Introduction

A fintech startup approaching Series A, a crypto firm negotiating a banking partnership, a company entering M&A — all three hinge on the same process: financial due diligence (FDD). How prepared you are for it will determine whether the deal closes, stalls, or reprices against you.

FDD is how investors, acquirers, and sponsor banks verify that what they're being told matches the financial reality. Being unprepared for it is one of the most common reasons deals lose momentum — or close at a lower valuation than expected.

This article covers what FDD actually is and how it differs from a financial audit. It also walks through what reviewers examine in practice, how to run the process step by step, and what fintech and crypto companies need to know before their first investor review.

Key Takeaways

- FDD is a structured pre-transaction evaluation of financial health — deeper in scope than a standard audit

- It directly affects purchase price, deal structure, and negotiating terms

- Core focus areas: quality of earnings, net debt, working capital, and cash flow sustainability

- Fintech and crypto deals carry added scrutiny on AML programs, regulatory compliance, and licensing status

- Companies with embedded compliance leadership in place before a deal close faster and negotiate from a stronger position

What Is Financial Due Diligence — and Why Does It Matter?

Financial due diligence is a comprehensive evaluation of a company's financial health conducted before a transaction, investment, or partnership. As the ICAEW's 2024 FDD guideline describes it: an objective inquiry into a target's financial position, designed to identify red flags and risks so purchasers and funders can make an informed decision.

FDD covers three dimensions:

- Historical performance — revenue trends, margin patterns, and earnings quality

- Current financial position — balance sheet accuracy, working capital, and liabilities

- Forward-looking projections — whether forecasts are realistic and supportable

The goal is to confirm that stated financials are accurate before the transaction closes.

Why It Directly Affects Deal Economics

FDD reduces information asymmetry between buyer and seller. What gets uncovered shapes more than just confidence — it shapes the deal itself. Purchase price, deal structure, warranties, and indemnities all get adjusted based on FDD findings.

The stakes are real. According to PwC, in one transaction example, a $30M liability discovery was limited by a $10M escrow cap — leaving the buyer absorbing $20M in unexpected losses post-close. Escrow caps don't make surprises disappear; they just determine who absorbs them.

Working capital adjustments are among the most contested outcomes. Bloomberg Law's analysis of ABA deal data found working capital was the most common purchase price adjustment metric, appearing in 89% of deals.

That frequency comes with friction. According to Grant Thornton's 2024 M&A dispute survey, 36% of deals involving working capital adjustments resulted in a dispute — which means getting this right during diligence isn't optional.

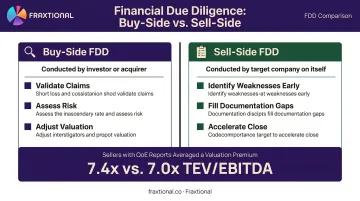

Buy-Side vs. Sell-Side FDD

| Type | Conducted By | Purpose |

|---|---|---|

| Buy-side FDD | Investor or acquirer | Validate claims, assess risk, adjust valuation |

| Sell-side FDD | Target company (on itself) | Identify weaknesses early, fill gaps, accelerate close |

Sell-side FDD is increasingly common — and for good reason. Sellers who commission their own Quality of Earnings reports before going to market averaged 7.4x TEV/EBITDA, compared to 7.0x for sellers without them, according to ACG/GF Data research. That's a measurable valuation premium from simply being prepared.

Financial Due Diligence vs. a Financial Audit: Key Differences

This is where many companies — especially early-stage ones — get tripped up. Having clean audited financials does not mean you're ready for FDD.

An audit, as defined by PCAOB AS 1000, has one objective: to obtain reasonable assurance that financial statements are free of material misstatement, whether due to error or fraud. It confirms compliance with GAAP or IFRS. Full stop.

What it does not tell you:

- Whether underlying earnings are sustainable

- Whether working capital will be adequate post-close

- What the business looks like from a buyer's perspective

Key Structural Differences

| Dimension | Financial Audit | Financial Due Diligence |

|---|---|---|

| Requirement | Legally required (public companies) | Voluntary, deal-driven |

| Timing | Annual, backward-looking | One-time, deal-specific |

| Scope | Standardized (GAAP/IFRS) | Tailored to transaction |

| Output | Audit opinion | FDD report with risk findings |

| Focus | Compliance with standards | Sustainable earnings & deal risk |

The audit certifies the car is roadworthy. The FDD investigator digs into the engine history, checks for unreported accidents, and decides whether it's worth the asking price. One confirms the paperwork is in order. The other tells you what you're actually buying.

ICAEW confirms that FDD is explicitly not an audit or assurance opinion — its scope is determined by the commissioning client and the specific transaction, not by accounting standards. The two serve different masters: the audit satisfies the regulator; the FDD report serves the deal.

What Financial Due Diligence Actually Covers

FDD is not a single analysis — it's a structured review across several distinct financial dimensions.

