Introduction

In 2024, South Carolina overhauled its money transmission framework by adopting the Money Transmission Modernization Act, restructuring financial requirements and fees for anyone transmitting money in the state. If your fintech, payment startup, crypto firm, or embedded finance business operates in South Carolina, that change affects you directly.

The state requires a license under the South Carolina Uniform Money Services Act, administered by the SC Attorney General's Money Services Division.

Operating without one carries real consequences: civil penalties of $1,000 per day per violation and felony criminal liability. This guide walks through who needs the license, the updated application requirements under the 2024 Act, current fees, and what staying compliant looks like once you're approved.

Key Takeaways

- A South Carolina Money Transmitter License is required for selling or issuing payment instruments, storing value, or receiving money for transmission

- Apply through NMLS with a $1,500 application fee and a $1,600 license fee

- Ongoing obligations include quarterly call reports, UAAR filings, AML/BSA policy maintenance, and permissible investments

- Banks, authorized delegates, and entities already licensed under similar state laws may qualify for exemptions

What Is a South Carolina Money Transmitter License and Who Needs One?

A money transmitter license is a state-issued authorization required to engage in money transmission in South Carolina. Under the SC Uniform Money Services Act (S.C. Code Ann. § 35-11-105), money transmission means:

- Selling or issuing payment instruments to persons in South Carolina

- Selling or issuing stored value to persons in South Carolina

- Receiving money or monetary value for transmission

Understanding the SC Licensing Landscape

South Carolina's regulatory framework includes distinct licenses for different financial services:

- Money Transmitter License: Covers businesses moving money on behalf of customers (the subject of this guide)

- Currency Exchange License: Required only if foreign currency exchange accounts for 5% or more of total revenues

- Check Casher License: Administered separately by the SC Board of Financial Institutions, not the Money Services Division

Who Must Apply?

You need a money transmitter license if you operate:

- Payment platforms processing customer-to-customer or business-to-consumer transfers

- Remittance services sending money domestically or internationally

- Digital wallet providers holding or transmitting customer funds

- Payroll processors transmitting funds on behalf of others

- Any fintech that moves funds on behalf of customers rather than on its own account

Key Exemptions

The following entities are exempt from licensing requirements:

- Federally chartered banks and credit unions

- Operators of payment systems clearing between exempt parties

- Authorized delegates (agents) of existing licensees—for example, Western Union agents operating under the licensee's obligations

- Payroll processing services

- Persons appointed as agents to collect and process payments for goods or services

Virtual Currency: The Nuance

Virtual currency businesses often wonder where they stand. South Carolina's Money Services Division issued a December 2018 interpretation clarifying that virtual currencies alone do not qualify as "monetary value" under the Act. That said, if a transaction involves fiat currency conversion or transfer, it may trigger licensing requirements.

Order MSD-19003 specifically addresses Bitcoin ATMs: operators acting as third-party exchangers facilitating contemporaneous exchanges of virtual currency for fiat currency are engaging in money transmission and require a license.

Step-by-Step: How to Apply for a South Carolina Money Transmitter License

The application process has three parallel tracks that must all be completed before a license is granted:

- Completing forms and uploading documents through NMLS

- Emailing select documents directly to the SC Attorney General's office

- Fulfilling pre-application registrations (business registration and FinCEN)

Pre-Application: Register Your Business and Obtain FinCEN Registration

Before starting your NMLS application:

- SC Secretary of State: Corporations, LLCs, and partnerships must register. Sole proprietorships and general partnerships don't need to complete this step.

- FinCEN MSB Registration: Apply for a Money Services Business (MSB) registration number through FinCEN. You'll need this number and your filing date when completing the NMLS application.

Complete the NMLS Application Forms

Create a profile in the Nationwide Multi-State Licensing System (NMLS), then complete:

- MU1 (Company Form): Your entity's core information, business model, and financial details

- MU2 (Individual Form): Required for all control persons — owners, executives, and key managers

Already licensed in other states? South Carolina participates in the MMLA (Multistate Money Services Businesses Licensing Agreement) Phase Two, which offers an abbreviated pathway for companies licensed in states with substantially similar laws.

