The principle driving these actions is activity-based regulation. State regulators don't care whether your company calls itself a fintech, a marketplace, or a software platform. What matters is what your product actually does — moving money, making loans, brokering credit, servicing debt. That activity triggers licensing requirements regardless of how you've branded your business model.

This guide walks through practical, sequenced licensing tips for fintech companies — from pre-launch activity mapping to bank partnership structuring to staying compliant after the license arrives.

Key Takeaways

- Licensing is triggered by activity, not technology — calling yourself a fintech doesn't create an exemption

- Most fintechs need licenses across multiple states and potentially multiple license types

- A bank partnership reduces direct licensing burden but doesn't eliminate compliance obligations

- State-by-state variation in triggers, thresholds, and timelines requires a full 50-state analysis

- Renewals, amendments, and reporting carry the same legal weight as the initial application

Map Your Activities to the Right Licenses Before You Launch

Before filing anything, build a product-flow matrix. The same app can trigger multiple license types simultaneously, and discovering this post-launch is expensive.

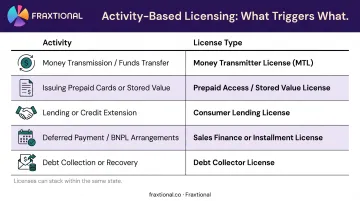

Common License Types Fintechs Encounter

| Activity | License Type |

|---|---|

| Receiving and transmitting funds or issuing stored value | Money Transmitter License (MTL) |

| Making consumer or commercial loans above rate/amount thresholds | Money Lender License |

| Arranging loans on behalf of another lender | Broker License |

| Collecting scheduled payments on loans you service | Loan Servicer License/Registration |

| Collecting debt owned by a third party | Debt Collection License |

These licenses stack. A lending platform might need a broker license, a servicer registration, and a debt collector license — all in the same state.

Licensing for Payments-Focused Fintechs

Payment companies generally need a Money Transmitter License in most states when they receive money for transmission or issue stored value. At the federal level, FinCEN requires registration as a Money Services Business under the Bank Secrecy Act — MSBs typically register within 180 days of establishing operations and renew every two years. This federal registration is separate from state MTLs and does not replace them.

MTL applications must typically be submitted through the Nationwide Multistate Licensing System (NMLS), which serves as the workflow infrastructure for participating state nondepository licensing. Approval timelines vary significantly — from a few weeks in some states to 12 months or more in others. Build that range into your go-to-market roadmap from day one.

Licensing for Lending and Credit-Focused Fintechs

Consumer and commercial lenders face a more complex matrix. Several states tie licensing obligations to specific loan amount and APR thresholds:

- Massachusetts: Small-loan license applies to loans of $6,000 or less where interest and expenses exceed 12% per annum; you'll also need separate licenses for third-party debt collection and loan servicer registration

- New Hampshire: "Small loan" means a loan of $10,000 or less with an APR of 10% or more for personal, family, or household use

- Nevada: The definition of "internet consumer lender" covers anyone who makes, solicits, brokers, arranges, or facilitates consumer loans online — meaning loan marketplaces and lead generators can trigger licensing before a single loan is funded

True lender risk compounds this further. Maine and Illinois both apply a totality-of-circumstances test to determine whether the fintech — not the bank — is the actual lender. Under Maine's Section 2-702, a company acting as agent or service provider for an exempt entity may still be treated as the lender if it holds the predominant economic interest. Illinois's Predatory Loan Prevention Act applies similar analysis based on program control, right of first refusal, and economic benefit.

Courts have followed suit. In In re Rent-Rite Super Kegs West Ltd., a court allowed true-lender allegations involving a bank-originated loan to proceed, looking past the formal structure to economic substance.

Navigate State-by-State Licensing Variations

There is no uniform national fintech license. Each state controls its own triggers, fee structures, net worth requirements, surety bond amounts, and examination processes. A 50-state analysis is not optional — it's the starting point.