Quality of Earnings (QoE) Analysis

Because companies are typically valued as a multiple of EBITDA, the QoE analysis sits at the center of most FDD engagements. The goal is to strip out non-recurring revenue and expenses, one-time items, accounting inconsistencies, and management adjustments, arriving at a "sustainable" EBITDA figure that reflects actual earning power.

PitchBook reported that EBITDA adjustments in M&A and lending now account for up to 30% of reported EBITDA figures, up from roughly 10% a decade ago. What's being claimed as earnings and what's actually repeatable can be very different numbers.

Balance Sheet and Net Debt Assessment

The due diligence team examines all assets and liabilities, including off-balance sheet obligations, contingent liabilities, and debt-like items, to calculate net debt. Net debt directly affects valuation and the final purchase price, often flowing through the purchase price adjustment mechanism at closing.

Working Capital Analysis

Net working capital (NWC) — current assets minus current liabilities — is negotiated between buyers and sellers as a closing condition. BDO notes that the NWC target is usually calculated as an average of normalized working capital over the trailing 12 months, adjusted for seasonality and industry conditions. Getting this wrong creates the disputes Grant Thornton identified in 36% of working capital adjustment deals.

Cash Flow and Forward-Looking Analysis

FDD also examines whether reported profits translate into actual cash generation. A company showing strong net income but deteriorating operating cash flow is a warning sign worth investigating.

Beyond historical data, FDD providers interview management to probe accounting policies, off-balance sheet risks, and the assumptions underlying financial forecasts. The key question is whether projected performance is grounded in defensible assumptions or built on growth rates the business has never actually achieved.

How to Conduct Financial Due Diligence: A Step-by-Step Process

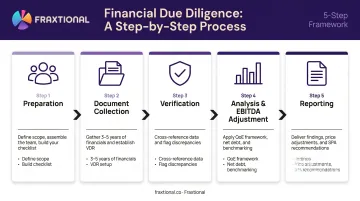

Step 1 — Preparation

Assemble a qualified team: internal finance leads, external transaction advisors, and legal counsel. Define the engagement scope based on deal complexity, and build a comprehensive checklist covering financial, tax, and operational areas. Getting this right upfront is what separates a clean process from one that unravels mid-negotiation.

Step 2 — Document Collection

Gather a minimum of three to five years of:

- Audited financial statements (income statements, balance sheets, cash flow statements)

- Tax returns and regulatory filings

- Management accounts and budgets

- Debt instruments, credit facilities, and creditor schedules

- Accounting policy documentation

Organize everything in a secure virtual data room (VDR). Sell-side advisors should manage VDR contents deliberately: what goes in, and when, carries direct implications for disclosure obligations and negotiating position.

Step 3 — Verification and Cross-Referencing

Cross-check all data for consistency:

- Compare management figures against audited statements

- Verify revenue against underlying contracts and bank statements

- Flag discrepancies, unexplained gaps, or period-over-period variances without clear rationale

Step 4 — Analysis and EBITDA Adjustment

Apply the QoE framework to:

- Adjust reported EBITDA for non-recurring items

- Assess working capital trends against the trailing 12-month normalized baseline

- Calculate net debt across all balance sheet items

- Benchmark key ratios (gross margin, operating margin, debt-to-equity) against industry norms

Step 5 — Reporting

Compile a formal FDD report that:

- Documents all findings and quantifies key risks

- Identifies deal-breakers or price-adjustment items

- Provides specific recommendations for the Sales and Purchase Agreement (SPA)

- Informs negotiation with clear, actionable output

Financial Due Diligence for Fintech and Crypto Companies

Standard FDD is already demanding. For fintech, crypto, and embedded finance companies, there's a second layer of scrutiny that many founders don't see coming until they're already in a live deal.

What Investors and Sponsor Banks Also Examine

Beyond financial statements, investors and sponsor banks look at:

- AML/BSA program adequacy: written policies, transaction monitoring infrastructure, SAR/CTR workflows

- Licensing status: active money transmitter licenses, FinCEN registration, NYDFS BitLicense (where applicable)

- Regulatory history — enforcement actions, consent orders, unresolved examinations

- Compliance leadership — whether a named CCO, BSA Officer, or CAMLO is in place and accountable

The FDIC's guidance on fintech due diligence organizes third-party review around business experience, financial condition, legal and regulatory compliance, risk management controls, information security, and operational resilience. Sponsor banks use the same framework — and they're thorough.

KPMG's Q3 2024 fintech report noted that regulators were intensifying focus on how financial institutions manage risks associated with fintech partners — and that scrutiny has only increased since.