Upload Required Documents in NMLS

The NMLS platform requires these core documents:

Business Formation & Registration

- Certificate of Authority or Good Standing from SC Secretary of State

- Articles of Incorporation or Organization

- Operating Agreement or Bylaws

Financial Documentation

- Audited financial statements demonstrating required net worth (most recent fiscal year)

- Unaudited interim financial statements (dated within 90 days of application)

- For startups: Audited beginning balance sheet with documentation of capitalization source and method

- List of permissible investments with book and market values

AML/BSA Compliance

- Written AML/BSA policies compliant with 31 CFR Chapter X

- Most recent independent review of AML/BSA program

Background & Credit Checks

- FBI criminal background checks for control persons ($36.25 per person)

- Credit reports for control persons ($15 each)

- Detailed explanation letters for any derogatory credit items (line by line)

Business Operations

- Comprehensive business plan

- Management chart

- Organizational chart (showing direct/indirect owners and subsidiaries)

- Flow of funds description

- Document samples: payment instruments, GLB Privacy Notice

- Sample authorized agent/delegate contract

Submit Additional Documents Directly to the SC Attorney General

Some documents — particularly those involving confidential financials or international background checks — go directly to the SC Attorney General rather than through NMLS. Email these to MSB@scag.gov:

- Parent company financial statements (if applicant is a wholly-owned subsidiary) or EDGAR links for publicly traded parents

- Third-party background checks (for individuals who resided outside the US in the past 5 years)

- Confidential treatment requests specifying each item you want withheld from public disclosure

Submit Your Application and Pay Fees

Complete your NMLS submission and pay:

- $1,500 application fee (non-refundable)

- $1,600 license fee (refunded if application is denied)

If you operate 100 or more authorized agent/delegate locations, you'll also owe $0.25 per active location annually.

Pro tip: Run through the NMLS Money Transmitter License Application Checklist before submitting — it's the fastest way to catch missing documents before the clock starts on review.

Financial Requirements, Fees, and Surety Bond

The 2024 Money Transmission Modernization Act (MTMA) overhauled South Carolina's financial requirements. If you're working from older sources — those citing $750 fees or a flat $50,000 bond — the figures are no longer accurate. Here's what applies now.

Surety Bond Requirement

Your required security amount is the greater of:

- $100,000 minimum, or

- 100% of your average daily money transmission liability in South Carolina for the most recently completed calendar quarter

Maximum: $500,000

The security can be a surety bond, letter of credit, or other security acceptable to the Commissioner. South Carolina accepts Electronic Surety Bonds (ESB) submitted via NMLS.

Net Worth Requirement

Under the 2024 MTMA, the flat $250,000 net worth threshold is gone. The requirement is now tiered based on total assets:

The greater of:

- $100,000 minimum, or

- 3% of the first $100 million in total assets, plus

- 2% of assets between $100 million and $1 billion, plus

- 0.5% of assets over $1 billion

Accepted evidence includes audited or unaudited financial statements. Startups may submit an audited beginning balance sheet with documentation of the source and method of capitalization.

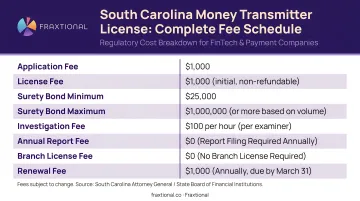

Complete Fee Schedule

| Fee Type | Amount | Notes |

|---|---|---|

| Application Fee | $1,500 | Non-refundable |

| License Fee | $1,600 | Refunded if denied |

| Annual Renewal Fee | $1,600 | Due annually |

| FBI Background Check | $36.25 per person | Per control person |

| Credit Report | $15 per person | Per control person |

| UAAR Fee | $0.25 per location | Only if 100+ active agents; $25,000 annual cap |

Permissible Investments Requirement

Licensees must maintain permissible investments with a market value equal to or greater than their outstanding money transmission obligations in South Carolina. Qualifying assets typically include cash, government securities, and other instruments listed under the MTMA — so prepare a current inventory of eligible holdings before you apply.

Ongoing Compliance Obligations After Licensing

Licensing is step one. South Carolina enforces ongoing reporting and program requirements that continue for as long as you operate — and the penalties for gaps are real.

Quarterly Reporting Requirements

Money Services Call Report: Within 45 days after each quarter ends, file the Call Report through NMLS. This report of condition documents your financial status and South Carolina transaction activity.

UAAR Filings: Report all authorized delegate adjustments (additions, deletions, modifications) via the Uniform Authorized Agent Reporting system within 45 days of quarter-end. Even if there are no changes, you must file a "No Changes to Report" confirmation.

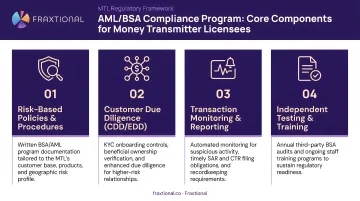

AML/BSA Program Obligations

Licensees must maintain a current Anti-Money Laundering program compliant with 31 CFR 1022.210, including:

- Written AML/BSA policies and procedures

- Designated compliance personnel

- Ongoing training programs

- Independent review proportional to your business's risk profile

The Money Services Division can conduct periodic examinations of licensees and their authorized delegates. Non-compliance can result in civil penalties of $1,000 per day per violation.

