Introduction

Crypto compliance is no longer a concern limited to large exchanges. Regulators across the US, UK, Canada, and EU are actively pursuing non-compliant firms of every size — and many founders and compliance leads are struggling to keep pace with enforcement that moves faster than their programs do.

The CFTC reported over $17.1 billion in FY2024 monetary relief, driven largely by digital asset cases including FTX/Alameda and Binance-related enforcement. In Canada, FINTRAC fined Binance $6 million in May 2024 for failing to register as a foreign MSB and failing to report large virtual currency transactions. These aren't isolated cases. They signal a sustained enforcement posture across every major jurisdiction.

This guide covers what every crypto firm needs to know right now:

- The regulatory landscape across the US, UK, Canada, and EU

- Core pillars every crypto compliance program must address

- The most common compliance risks firms face

- How to build a defensible compliance function, regardless of company size

Key Takeaways

- Crypto compliance covers AML/KYC, licensing, transaction monitoring, data retention, and cybersecurity — requirements vary significantly by jurisdiction

- The US, UK, Canada, and EU each operate distinct frameworks; cross-border firms must satisfy all relevant obligations simultaneously

- Non-compliance exposes firms to fines, license revocation, enforcement actions, and loss of banking access

- Obligations apply at every stage — seed-stage startups and large exchanges alike; fractional compliance leadership covers the gap without a full-time hire

What Is Crypto Compliance and Why It Matters

Crypto compliance refers to the laws, regulations, and internal practices governing how digital asset businesses handle financial transactions, verify customer identity, report suspicious activity, and protect customer data. The primary goals are preventing money laundering, fraud, terrorist financing, and market manipulation.

The consequences reach further than fines.

What compliance enables:

- Access to banking and payment infrastructure

- Sponsor bank relationships for fiat on/off ramps

- Credibility during Series A/B investor due diligence

- Institutional partnerships that require documented compliance programs

- Regulatory goodwill that matters when rules change quickly

The Federal Reserve's August 2024 enforcement action against Customers Bancorp illustrates how compliance quality directly affects banking access. The written agreement — triggered by BSA/AML and OFAC deficiencies tied to the bank's digital asset strategy — required a full program overhaul and imposed a 30-day notice requirement before any new digital asset products or services could be launched.

That constraint wasn't regulatory abstraction. It was a compliance failure that directly limited the bank's own business operations.

Multiple agencies are watching: FinCEN, the SEC, the CFTC (US), the FCA (UK), FINTRAC (Canada), and ESMA (EU) are all actively monitoring and enforcing. By the time an enforcement action lands, the damage to banking relationships and investor confidence is already done.

The Global Crypto Regulatory Landscape

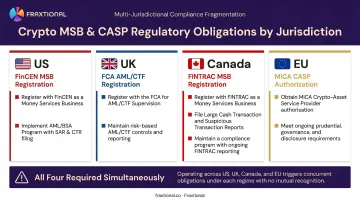

Crypto regulation is not uniform — it varies by jurisdiction, by asset type, and by what your firm actually does. Here's what operators need to know across the four major markets.

United States

The US has no single crypto regulator — jurisdiction depends on what a firm does and what assets it touches.

- FinCEN: Any person accepting and transmitting convertible virtual currency must register as a Money Services Business (MSB) and comply with BSA/AML obligations, including AML programs, recordkeeping, and reporting. Registration is due within 180 days and renews every two calendar years.

- SEC: Asserts jurisdiction over digital assets it deems securities. The SEC's Crypto Task Force, launched January 2025 under Commissioner Hester Peirce, is working to clarify which assets qualify as securities and create paths to registration.

- CFTC: Covers crypto derivatives and futures products.

- GENIUS Act: Signed into law as Public Law 119-27 on July 18, 2025 — a stablecoin framework requiring one-to-one reserves, monthly reserve disclosures, and BSA compliance for issuers.

