One client working with Fraxtional described it plainly: "We had an AML policy, but it didn't hold up during a sponsor bank review." Having a policy and having governance are two different things.

This guide covers what compliance governance actually means, how it differs from compliance alone, what the GRC framework requires, and how to build a foundation — written for founders and operators who are not compliance experts yet.

Key Takeaways

- Compliance governance is the internal leadership structure that keeps regulatory risk managed continuously, not just at exam time.

- GRC (Governance, Risk, and Compliance) represents three distinct but interdependent pillars that must function together.

- A compliance governance framework defines accountability, identifies risks, sets policies, and establishes monitoring.

- Early-stage fintechs that can't support a full-time CCO can use fractional compliance leadership as a practical alternative.

What Is Compliance Governance?

Compliance governance is the internal leadership system through which an organization manages regulatory risk, adheres to applicable laws, and enforces the policies that flow from those obligations. The key word is ownership — governance is about who is responsible, not just what the rules say.

A well-functioning compliance governance structure typically involves:

- Board of directors — sets the tone and holds leadership accountable

- CEO and CFO — own the consequences and resource decisions

- Compliance Officer or BSA Officer — day-to-day program ownership

- Risk Officer — identifies and monitors exposure across the business

- Heads of Product and Operations — compliance-adjacent accountability where their functions create regulatory risk

Without this structure, you may have compliance documents without compliance ownership — and those are very different things.

Governance vs. Compliance: What's the Difference?

Compliance (or regulatory compliance) refers to the act of adhering to specific external laws and regulations — BSA/AML rules, Reg E, UDAAP, GDPR, FCA requirements, and others depending on your product and geography.

Governance is the internal system that ensures those obligations are actually being met and owned by the right people. Who is accountable, what structures are in place, and how decisions get escalated — that's governance.

A concrete example: a fintech has a written AML policy — policy on paper, nothing more. If no designated officer is enforcing it, monitoring transactions, or filing SARs, the program exists in name only. Regulators will find that gap.

That gap is exactly what a formal GRC framework is designed to close.

The GRC Framework

ISACA defines Governance, Risk, and Compliance as an integrated approach that helps organizations align activities to business objectives, manage risk, and stay in compliance with regulations. All three components must function together:

| Pillar | What It Covers |

|---|---|

| Governance | People, roles, and structures that set tone and ensure accountability |

| Risk Management | Identifying exposures and putting controls in place before they become violations |

| Compliance | Executing against specific regulations and demonstrating adherence to regulators and banking partners |

Treating these as separate workstreams creates real exposure. A company might flag an AML risk but never update its policies — or update policies but leave no one accountable for the fix. That's how enforcement actions happen even when a firm believed it was "doing compliance."

The Key Elements of a Compliance Governance Framework

A compliance governance framework is built in layers, not all at once. The OCC and CFPB both identify board and management oversight as core components of any compliance management system, with policies, training, monitoring, and corrective action rounding out the program.

Here's how to think about it in practice:

Step 1: Map Your Regulatory Obligations

Start with what applies to you based on your product, geography, and customer profile. Fintechs and money transmitters typically face a layered set of obligations:

- BSA/AML requirements under 31 CFR 1022.210 (US)

- State money transmission licensing requirements (US)

- Data privacy regulations (GDPR in EU, CCPA in California, PIPEDA in Canada)

- Consumer protection rules (Reg E, UDAAP)

- FCA registration for UK crypto and e-money businesses

- FINTRAC registration for Canadian MSBs and foreign MSBs

Multi-jurisdiction operators need obligations mapped by country — a single generic AML policy covering the US, UK, EU, and Canada will not satisfy any of them.

Step 2: Define Accountability

Assign explicit ownership of compliance functions to specific individuals or roles. This means naming who is responsible for:

- Policy maintenance and updates

- Regulatory reporting (SARs, CTRs, exam responses)

- Exam and audit readiness

- Escalation of compliance issues to leadership

Vague ownership — "the legal team handles it" or "the CEO is responsible for compliance" — will not hold up under regulatory scrutiny or sponsor bank due diligence.

Step 3: Build Policies and Controls

Translate regulatory requirements into written internal policies: AML program documentation, privacy policy, complaint management procedures, and so on. Then build the operational controls that enforce those policies day to day.

