A qualified opinion on your SOC 2 report can stall a sales cycle. An over-scoped audit drains engineering time for months. A firm that doesn't understand payment processing or crypto custody may miss the controls that actually matter to your prospective bank partners and institutional clients.

Not all CPA firms are equal here. Generic audit firms audit generic companies. If your product touches sponsor bank integrations, tokenized assets, or third-party payment APIs, you need a firm that understands your environment before they test it.

Key Takeaways

- SOC 2 audits must be performed by a licensed CPA firm operating under AICPA standards — verify this before any other conversation.

- Industry-specific experience in fintech, crypto, or embedded finance matters; generalist auditors will misread the scope of complex environments.

- Before signing, confirm the firm offers transparent pricing, a defined methodology, and a structured readiness process.

- Red flags: "guaranteed" outcomes, no partner-level involvement, vague timelines.

- Build your compliance infrastructure before engaging an auditor — it shortens timelines and produces cleaner reports.

What Is a SOC 2 Audit and Why Your Firm Choice Matters

SOC 2 is part of the AICPA's System and Organization Controls suite — a third-party attestation report that evaluates a service organization's controls across five Trust Services Criteria (TSCs): Security, Availability, Processing Integrity, Confidentiality, and Privacy. It has become the baseline trust signal for SaaS, fintech, and data-handling companies operating in the US, UK, and Canada.

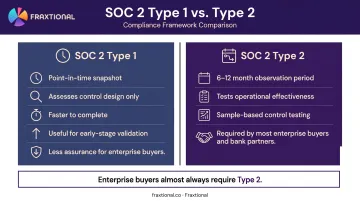

Type 1 vs. Type 2: Why It Changes Your Audit Relationship

The report type you pursue determines the kind of engagement you're entering:

- SOC 2 Type 1 — Assesses whether controls are suitably designed at a single point in time. Faster to complete, useful for early-stage validation.

- SOC 2 Type 2 — Evaluates whether controls operated effectively over a defined period, typically 6–12 months. Includes sample-based testing of control execution. Enterprise buyers almost always require this.

Type 2 means your audit firm is present and active over an extended observation period, not just showing up for a snapshot. Which firm you choose — and how they work — matters far more than it would for a point-in-time review.

The Firm You Choose Is a Strategic Decision

A strong audit firm surfaces control gaps early and guides remediation. A weak one may issue a qualified opinion, miss critical scope elements, or leave your team scrambling to reconstruct evidence mid-fieldwork. Either way, the downstream costs are real:

- Slower sales cycles as prospects wait on a clean report

- Investor hesitation when qualifications or gaps appear

- Re-audits that often cost more than the original engagement

The firm whose name appears on your report also signals something about your compliance posture. Enterprise procurement teams and bank partners read SOC 2 reports closely — and they notice who signed them.

What to Consider When Choosing a SOC 2 Audit Firm

SOC 2 is principles-based, not prescriptive. That means the quality of your audit firm shapes not just the report outcome but how defensible your security program actually is.

AICPA Accreditation and Auditor Independence

Start here. SOC 2 engagements are CPA attestation services performed under AICPA standards — only licensed CPA firms can issue them. This isn't a differentiator; it's a legal requirement.

Two things to verify immediately:

- Confirm the firm is a licensed CPA firm operating under AICPA professional standards. Check their peer review status using the AICPA Peer Review public file search — enrollment status and accepted reviews are publicly accessible.

- Confirm auditor independence. Per AICPA guidance, accountants delivering attestation services must be independent in fact and appearance. A firm that offers to build your controls and then audit them has a conflict of interest that invalidates the report's credibility.

Any firm that cannot confirm CPA status or won't provide written independence documentation should be removed from consideration.

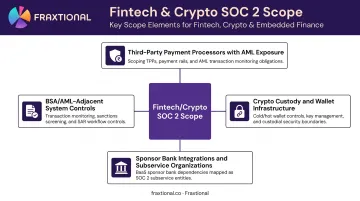

Industry-Specific Experience in Fintech, Crypto, or Embedded Finance

This is where most selection decisions go wrong. A fintech or crypto SOC 2 engagement is not generic SaaS scope.