- CLARITY Act (H.R.3633): Passed the House and was ordered reported with amendment in Senate committee as of May 2026 — not yet enacted. Do not treat it as settled law.

United Kingdom

The FCA requires cryptoasset businesses to register for AML/CTF supervision under the Money Laundering Regulations. The numbers reflect how seriously the FCA takes gatekeeping: of 396 applications received since January 2020, only 63 have been registered (16%) as of May 2026, with 259 withdrawn and 14 refused.

The FCA's 2025 regulatory roadmap is substantial:

| Consultation Paper | Published | Scope |

|---|---|---|

| CP25/14 | May 2025 | Stablecoin issuance and cryptoasset custody |

| CP25/25 | September 2025 | FCA Handbook rules for regulated crypto activities |

| CP25/40 | December 2025 | Trading platforms, lending, staking, DeFi |

Final rules are expected in 2026. The UK Travel Rule for crypto transfers has been in force since September 1, 2023.

Canada

Canada requires all crypto businesses — exchanges, wallet providers, and money services businesses — to register with FINTRAC and implement a full AML compliance program, including a designated compliance officer.

Key obligations include:

- Large virtual currency transaction reports for transactions of CAD $10,000 or more

- Travel Rule compliance for virtual currency transfers

- Written compliance policies reviewed and approved annually by a senior officer

The Binance penalty makes the enforcement posture clear: $6 million for failing to register as a foreign MSB and failing to report large virtual currency transactions. Non-compliance isn't a theoretical risk in Canada — it's an enforcement priority.

European Union

MiCA (Regulation EU 2023/1114) is the most comprehensive crypto regulatory framework globally. ART and EMT (stablecoin) provisions applied from June 30, 2024; the full CASP regime applied from December 30, 2024.

Key obligations for CASPs include:

- Authorization to provide crypto-asset services in the EU

- Capital buffers: minimum €50,000 to €150,000 depending on service class

- Consumer protections, governance requirements, and safeguarding obligations

- Separate compliance tracks for asset-referenced tokens and e-money tokens

The Fragmentation Challenge

A firm operating across all four jurisdictions must satisfy FinCEN MSB registration, FCA AML registration, FINTRAC registration, and MiCA CASP authorization — simultaneously, with no single requirement substituting for another. What's permissible in one market may be restricted in another. Building a compliance program that works across all four requires mapping each regulator's obligations independently — starting with licensing, then AML program requirements, then reporting obligations — before attempting any consolidation.

Core Pillars of a Crypto Compliance Program

AML and KYC

AML and KYC form the foundation of any crypto compliance program.

KYC requires verifying customer identity before onboarding. AML requires ongoing transaction monitoring and suspicious activity reporting (SARs).

The FATF Travel Rule extends these obligations further: VASPs must transmit verified sender and recipient data on qualifying transfers. The threshold is $3,000 in the US, and the rule has been in force in the UK since September 2023 and applies under both FINTRAC and MiCA.

The enforcement record makes the stakes concrete. FinCEN imposed a $29 million penalty against Bittrex in October 2022 for willful BSA violations. BitMEX faced a $100 million enforcement action in August 2021 for operating unregistered and failing BSA obligations.

Both cases involved firms that had customers, transactions, and operations. What they lacked were defensible programs.

Licensing and Registration

Every jurisdiction has its own licensing regime, and operating without required registrations is a primary enforcement target:

- US: FinCEN MSB registration; state-level money transmitter licenses where applicable

- UK: FCA AML/CTF registration under the Money Laundering Regulations

- Canada: FINTRAC MSB or foreign MSB registration

- EU: CASP authorization under MiCA

License revocation — not just fines — is a real consequence of non-compliance. Regulators now coordinate cross-border, which means a deficiency flagged in one jurisdiction can surface in another.

Transaction Monitoring and Sanctions Screening

Crypto firms must monitor on-chain and off-chain transactions, flag suspicious activity, and screen against OFAC, UN, and other global sanctions lists.