Fintech-Specific Red Flags Investors Look For

- Revenue concentrated in a small number of clients or payment corridors

- Aggressive revenue recognition practices that inflate reported figures

- High customer acquisition costs relative to lifetime value

- Unclear or inconsistent transaction volume reporting

- Unresolved regulatory enforcement actions or outstanding consent orders

The consequences of getting this wrong are significant. FinCEN's $3.4 billion civil money penalty against Binance — the largest in U.S. Treasury history — for willful BSA violations shows what happens when compliance programs can't keep pace with business growth.

Why Early-Stage Companies Are Often Underprepared

Most seed and Series A fintech companies have compliance documentation that's fragmented — pieces of policy here and there, but nothing connected or defensible under scrutiny. When a live deal begins, scrambling to organize compliance documentation delays transactions, erodes negotiating leverage, and signals to investors that governance maturity hasn't kept pace with growth.

The Case for Embedded Compliance Leadership Before a Deal

That gap is fixable — but timing matters. Companies that embed director-level compliance leadership before a deal begins arrive with something concrete investors can review on day one:

- Documented AML program with written policies and monitoring evidence

- Current risk assessments aligned to the company's transaction profile

- Organized regulatory filing history (SARs, CTRs, exam correspondence)

- A named officer who can answer investor questions directly

Fraxtional works with fintech and crypto companies at exactly this stage. Through fractional CCO, CRO, and BSA Officer placements, the firm helps companies produce the compliance documentation — AML program evidence, risk assessment reports, transaction monitoring validation, sponsor bank onboarding materials — that investors and banking partners expect during FDD.

One Series A neobank CEO put it plainly: "We used Fraxtional to rewrite our entire AML stack before a funding round. Our investors were impressed with how ready we were."

The cost and timing advantages are real. Fraxtional's model delivers up to 50–70% cost savings compared to a full-time executive hire, with same-week onboarding rather than a six-month recruitment process — which, for companies approaching a fundraise or banking partnership, can make all the difference.

Common Red Flags Uncovered During Financial Due Diligence

Earnings Quality Issues

Non-recurring revenue items that inflate reported EBITDA — such as one-time contracts, government grants, and asset sales — are among the most common findings in FDD. Inconsistent accounting policy application across periods and unexplained year-over-year margin swings both signal that reported earnings overstate sustainable profitability.

HP's acquisition of Autonomy for $11.6 billion is the cautionary example here. HP recorded an $8.8 billion writedown in 2012, with the Financial Times reporting that more than $5 billion was attributed to accounting improprieties and misrepresentations. The takeaway: EBITDA adjustments that look clean at the surface level can conceal structural revenue problems that only emerge under methodical review.

Hidden Liabilities and Off-Balance Sheet Exposure

FDD regularly surfaces contingent liabilities that don't appear on the face of financial statements: pending litigation, unresolved tax assessments, personal guarantees, regulatory fines, or off-balance sheet financing arrangements. Marsh's 2024 transactional risk claims report found that financial statement breaches accounted for 45% of total R&W claim payments — confirming that these discoveries are both common and expensive.

Working Capital and Cash Flow Inconsistencies

Three specific patterns warrant investigation:

- High days sales outstanding (DSO) or aged receivables concentration — APQC's 2025 cross-industry benchmark puts median collection at 38 days, with bottom performers at 46 days or more

- Deteriorating payables management — extending payables to improve short-term cash position at the expense of supplier relationships

- Growing gap between net income and operating cash flow — a reliable signal of either operational stress or earnings manipulation

Frequently Asked Questions

What is financial due diligence?

Financial due diligence is a structured evaluation of a company's financial health — covering historical performance, current position, and future projections — conducted before a transaction, investment, or partnership. Its purpose is to verify that stated financials are accurate and surface risks before a deal closes.

What are the 4 P's of due diligence?

The 4 P's commonly refer to People (management and team quality), Performance (financial track record), Potential (growth forecasts and market opportunity), and Process (operational and compliance systems). Together, they provide a complete view of a target company beyond financials alone.

How is FDD different from an audit?

An audit confirms that historical financial statements comply with accounting standards. FDD goes further — assessing whether earnings are sustainable, whether working capital is adequate, and what specific risks exist for a transaction. The two are complementary but answer very different questions.

How long does financial due diligence take?

Timeline depends on deal complexity and how well-organized the target's documentation is. Smaller, well-prepared companies can move through in weeks; larger transactions may take several months. Organized financial records and compliance documentation in place before a deal starts is the single biggest factor in compressing that window.

What documents are needed for financial due diligence?

Core requirements include three to five years of audited financial statements, income statements, balance sheets, cash flow statements, tax returns, and management accounts. For regulated companies — particularly fintech and crypto — add regulatory filings, compliance program documentation, licensing records, and AML program evidence.

Who typically conducts financial due diligence?

FDD is typically conducted by the buyer's or investor's team, often with external advisors such as transaction advisory firms, accountants, or legal counsel. Target companies increasingly run sell-side diligence on themselves to identify gaps and validate their financial position before going to market, a practice that's become standard in competitive processes.