Your environment likely includes:

- Third-party payment processors with heightened AML exposure (per FFIEC BSA/AML guidance)

- Crypto custody infrastructure, wallet systems, and transaction processing controls

- Sponsor bank integrations and subservice organization dependencies

- BSA/AML-adjacent system controls that generalist auditors may not accurately characterize

Ask prospective firms for examples of SOC 2 reports issued for companies in your sector. If they can't produce them, they're learning your environment at your expense. A misunderstood control environment leads to over-scoping, unnecessary evidence requests, or — at worst — missed risks that surface as findings later.

Audit Scope Definition and Methodology

Vague scoping is one of the most reliable predictors of audit delays and cost overruns. Before engaging any firm, get clear answers on:

- Which TSCs apply to your business model, and why

- Which systems, products, and geographies fall in-scope

- How subservice organizations (cloud providers, payment processors, custody platforms) will be treated — carved out or included

- What evidence types the firm accepts and how they approach control sampling

A credible audit firm has a structured intake process for scope definition. Ask whether they use audit management technology to reduce the evidence-collection burden on your team — firms with automation tooling typically cut fieldwork time by several weeks compared to manual collection processes.

Pricing Transparency and Deliverables

Request a written quote that specifies:

- Total fee and what's included (number of TSCs, systems, entities, locations)

- What triggers additional charges — crypto complexity, multiple subservice organizations, additional report revisions

- Whether the engagement covers Type 1, Type 2, or both, and how pricing differs between them

- Deliverables: draft report with a review period, final report, and management letter if applicable

- Turnaround time from end of fieldwork to draft delivery

Pricing varies significantly based on company size, control complexity, and scope. Don't accept a range without a clear breakdown. Ask each firm to separate audit fees from any advisory or readiness fees — these are different services and should be quoted separately.

Pre-Audit Readiness and Advisory Support

Once pricing is confirmed, ask whether the firm offers a readiness assessment or gap analysis before the formal observation window begins. Completing one before the audit clock starts lets you remediate control deficiencies before they become findings.

The quality of this advisory work varies — and the difference is meaningful:

- Some firms flag gaps and stop there, leaving your team to interpret root cause alone.

- Better firms explain why a control is failing and provide directional guidance on how to fix it properly.

- The best firms treat preparation as a collaborative process, not a checklist exercise.

One-off evidence artifacts created to satisfy an auditor for a single cycle don't build durable compliance programs. Firms that act as advisors during preparation help you build controls that hold up across future audit cycles, reducing remediation work each time you recertify.

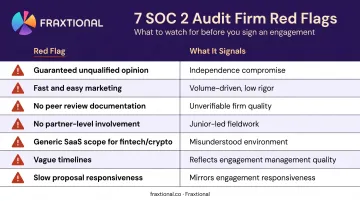

Red Flags to Watch for When Evaluating SOC 2 Audit Firms

Not every CPA firm offering SOC 2 services is equally rigorous. The Journal of Accountancy has warned that promises of "fast and easy" SOC reports can threaten the credibility of the entire engagement, and that high-volume SOC services may come at the cost of quality and objectivity.

Watch for these patterns during your evaluation:

| Red Flag | What It Signals |

|---|---|

| Guaranteed unqualified opinion | Independence compromise — reputable AICPA auditors cannot promise outcomes |

| "Fast and easy" marketing | Volume-driven model prioritizing throughput over rigor |

| No peer review documentation | Unable to confirm firm quality through AICPA's public review program |

| No partner-level involvement | Junior staff completing fieldwork with a partner name on the report |

| Generic SaaS scope for fintech/crypto | Firm doesn't understand your control environment or subservice organization structure |

| Vague or inflated timelines | Reflects how the engagement will run once you've signed |

| Slow proposal-phase responsiveness | Engagement responsiveness usually mirrors sales responsiveness |

Partner involvement deserves specific scrutiny. At larger firms, clients sometimes complete an entire engagement without meaningful input from the credentialed partner who signs the report. Confirm upfront that a named partner will participate in scoping conversations, fieldwork walkthroughs, and report review — not only contract execution.

