year increase in compliance spending from 2021 to 2022, and 99% of institutions report that costs continue to rise.

That pressure lands hardest on mid-size banks, typically those with $1 billion to $10 billion in assets. Unlike large institutions with dedicated compliance departments, these banks must absorb significant program costs without the same economies of scale.

What those costs actually look like depends on program sophistication, transaction volumes, regulatory risk profile, and whether the bank builds in-house, buys software, or outsources leadership functions. This guide covers realistic cost ranges, the three major cost components (people, processes, technology), the factors that drive costs up or down, and practical budgeting guidance for 2026.

Key Takeaways

- Total AML compliance costs for mid-size banks range from $500,000 to over $3 million annually

- Personnel costs (BSA officers, compliance analysts, and leadership) account for 50–60% of total spend

- Technology platforms (transaction monitoring, KYC, case management) run $100,000 to $500,000+ annually

- Fractional compliance leadership models can reduce executive-level costs by 50-70% versus full-time hires

- Underinvestment creates long-term risk: remediation costs typically run 2x-3x the original regulatory penalty

How Much Does an AML Compliance System Cost for a Mid-Size Bank?

Mid-size banks face the same regulatory requirements as large banks under BSA/AML, FinCEN, and FFIEC guidance, but with far fewer resources. Banks with $1 billion to $10 billion in assets report compliance costs of approximately 2.9% of non-interest expenses, while smaller institutions below $100 million face costs as high as 8.7% of non-interest expenses.

This disproportionate burden is statistically significant. Smaller banks attribute 11% to 15.5% of their personnel expenses to regulatory compliance, compared to 5.6% to 9.6% for larger institutions. Mid-size banks dedicate approximately 50% of all risk management spending to BSA/AML compliance alone.

When cost is misunderstood, the outcomes land at two extremes: underbudgeting that invites regulatory sanctions, or overbuilding with redundant vendors and excess staffing that adds cost without reducing risk. The tiers below define realistic spending ranges based on asset size, product complexity, and regulatory exposure.

Tier 1: Entry-Level AML Compliance Program ($300K–$700K/year)

What's typically included:

- Basic transaction monitoring platform

- Manual KYC/sanctions screening tool

- One or two compliance analysts

- Part-time BSA officer function

Best for: Mid-size banks with less than $3 billion in assets, limited product complexity, and a consistent customer base. Note that if alert volumes grow and manual review becomes a bottleneck, this tier carries elevated regulatory risk.

Tier 2: Mid-Range AML Compliance Program ($700K–$2M/year)

Best for: Most mid-size banks in the $3 billion to $8 billion asset range with diversified products — commercial banking, payments, and wire transfers. Transaction monitoring must span multiple business lines, and alert volumes require a structured review workflow.

What's typically included:

- Robust transaction monitoring platform with configurable rules

- Integrated KYC/CDD tools

- Dedicated BSA officer plus 2–4 analysts

- Independent testing/audit function

- Basic case management software

Tier 3: Advanced/Full-Scale AML Compliance Program ($2M–$5M+/year)

What's typically included:

- Enterprise-grade AI-powered transaction monitoring

- Automated sanctions and PEP screening

- End-to-end case management

- Full BSA/AML team (BSA Officer, compliance analysts, data team)

- Ongoing independent audits

- Cross-border or high-risk product coverage

Best for: Mid-size banks approaching $10 billion in assets, those with high-risk customer segments (money services businesses, crypto-related banking), international correspondent banking, or banks under consent order or heightened regulatory scrutiny.

Key Factors That Drive AML Compliance Costs for Mid-Size Banks

AML compliance pricing for mid-size banks is not a fixed formula—it is shaped by the intersection of regulatory exposure, operational complexity, and the bank's strategic choices about technology and talent.

Asset Size and Transaction Volume

Transaction volume directly drives monitoring platform licensing costs and analyst workload. A bank processing 500,000 transactions monthly has meaningfully different monitoring requirements and costs than one processing 5 million.

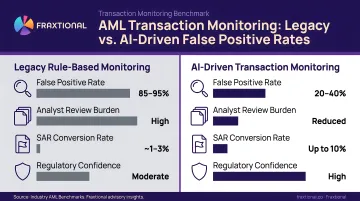

A mid-market bank with approximately $5 billion in assets may generate approximately 50,000 alerts per year. Traditional AML systems generate 90%-98% false positive alerts, creating massive operational waste. Each investigation costs $25-$50 per alert at mid-size institutions, meaning alert processing alone can consume hundreds of thousands of dollars annually.