States With Broad or Complex Requirements

Several states are worth flagging early in your planning:

- Nevada requires a license even for companies that merely help consumers find a bank loan — the solicitation trigger is unusually broad

- Maine and Illinois apply totality-of-circumstances tests that can reclassify a fintech as the de facto lender regardless of how the bank partnership is structured

- New York layers a BitLicense requirement on top of standard MTL requirements for any company receiving, transmitting, or exchanging virtual currency — one of the most demanding crypto licensing regimes in the country

- Pennsylvania regulators have explicitly reaffirmed that labeling a business as "software" or "infrastructure" does not exempt it from financial services licensing

Licensing Timelines as an Operational Risk

Most states require regulatory approval before a company may begin operating. A fintech that doesn't account for multi-month application timelines in its launch roadmap faces a hard choice: delay go-live or operate at legal risk.

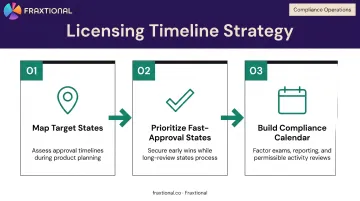

Build your timeline strategy around these practical steps:

- Map target states against realistic approval timelines during product planning, not after

- Prioritize faster-approval states first to generate early licensing wins while longer-review states are in process

- Factor examination cycles, annual reporting deadlines, and permissible activities reviews into your compliance calendar from day one

As of February 2026, 31 states had enacted the CSBS Money Transmission Modernization Act in whole or in part, which is gradually standardizing some requirements — but the licensing landscape remains state-by-state for now.

Once licensed, fintechs enter ongoing supervisory relationships with each state. Examination frequency, annual reports, and permissible activities standards differ enough that what's compliant in one state may require additional steps in another.

Use the Bank Partnership Model to Reduce Your Licensing Burden

A bank partnership allows a fintech to offer regulated financial products — lending, payments, card issuance — through a chartered bank's existing authorizations. The bank conducts the licensed activity; the fintech manages technology, distribution, and the customer experience. Chartered banks can lend nationally without state-by-state lending licenses and can export interest rates from their home state under Marquette National Bank v. First of Omaha and 12 U.S.C. § 85.

What the Model Solves — and What It Doesn't

The partnership reduces direct licensing burden, but it creates a different set of obligations. As a bank service provider, the fintech falls under the Bank Service Company Act, which gives federal banking agencies oversight authority over third-party services performed for insured depository institutions. The FDIC, OCC, and Federal Reserve issued final interagency third-party risk guidance in 2023 requiring banks to manage fintech partners as supervised vendors.

The fintech must demonstrate compliance with BSA/AML, UDAAP, Reg E, and fair lending requirements — because the bank's own examiners will review the fintech's program directly.

That's where preparation matters. Fraxtional works with fintechs to build their compliance stack before bank meetings: reviewing AML frameworks, drafting policy documentation, and closing the gaps that most commonly stall due diligence.

Payment network access creates a parallel constraint. Only network member banks can issue Visa or Mastercard products or settle ACH transactions on behalf of fintechs — third parties route entries through an Originating Depository Financial Institution. Companies that enter card issuance or payment processing without a bank sponsor face structural routing limitations that no compliance workaround can resolve.

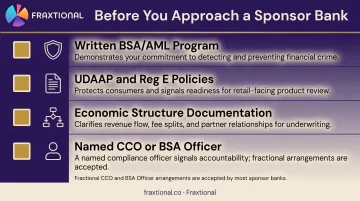

What to Prepare Before Approaching a Sponsor Bank

- Written BSA/AML program with internal controls, named compliance officer, training, and independent review (required under 31 CFR Part 1022)

- UDAAP and Reg E policies aligned to the product's consumer-facing features

- Clear documentation of the economic structure — particularly for lending programs subject to true-lender scrutiny

- A named CCO or BSA Officer (fractional arrangements are widely accepted by sponsor banks)

Managing Ongoing Compliance Obligations After Licensing

Getting a license is the start of a regulatory relationship, not the finish.

License Renewals and Material Changes

Most states require annual or biennial renewals involving fee payments, updated financials, and certifications of continued compliance. Missing a deadline creates the same legal exposure as operating without a license.

Many states also require notification of material business changes — new products, ownership changes, significant adverse legal events — within tight windows. Some states require notice within 10 to 30 days. Fintechs expanding their product line or geographic footprint need to evaluate whether those changes trigger new licensing requirements in existing states or require licenses in new jurisdictions.