Annual Renewal Process

Beyond examinations, your license requires annual renewal to remain active. Key renewal obligations include:

- Annual fee: $1,600 due through NMLS at renewal

- Net worth: Continued demonstration of minimum net worth requirements

- Permissible investments: Maintained at required levels year-round

Failure to meet any of these standards can result in suspension or revocation.

Fractional Compliance Support

For many fintech startups and growing money transmitters, maintaining a full-time compliance executive to cover all of this isn't practical. Fraxtional provides BSA Officer, CCO, and CAMLO services on a flexible basis — so you have experienced compliance leadership handling SC reporting requirements and exam readiness without the overhead of a permanent hire.

Exemptions, Common Mistakes, and Misconceptions

Understanding where the law draws lines saves you from applying when you don't need to — and from skipping the process when you do. Here's what the South Carolina statute actually says on each front.

Key Exemptions Clarified

Banks: Federally and state-chartered banks are exempt unless using non-bank agents for money transmission activities.

Payment System Operators: Operators of payment processing or clearing systems between otherwise exempt parties don't need a license.

Authorized Delegates: Agents of licensed money transmitters don't need their own license for activities covered under the licensed entity's agreement. However, offering additional unlicensed money services on the side would require separate licensure.

Multistate Licensees: Entities already licensed in states with substantially similar laws who obtain SC approval may use an abbreviated application pathway.

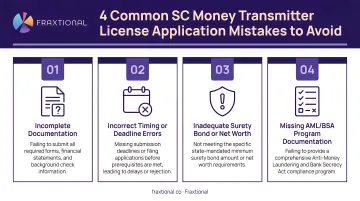

Common Application Mistakes

These four mistakes account for the majority of SC application delays:

- FinCEN registration order: Complete your MSB registration first — your NMLS application requires the registration number and filing date before you can proceed.

- Vague financial statements: Audited statements must clearly show you meet the net worth threshold. Startups need detailed capitalization documentation, not just summary figures.

- Incomplete credit explanations: Every derogatory credit item needs its own explanation letter. A single generic summary won't satisfy reviewers and will stall your file.

- Wrong submission channel: Some documents go to NMLS; others must be emailed directly to MSB@scag.gov. Misrouting a document is one of the most avoidable delays in the process.

Major Misconceptions

"I'm a Western Union agent, so I don't need any oversight": Partially true. You don't need your own license for activities conducted under Western Union's license, but if you offer additional money services independently, you need your own license.

"Pure virtual currency businesses are fully exempt": Not automatically. If your transactions involve fiat currency conversion or transfer—such as operating a Bitcoin ATM—you likely need a license under Order MSD-19003.

Frequently Asked Questions

How much does it cost to get a money transmitter license in South Carolina?

The core costs are a $1,500 non-refundable application fee, $1,600 license fee, a surety bond ranging from $100,000 to $500,000 based on your transaction volume, and demonstrating net worth starting at $100,000 (tiered based on total assets). Background checks and credit reports add $36.25 and $15 per control person, respectively.

What is a money transmitter license?

A money transmitter license is a state-issued authorization required for businesses that sell or issue payment instruments, sell or issue stored value, or receive money or monetary value for transmission on behalf of others.

What can you do with a South Carolina money transmitter license?

With the license, you can legally offer payment instrument sales, stored value services, wire transfers, digital payments, and remittance services to South Carolina consumers and businesses. You can also operate authorized delegate networks within the state.

Do I need a license if I only process virtual currency in South Carolina?

SC's Money Services Division has determined that virtual currencies alone don't qualify as "monetary value" under the Act. However, if your transactions involve fiat currency conversion or transfer, a license may be required. For businesses operating Bitcoin ATMs facilitating fiat-to-crypto exchanges, reference Order MSD-19003 as the relevant guidance.

How long does it take to get a South Carolina money transmitter license?

South Carolina does not publish an official processing timeline. Expect the review process to take several weeks to a few months depending on application completeness and volume. Incomplete applications are the most common cause of delays.

What happens if I operate as a money transmitter in South Carolina without a license?

Unlicensed money transmission in SC can result in civil penalties of $1,000 per day per violation (plus costs and attorneys' fees). Knowing and intentional violations—where you receive more than $500 in compensation within a 30-day period—carry Class B felony criminal liability under the SC Uniform Money Services Act.