Customer Risk Profile and Product Mix

Customer mix and product breadth both push compliance costs upward. Banks serving higher-risk segments face Enhanced Due Diligence requirements and higher alert volumes, while product diversity multiplies the typologies needing monitoring coverage. Key risk drivers include:

- Money services businesses and cash-intensive commercial accounts

- International wire transfer capabilities

- Commercial lending alongside retail deposits

- Payments products with cross-border exposure

Technology Choice: Legacy vs. Modern Platform

Banks running legacy on-premise transaction monitoring systems face high maintenance costs, expensive upgrades, and slower rule tuning. Cloud-based, API-first platforms typically carry higher upfront costs but deliver significantly lower total cost of ownership.

The critical difference is false positive reduction. Legacy rule-based systems miss 30-45% of suspicious activity, while AI-driven systems can reduce false positives by 50-70% within 12 months. For a bank processing 50,000 alerts annually, that reduction can eliminate the equivalent of one or two full-time analyst positions.

Compliance Staffing Model

The cost difference between a fully in-house team (BSA officer, analysts, internal audit) versus a hybrid model using fractional compliance leadership is substantial.

BSA Officer and compliance leadership functions are often the highest single cost line items. Mid-size banks may not require—or be able to sustain—full-time executive-level hires year-round. Fractional BSA Officer models deliver experienced director-level oversight at 50-70% lower cost than full-time executive hires, without sacrificing regulatory credibility.

Regulatory History and Examination Frequency

Banks with prior examination findings, MRAs (Matters Requiring Attention), or consent orders face significantly elevated costs due to enhanced monitoring requirements, more frequent independent testing, and potential for external monitorship.

Consider CommunityBank of Texas: $8 million in civil money penalties for willful failure to maintain an effective AML program. The penalty represented only direct costs—remediation programs typically run 2x-3x the penalty amount, meaning total remediation likely exceeded $16-$24 million.

Breaking Down the Full AML Compliance Cost

AML compliance costs run deeper than a software license. Three interconnected cost layers drive total spend, and mid-size banks need to plan for all of them.

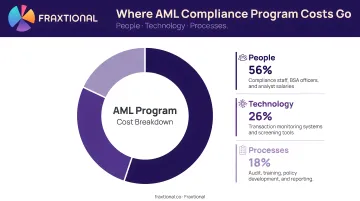

People (Largest Cost Category)

Typical staffing requirements for a mid-size bank AML program:

- BSA/AML Officer (or equivalent)

- Compliance analysts for transaction monitoring review and SAR filing

- CDD/KYC function

- Periodic independent testing

Current salary benchmarks:

- BSA Officer: $126,215 average

- AML Compliance Analyst: $96,903 average

- Chief Compliance Officer: $193,853 average

Personnel costs often represent 50-60% of total AML compliance spend. Labor and training account for approximately 57% of total financial crime compliance spending, with compliance representing approximately 10% of a financial institution's total personnel expenses.

Fractional BSA Officer models offer a practical alternative. Banks working with providers like Fraxtional access BSA Officer and CCO-level expertise without the $150,000-$200,000+ annual salary commitment, while maintaining the regulatory credibility these functions require.

Technology (Second Largest Category)

The technology stack a mid-size bank typically needs:

- Transaction monitoring software

- KYC/CDD and sanctions screening platform

- Case management tool

- Customer risk scoring/CIF system

Technology costs alone can run $250,000 to $1 million+ annually. Acquiring these as separate point solutions typically costs more than a single integrated platform.

Cost structure breakdown:

- One-time costs: Implementation/integration ($50,000-$200,000 depending on core banking system complexity)

- Recurring costs: Annual licensing/subscription fees

- Periodic costs: Upgrade and re-validation expenses

Mid-market institutions (100-1,000 employees) spend $3.2 million to $7.8 million per year on transaction monitoring alone, which represents 25-35% of total AML budgets.

Processes, Audits, and Ongoing Obligations (Often Underestimated)

Recurring process costs frequently underbudgeted:

- Annual BSA/AML risk assessment

- Independent program testing/audit ($30,000-$80,000 per engagement)

- SAR filing and CTR reporting workflows

- Staff training and CAMS certification maintenance

- Regulatory examination preparation

CAMS certification costs per staff member:

- Initial certification: $2,300-$6,000

- Annual recertification: $250

- Continuing education: $300-$800 annually

These ongoing process costs can represent 15-25% of total AML spend for mid-size banks.