How Fraxtional Can Help You Prepare for a SOC 2 Audit

Going into a SOC 2 audit without a compliance program in place is expensive. Missing documentation, unclear policy ownership, and weak audit trails are the most common causes of extended timelines and qualified opinions — all of which are preventable with the right preparation.

Fraxtional is a fractional compliance leadership firm that works with fintech, crypto, BaaS banks, and embedded finance companies to build the compliance infrastructure needed before an audit firm arrives. Recognized as a Top 10 Best Fractional Compliance Firm in the US for 2024 and 2025, the firm operates on a Director-led model designed for companies that need audit-ready programs without the overhead of a full-time hire.

What "Director-Led" Actually Means in Practice

Every Fraxtional engagement is led by an experienced Director, not delegated to junior staff. For SOC 2 readiness, that means a Director who stays on every call, reviews every policy, and coordinates directly with your audit firm rather than periodic check-ins.

For companies at seed, Series A, or Series B stage, this provides access to CCO, CRO, BSA Officer, CAMLO, or MLRO-level compliance depth without the cost of a full-time executive hire.

Specific Ways Fraxtional Supports SOC 2 Readiness

- Defining control environments aligned to the Trust Services Criteria relevant to your business model

- Developing information security policies and procedures built around how your company actually operates — not generic frameworks

- Advising on vendor management programs and access control documentation

- Preparing management assertions and audit-ready system descriptions

- Coordinating with your CPA audit firm on evidence requests, scope discussions, and fieldwork walkthroughs

Fraxtional does not perform SOC 2 attestations: that role belongs to a licensed CPA firm. The work happens on your side of the table, getting your controls, policies, and documentation to a state where the audit firm can do their job efficiently and your team isn't scrambling mid-fieldwork.

This is also where multi-jurisdictional context matters. For clients operating across the US, UK, Canada, and EU, Fraxtional's compliance work cross-maps to relevant regulatory frameworks (including AML, GDPR, and sector-specific requirements), so your SOC 2 scope reflects the full picture of how your business operates.

Conclusion

The right SOC 2 audit firm understands your industry, maintains genuine independence, communicates clearly, and stays engaged across the full compliance lifecycle — not just during the active audit period.

Companies that invest in building their compliance infrastructure before engaging an audit firm achieve faster timelines and cleaner reports. SOC 2 is an annual commitment — the controls documentation, evidence workflows, and vendor inventories you establish in year one directly shape what year two costs you.

Frequently Asked Questions

What does a SOC 2 audit mean?

A SOC 2 audit is an independent attestation by a licensed CPA firm that evaluates whether a service organization's controls meet the AICPA's Trust Services Criteria across five categories: Security, Availability, Processing Integrity, Confidentiality, and Privacy. Customers, partners, and investors use the resulting report to assess your security and compliance posture.

Who performs SOC 2 audits?

Only licensed CPA firms operating under AICPA professional standards can conduct SOC 2 audits. The auditor must maintain full independence from the organization being examined. You can verify a firm's peer review status and enrollment through the AICPA's public peer review file search tool.

How much does a SOC 2 audit cost?

Costs vary based on several factors:

- Report type (Type 1 vs. Type 2)

- Number of Trust Services Criteria in scope

- System complexity and subservice organization treatment

- Number of entities, geographies, or fintech/crypto-specific control requirements

Request written quotes from multiple CPA firms that separate audit fees from readiness or advisory fees.

What is the difference between SOC 2 Type 1 and Type 2?

A Type 1 report assesses whether controls are suitably designed at a single point in time. A Type 2 report evaluates whether those controls operated effectively over a defined period — typically 6–12 months — and includes tests of controls and their results. Type 2 provides a higher level of assurance and is what most enterprise buyers and bank partners require.

How long does a SOC 2 audit take?

Type 1 audits move faster, assessing control design at a single point in time. Type 2 audits require a 6–12 month observation period plus fieldwork and reporting. Companies with organized documentation and well-designed controls move through fieldwork faster, so pre-audit readiness directly shapes the total timeline.

Do I need a compliance officer before starting a SOC 2 audit?

Not a formal requirement, but having dedicated compliance leadership in place before engaging an audit firm, whether full-time or fractional, substantially improves outcomes. Controls, evidence, and scope all need to be defined before the audit clock starts — doing that work mid-audit is costly and slow.