Examination Readiness

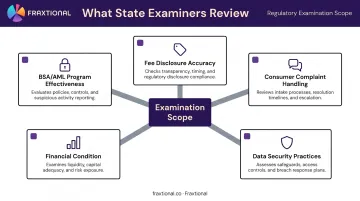

Licensed fintechs are subject to periodic examinations covering:

- BSA/AML program effectiveness

- Consumer complaint handling and resolution

- Fee disclosure accuracy

- Data security practices

- Financial condition

Examination readiness isn't a sprint before an audit — it's a standing operational posture. That means keeping policies current, maintaining a documented procedures library, training staff regularly, and running internal audits on a defined schedule.

When to Bring in Fractional Compliance Leadership

Sustaining that posture across multiple licensed states — while managing renewals, material change notifications, and reporting deadlines — is more than most early-stage teams can absorb alone. For startups and growth-stage fintechs without a dedicated compliance function, this is where internal capacity typically runs out.

Fractional compliance leadership addresses that gap directly. A fractional CCO or BSA Officer — through a firm like Fraxtional — takes ownership of ongoing compliance operations without the cost or commitment of a full-time executive hire. As the business scales into new jurisdictions or product lines, the engagement adjusts accordingly.

Common State Licensing Mistakes Fintechs Make

Assuming a Platform Model Creates an Exemption

The most common pre-launch mistake is concluding that operating through technology infrastructure exempts the company from licensing. The SoLo Funds consent order is instructive: despite a platform model, California's DFPI found the company brokered consumer loans without the required license. Pennsylvania regulators have made the same point explicitly.

Consequences include cease-and-desist orders, civil money penalties, and required restitution to affected customers.

Doing a Partial State Analysis

Many fintechs obtain an MTL in their home state and a few large markets, then discover later they've been operating unlicensed in states with broad jurisdictional reach. Some states treat online solicitation of residents as sufficient to trigger licensing — meaning geographic targeting in digital advertising can inadvertently create unlicensed exposure across multiple jurisdictions.

Letting Post-Licensing Maintenance Slip

Companies that obtain licenses often fail to track renewal deadlines, respond to regulator inquiries, or notify regulators of business changes within required timeframes. This is especially common during rapid growth, when product features evolve faster than compliance monitoring keeps pace. License maintenance requires the same operational discipline as the initial application process.

Frequently Asked Questions

What are the regulations for fintech companies in the U.S.?

Fintechs operate under a layered framework of federal law — including the Bank Secrecy Act, Regulation Z, Regulation B, and Regulation E — plus state-level licensing regimes that vary by activity type. Payments, lending, brokering, and debt servicing each carry distinct requirements across all 50 states, and the CFPB has supervisory authority over larger consumer financial market participants.

Do fintech companies need a money transmitter license in every state?

Most states require an MTL to receive and transmit funds or issue stored value, though some have exemptions or different thresholds. There is no single federal money transmitter license for non-bank entities — FinCEN registration as an MSB is required federally, but it is separate from and does not replace state MTLs. A state-by-state analysis is required.

Can a bank partnership replace state licensing requirements?

A bank partnership can reduce a fintech's direct licensing burden, since chartered banks operate under existing federal or state authorizations. The fintech still bears compliance obligations as a bank service provider — subject to the bank's compliance program expectations and its primary regulator's oversight.

How long does it take to get a money transmitter license?

Approval timelines vary significantly by state — ranging from a few weeks in some jurisdictions to 12 months or more in others. Build licensing timelines into your product launch roadmap well in advance of planned go-live dates, and file in multiple states concurrently where possible.

What happens if a fintech operates without the required state license?

Operating without a required license can result in cease-and-desist orders, civil money penalties, consumer restitution requirements, and lasting reputational damage. State regulators have pursued enforcement actions against unlicensed fintechs consistently — ignorance of licensing requirements is not a recognized defense.

What is the NMLS and do all fintech companies need to use it?

The Nationwide Multistate Licensing System (NMLS) is the centralized platform for submitting and managing license applications across participating states. Most money transmitter and consumer lender applications run through NMLS, making it the practical starting point — though each state still controls its own substantive requirements.