Lean vs. Robust AML Program — What's the Difference?

The cost difference between a lean and robust AML compliance program reflects meaningfully different levels of regulatory risk, detection effectiveness, and operational resilience. The table below breaks down how the two approaches compare across the dimensions that matter most.

| Dimension | Lean Program | Robust Program |

|---|---|---|

| Detection capability | Rules-based monitoring with limited tuning and 95%+ false positive rates | Risk-based, configurable models with 60-75% false positive rates and better coverage of complex typologies |

| Staffing | Minimal headcount with staff wearing multiple hats | Dedicated roles with clear ownership of monitoring, investigations, SAR filing, and independent oversight |

| Regulatory resilience | May pass routine exams but vulnerable during heightened scrutiny | Documented governance, independent testing, and audit trails that hold up under examination pressure |

| Long-term cost | Lower annual spend but compounding risk—remediation after enforcement can cost 2x-3x what proactive investment would have cost | Higher predictable annual spend but lower tail risk of enforcement and remediation |

The "long-term cost" row is where lean programs most often break down in practice. Metropolitan Commercial Bank faced a $15 million penalty for AML program deficiencies — and the remediation that followed (system overhauls, staffing additions, lookback reviews, legal fees) ran an estimated $30-$45 million on top of the penalty itself. For mid-size banks weighing upfront program costs, that math is hard to ignore.

How to Budget Smarter for AML Compliance in 2026

Smart AML budgeting means allocating resources proportionate to your bank's actual risk profile, regulatory obligations, and growth trajectory — not simply maximizing or minimizing spend.

Key budgeting considerations for 2026:

- Run a current-state BSA/AML risk assessment to identify gaps before selecting technology or staffing solutions

- Evaluate total cost of ownership across a 3-year horizon, not just Year 1 licensing fees

- Benchmark your compliance spend as a percentage of non-interest expenses against the 2.9% figure reported for $1B–$10B banks

- Determine whether director-level compliance functions require full-time headcount or whether a fractional engagement model — such as those offered by Fraxtional — provides equivalent regulatory credibility at lower cost

What most mid-size banks get wrong:

- Focusing only on software costs while underestimating people costs

- Choosing the cheapest transaction monitoring platform without evaluating false positive rates (which drive analyst headcount)

- Not budgeting for independent testing and audit as a recurring line item

- Waiting for a regulatory finding to invest in program improvements rather than building proactively

Frequently Asked Questions

How much do AML compliance systems cost for mid-size banks?

Total annual AML compliance costs for mid-size banks typically range from $500,000 to over $3 million depending on asset size, risk profile, and program sophistication. Technology represents roughly 30–40% and personnel represents 50–60% of that total.

What are examples of AML compliance costs for mid-size banks?

Common cost line items include:

- Transaction monitoring platform: $100,000–$500,000/year

- BSA Officer salary: $120,000–$200,000+

- Compliance analysts: 2–4 FTEs at $90,000–$100,000 each

- Independent audit/testing: $30,000–$80,000 per engagement

- SAR filing and CTR reporting workflow costs (variable)

What AML compliance software do mid-size banks use?

Mid-size banks typically use platforms covering transaction monitoring, sanctions/PEP screening, KYC/CDD case management, and customer risk scoring. Common approaches include integrated suites (NICE Actimize, Verafin, Nasdaq Surveillance) or modular API-first platforms — the right fit depends on core banking system compatibility and transaction volume.

What is the biggest cost driver in an AML compliance program for a mid-size bank?

Personnel is consistently the largest cost driver, particularly the BSA Officer and compliance analyst functions. Compliance staffing represents approximately 10% of total personnel expenses at financial institutions. Fractional BSA Officer arrangements typically cut this expense by 40–60% compared to a full-time hire.

Can mid-size banks reduce AML compliance costs without increasing regulatory risk?

Yes. Cost optimization is achievable through automation to reduce false positives and analyst workload, consolidating point-solution vendors into integrated platforms, and using fractional compliance leadership for executive functions — none of which compromise regulatory defensibility.

What happens if a mid-size bank underinvests in AML compliance?

Underinvestment can result in regulatory MRAs, consent orders, or civil money penalties. Sterling Bank and Trust faced a $6 million penalty for BSA/AML violations, plus reputational damage and remediation costs that typically far exceed what a properly funded program would have cost.