Common red flags that trigger enhanced scrutiny:

- Rapid activity across multiple exchanges

- Large transfers inconsistent with customer profile

- Use of privacy coins or mixers

- Connections to high-risk jurisdictions

OFAC sanctions cases against crypto firms illustrate the exposure: Poloniex paid $7.6 million in 2023 for apparent violations involving Crimea, Cuba, Iran, Sudan, and Syria; Kraken paid $362,000 in 2022 for Iran-related violations. Manual review is insufficient at scale. Automated monitoring is now an industry standard.

Data Retention and Recordkeeping

Retention requirements vary by jurisdiction but follow a consistent pattern:

- FinCEN/BSA: SAR copies and supporting documentation retained for 5 years from filing

- UK MLRs: Records kept for 5 years after an occasional transaction or end of business relationship

- MiCA: CASPs must maintain records of services, activities, orders, and transactions

The FTX collapse is the clearest example of what an absence of governance looks like to regulators. The SEC's December 2022 charges cited concealed diversion of customer funds, commingling, and undisclosed risk — a situation enabled by the absence of basic internal controls and documentation.

Regulators and prosecutors will look at your records (or their absence) when things go wrong.

Cybersecurity and Third-Party Risk

Weak recordkeeping and weak security often appear together. Crypto firms handle private keys, customer funds, and sensitive personal data — and the threat environment is severe. According to a 2024 Chainalysis report, crypto hack losses reached $2.2 billion in 2024, with North Korea-linked hacking more than doubling to a record $1.3 billion.

Regulatory expectations now include:

- Documented incident response plans

- Private key management and security protocols (addressed in FCA CP25/14 and ESMA's December 2024 guidelines)

- Formal third-party vendor risk assessments

- Due diligence on counterparties and VASPs, covering their licensing status, jurisdictional footprint, and AML/KYC controls

Firms are accountable not only for their own controls but for the compliance posture of the service providers they work with.

Common Compliance Risks Crypto Firms Face

Regulatory Fragmentation and Rapid Change

DeFi protocols, stablecoins, NFTs, and tokenized assets frequently fall into gray zones where regulatory classification is contested. Firms that assume regulatory silence means permission routinely discover otherwise when enforcement arrives.

Staying current across all applicable jurisdictions takes real resources — which is precisely where many early-stage firms run into trouble.

Resource Constraints at Early-Stage Firms

The compliance burden on a seed-stage crypto startup is effectively the same as on a large exchange. But the resources are not.

Many growing firms lack the budget for a full-time CCO, MLRO, or BSA Officer — yet still face AML, KYC, licensing, and monitoring obligations from day one. The CFTC's FY2024 enforcement record included cases as small as $2.3 million involving digital asset fraud, alongside the headline Binance and FTX matters. A defensible compliance program is a day-one obligation, not something that scales in later once the team grows.

This gap between regulatory obligation and operational capacity is where enforcement risk concentrates for early-stage firms.

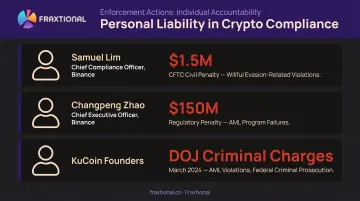

Personal Liability for Compliance Personnel

Regulators have demonstrated willingness to pursue individuals, not just firms. Recent enforcement actions make the stakes concrete:

- Binance's former CCO Samuel Lim was ordered to pay a $1.5 million civil monetary penalty by the CFTC for willful evasion-related violations

- Former Binance CEO Changpeng Zhao was ordered to pay $150 million

- Two KuCoin founders were criminally charged by the DOJ in March 2024 for violating US AML laws

For anyone holding a compliance title — CCO, MLRO, CAMLO, or BSA Officer — personal exposure is real. Qualified, empowered compliance leadership with documented decision-making trails protects the firm and the individual holding the title.