"We didn't know" is not an acceptable response to a regulator. Documented policies paired with enforceable controls create the paper trail that shows your program is real and operational — not just written down.

Step 4: Train and Communicate

Everyone with compliance-adjacent responsibilities needs to understand what's expected of them. Training is a recurring obligation, not a one-time onboarding checkbox. Training records also serve as evidence during exams that your program is actively maintained.

Step 5: Monitor, Test, and Enforce

This is what separates a functional compliance governance program from a paper exercise:

- Audit whether policies are being followed

- Detect gaps or violations before regulators do

- Report findings to leadership with documented minutes

- Update the framework as regulations change

Regulators and sponsor banks scrutinize this ongoing cycle most closely. A policy that exists but isn't tested, enforced, or updated won't pass examination — regardless of how well it was written at launch.

Why Compliance Governance Matters for Fintechs and Startups

The enforcement record across jurisdictions makes the stakes concrete.

Regulatory Consequences

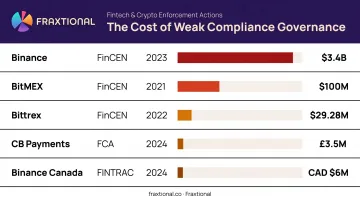

- Binance received a $3.4 billion civil money penalty from FinCEN in 2023 for BSA violations

- BitMEX was fined $100 million by FinCEN in 2021 for operating without a registered AML program

- Bittrex faced a $29.28 million FinCEN action in 2022, partly because the firm relied on as few as two employees with minimal AML training to manually review more than 20,000 transactions per day

- CB Payments Limited (Coinbase's UK entity) was fined £3,503,546 by the FCA in 2024 after onboarding 13,416 high-risk customers in breach of a regulatory requirement — with control failures undiscovered for nearly two years

- Binance Holdings Limited was penalized CAD 6,002,000 by FINTRAC in 2024 for non-compliance with Canadian AML obligations

These cases share a common thread: governance structures that couldn't translate written policy into operational controls. The regulatory fallout is severe — but so is the commercial impact.

Sponsor Bank Consequences

The regulatory risk extends directly into business viability. According to an American Bankers Association comment filed with the Federal Reserve, between early 2023 and early 2024, 25.6% of FDIC formal enforcement actions, 22% of OCC formal orders, and 14% of Federal Reserve enforcement activity involved fintech partner banks — a clear signal that sponsor banks are under mounting pressure to vet their fintech partners more rigorously.

Sponsor banks increasingly require evidence of mature compliance governance before entering BaaS partnerships. Weak governance blocks market access regardless of how strong the product is.

Fraxtional's experience facilitating sponsor bank relationships confirms this. Before committing to a partnership, banks typically require:

- Named executive accountability (a designated BSA Officer or CCO)

- Documented AML programs with written policies and procedures

- Transaction monitoring infrastructure with defined escalation paths

- Audit-ready reporting and evidence of ongoing oversight

A missing BSA Officer or policy gaps discovered during due diligence can delay or kill an onboarding entirely.

Cross-Border Complexity

Companies operating across the US, UK, EU, and Canada face overlapping — and sometimes conflicting — regulatory obligations. The FATF provides a risk-based framework for virtual assets, but FCA, FINTRAC, EBA, and FinCEN each impose jurisdiction-specific requirements on top of that baseline. Governance structures need to assign explicit ownership for each jurisdiction — a single global policy rarely satisfies all four regulators simultaneously.

Who Owns Compliance Governance at a Startup?

In mature organizations, compliance governance sits with a dedicated Chief Compliance Officer, BSA Officer, or MLRO. Early-stage fintechs and crypto firms rarely have the budget or need for a full-time compliance executive from day one — but that doesn't mean the role can go unfilled.

The Risk of Undefined Ownership

Assigning compliance responsibility to a non-expert — the CEO, a generalist lawyer, or whoever has the most bandwidth — creates a gap that regulators and sponsor banks will find. The FFIEC expects BSA compliance officers to have appropriate authority, independence, access to resources, and genuine competence. "Our CEO oversees compliance" does not satisfy that standard.

The most expensive compliance failures tend to happen when undefined ownership meets a regulatory exam or sponsor bank review at the same time.

Fractional Compliance Leadership as a Practical Solution

Fractional compliance leadership addresses this gap directly. An experienced director-level professional provides part-time or project-based services, taking on your named CCO, BSA Officer, CAMLO, or MLRO role without the cost of a full-time executive hire.

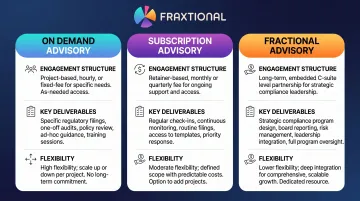

Fraxtional applies this model for fintech, crypto, and embedded finance companies across the US, UK, Canada, and EU. Three engagement structures are available:

- On Demand Advisory — flat fee for discrete projects like audits, risk assessments, or sponsor bank preparation

- Subscription Advisory — monthly or weekly retainer with a dedicated Director, adjustable as your needs change

- Fractional Advisory — monthly retainer with named title use (CCO, CRO, BSA Officer, CAMLO, MLRO), designed for companies that need full executive accountability without a full-time hire

The team holds CAMS certifications alongside Certified Bitcoin Professional and Certified Ethereum Professional credentials — relevant for crypto-adjacent compliance roles. Directors embed with client teams, represent the business to regulators and banks, and take ownership of filings, audits, and escalations. That's a different arrangement from receiving outside advice.

On cost, fractional CRO and CCO engagements typically run 50–70% less than a full-time executive hire — with the added advantage of immediate deployment rather than a months-long search.

Common Compliance Governance Risks to Watch For

Several patterns show up repeatedly in fintech compliance failures:

- Conflicts of interest at the leadership level — when the person responsible for compliance also has P&L accountability, independence erodes

- Siloed teams — product, engineering, and operations teams that don't surface compliance issues creates blind spots that regulators and auditors exploit

- Paper programs — governance structures that exist in documentation but aren't operationally enforced; the FCA's action against CB Payments cited lack of "skill, care, and diligence" in the monitoring of controls, not just their design

- Stale policies — regulations change, and policies that aren't updated to reflect those changes become liabilities rather than protections

Structural safeguards that reduce these risks:

- Regular compliance committee meetings with documented minutes

- Escalation paths that go directly to board level for material issues

- Periodic third-party reviews of the compliance program — independent audits catch what internal teams miss

- A culture where compliance is treated as a strategic function, not an annual checkbox

These safeguards matter because enforcement actions rarely target policy gaps alone — they expose operational ones. The Bittrex case is a direct example: two employees manually reviewing tens of thousands of daily transactions. That's not a governance structure. It's the kind of resource shortfall that turns a routine exam into a consent order.

Frequently Asked Questions

What does compliance governance mean?

Compliance governance is the internal leadership structure — covering the people, processes, and policies — that ensures an organization meets its regulatory obligations and manages risk continuously. It's about ownership and accountability, not just documentation.

What is the difference between governance and compliance?

Compliance refers to adhering to specific laws and regulations. Governance is the internal system of accountability that makes compliance happen. Governance answers "who is responsible"; compliance defines "what they must follow."

What are the 4 pillars of governance?

The four pillars are:

- Accountability — clear ownership of decisions

- Transparency — accurate disclosure to stakeholders

- Fairness — equitable treatment of all parties

- Responsibility — acting in the best interests of the organization and its stakeholders

What are the 7 elements of compliance?

The seven elements are:

- Written policies and procedures

- Designated compliance leadership

- Training and education

- Monitoring and auditing

- Reporting mechanisms

- Enforcement and discipline

- Response and prevention procedures

When should a fintech startup build a compliance governance framework?

Before the company processes customer funds, applies for licenses, or engages with a sponsor bank. Waiting until an exam or compliance failure occurs is significantly more costly in time, money, and business relationships than building the foundation early.

Does a startup need a full-time compliance officer to have good compliance governance?

No. A full-time CCO is not always necessary at early stages. Fractional compliance leadership provides the same level of expertise and accountability at a fraction of the cost, with the flexibility to scale as the business grows. The key requirement is that someone qualified owns the function — not that they're on your payroll full-time.