How to Build and Strengthen Your Crypto Compliance Program

Start with a Documented, Risk-Based Approach

Build compliance into operations at launch. A formal risk assessment should map your business activities, customer types, geographies, and products to applicable regulatory obligations — with documented mitigants for identified risks and audit-ready output.

Regulators expect to see this documentation during examinations and licensing reviews. Firms that can produce a current, well-maintained risk assessment are far easier to work with — and far harder to penalize — than those that can't.

Integrate Compliance Across the Business

Avoid siloed compliance systems. KYC/AML onboarding, transaction monitoring, sanctions screening, and suspicious activity reporting should be embedded in the core operating model — not managed as parallel functions.

Fragmented programs are harder to defend to regulators and create more gaps. When a sponsor bank or regulator asks how your controls work together, the answer should be obvious from your documentation.

Access Expert Compliance Leadership Without the Full-Time Cost

For many crypto startups and growing firms, a full-time CCO, MLRO, or BSA Officer isn't financially viable at every stage — but the regulatory obligations don't wait for headcount approvals.

Fractional compliance leadership — the model Fraxtional uses — places a director-level expert in a named role (CCO, CAMLO, MLRO, BSA Officer) on a flexible basis. That leader holds the title, interacts directly with regulators and banking partners, and owns audit readiness, SAR workflows, and regulatory filings.

Fraxtional has supported crypto clients through sponsor bank AML reviews, pre-funding round compliance readiness, and FinCEN registration. One client noted their AML framework was resolved and their sponsor bank review cleared faster than expected.

The engagement model is designed to scale with your business:

- On Demand Advisory — discrete project support for specific regulatory questions or program gaps

- Subscription Advisory — ongoing retainer access for weekly or monthly compliance needs

- Fractional Leadership — a dedicated Director in a named role, stepping in when obligations require it

When the business is ready for a permanent hire, the transition is straightforward. Until then, you're covered.

Frequently Asked Questions

Frequently Asked Questions

What is compliance in crypto?

Crypto compliance covers the laws, regulations, and best practices that govern how digital asset businesses operate — verifying customer identity, monitoring transactions, reporting suspicious activity, and protecting customer data. The core purpose is preventing financial crime while staying in good standing with regulators across every jurisdiction where a firm operates.

What are the crypto regulations?

Crypto regulations vary by jurisdiction and regulator — covering AML/KYC rules (FinCEN, FINTRAC, FCA), licensing regimes (MiCA in the EU, FCA registration in the UK, MSB registration in the US), and stablecoin frameworks (GENIUS Act in the US). There is no single global framework; firms must comply with the rules in every jurisdiction where they operate.

What regulatory protection does crypto have in the UK?

The FCA requires cryptoasset firms to register for AML/CTF supervision. Its 2025 roadmap will introduce rules covering trading platforms, stablecoin issuance, custody, and conduct standards, with final rules expected in 2026. The Travel Rule for crypto transfers has been in force since September 2023, and FCA financial promotions rules apply to UK-facing marketing.

What are the consequences of non-compliance for a crypto firm?

Consequences include fines, enforcement actions, license revocation, and loss of banking relationships. Executives and compliance personnel face personal liability, as the CFTC's actions against Binance leadership demonstrated. Reputational damage from public enforcement actions can permanently impair a firm's ability to operate.

What does a crypto compliance officer do?

A crypto compliance officer (titled CCO, MLRO, CAMLO, or BSA Officer depending on jurisdiction) designs the firm's AML/KYC program, manages regulatory relationships, oversees licensing obligations, and monitors transactions for suspicious activity. Most regulators require a named, qualified individual in this role — not just a policy document.

Do crypto startups need a dedicated compliance officer?

Regulatory obligations apply regardless of company size or stage, and most jurisdictions expect a designated compliance officer from day one. Fractional compliance leadership is a practical path forward — providing director-level expertise, a named title, and audit-ready documentation at a fraction of the cost of a full-time executive hire.