Introduction

Most fintech founders don't set out to build a compliance program. They set out to build a product. But from the moment a company processes its first transaction, collects customer data, or approaches a sponsor bank, the regulatory obligations start stacking up.

BSA/AML under FinCEN, consumer protection rules from the CFPB, FCA authorization in the UK, FINTRAC registration in Canada, data privacy rules that apply even when you didn't expect them to — the list grows faster than most early-stage teams anticipate.

The challenge isn't that these obligations are secret. It's that most early-stage companies have no structure for managing them. Rules get tracked in spreadsheets. Compliance becomes someone's side responsibility, risk decisions happen informally, and then a sponsor bank asks for documentation of your program.

GRC — Governance, Risk, and Compliance — is the framework that brings order to that complexity. It connects how a company is led, what risks it faces, and what rules it must follow into one integrated discipline.

This article breaks down each pillar of GRC and shows how to build a functioning program — even if you don't have a dedicated compliance team yet.

Key Takeaways

- GRC stands for Governance, Risk, and Compliance — an integrated framework connecting leadership decisions, risk management, and regulatory obligations.

- The three pillars — Governance, Risk Management, and Compliance — cover oversight, threat control, and regulatory obligations respectively.

- Sponsor banks, investors, and regulators all require evidence of a structured GRC program — fintechs that lack one face real partnership and licensing risk.

- You don't need a large team to start — defined ownership and fractional compliance leadership are enough to build a credible program.

What Is GRC?

GRC stands for Governance, Risk, and Compliance. The term was coined by OCEG (Open Compliance and Ethics Group) in 2002 to describe the three business functions that must work together — rather than in isolation — for an organization to reliably achieve its objectives, manage uncertainty, and act with integrity.

That last phrase matters. GRC is not a checklist. It's a structural discipline that connects leadership, operations, and regulation into a coherent system.

GRC as a Concept vs. GRC as a Program

Two uses of the term are worth separating:

- GRC as a concept is the philosophy — the idea that governance, risk, and compliance are interdependent and should be managed together.

- GRC as a program is how that philosophy gets implemented through policies, controls, processes, assigned roles, and sometimes software.

Many companies have pieces of each pillar in place without ever connecting them. That's not a GRC program: it's three separate functions operating independently, which creates exactly the kind of gaps regulators find during examinations.

What GRC Is Not

That distinction also corrects a persistent misconception: GRC is not synonymous with compliance. Compliance is one of the three pillars. GRC is the broader system that determines how risk gets identified, where decisions get made, and how compliance obligations connect to business strategy.

Running a compliance function without governance or risk management is reactive by definition — you're meeting requirements without any structure for anticipating where the next problem originates.

The Cost of Getting This Wrong

According to the ACFE's 2024 Report to the Nations, a typical organization loses 5% of annual revenue to occupational fraud alone. That figure doesn't capture regulatory penalties, remediation costs, or the downstream damage to partner and investor relationships — all of which follow from unstructured risk and compliance management.

The Three Pillars of GRC Explained

Governance: Setting the Rules of the Road

Governance is the system of policies, leadership structures, and accountability mechanisms that determine how a company makes decisions. It covers who is responsible for what, how ethical conduct is enforced, and how the board or executive team maintains oversight.

In practice, governance for a financial services company looks like:

- Written policies that define acceptable conduct and decision-making authority

- Clear reporting lines and escalation paths for compliance issues

- Board-level or senior leadership risk committees

- Documented procedures for significant decisions — launching a new product, entering a new market, onboarding a new vendor

Without governance, risk management and compliance have no home. Decisions happen informally, ownership is unclear, and when something goes wrong, there's no structure to respond.

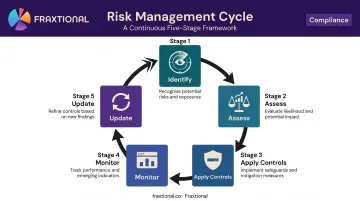

Risk Management: Identifying and Controlling Threats

Risk management is the process of identifying, assessing, prioritizing, and responding to threats before they become incidents or violations. The cycle runs in a continuous loop:

- Identify risks across financial, operational, regulatory, reputational, and cyber dimensions

- Assess likelihood and potential impact

- Apply controls — preventive, detective, or corrective

- Monitor control effectiveness continuously

- Update the risk picture as the business and environment change

For fintechs and banking companies specifically, this must cover BSA/AML risk, credit and fraud risk, cybersecurity threats, and third-party vendor risk. Each of these can generate regulatory liability if left unmanaged.

Compliance: Meeting Regulatory Requirements

Compliance is the ongoing obligation to adhere to external laws and regulations as well as internal policies. Writing your first AML policy is a starting point — maintaining an active, tested compliance program is the actual requirement.

Key compliance domains for fintechs operating across the US, UK, and Canada include:

- BSA/AML — FinCEN registration, AML program requirements under 31 CFR 1022.210, SAR and CTR filing

- UDAAP — CFPB rules on unfair, deceptive, or abusive acts or practices in consumer financial products

- Regulation E — consumer protections for electronic fund transfers and remittance

- KYC/KYB — Customer and business identification programs under FinCEN's CIP requirements

- FCA authorization — payment and e-money firms must be authorized or registered with the FCA before operating in the UK

- FINTRAC registration — Canadian MSBs and foreign MSBs must register before conducting covered activities

- Data privacy — GDPR applies to companies outside the EU targeting EU residents; CCPA applies to qualifying businesses handling California consumer data

Cross-border operators don't get to choose one regime. They have to map all of them simultaneously.

How the Three Pillars Connect

GRC's real value comes from integration, not from each pillar in isolation. Governance creates structure and accountability. Risk management identifies threats within that structure. Compliance ensures the organization meets the external rules that govern it.

When these functions operate in silos, the result is predictable:

- Coverage gaps — risks fall between functions with no owner

- Duplicate effort — teams address the same issues independently

- Examiner blind spots — regulators find what internal siloes missed

- No clear accountability — when something breaks, ownership is contested

Why GRC Is Non-Negotiable for Fintechs and Financial Startups

Sponsor Bank Expectations

For fintechs relying on banking-as-a-service or program bank partnerships, the compliance review comes before the contract. The 2023 interagency guidance on third-party relationships from the Federal Reserve, FDIC, and OCC is clear: a bank's use of third-party fintech partners does not transfer or reduce its own regulatory responsibility.

Banks are therefore highly motivated to verify that fintech partners have functioning compliance programs before they approve a relationship.

In practice, this means sponsor banks expect documented AML programs, assigned compliance leadership, written policies, and evidence of operational controls. A fintech that arrives without these faces delays at best and outright rejection at worst.

One pattern Fraxtional sees regularly: a fintech has an AML policy, but it doesn't hold up under bank review. Getting that documentation right before the bank conversation — not during it — is what separates a 60-day onboarding from a 6-month stall.

Investor and Board Scrutiny

At Series A and beyond, compliance and risk infrastructure have become diligence items. Fintechs now operate under sustained regulatory pressure across every major market, and investors have noticed. Board members and lead investors who watched enforcement actions hit crypto firms and payments companies are asking pointed questions about program maturity before closing deals.

A named CCO or BSA Officer with credentials regulators recognize changes that conversation. It signals the company is building for durability, not just speed.

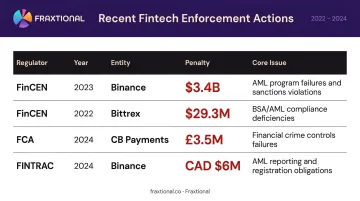

Regulatory Enforcement Is Active

Enforcement is not theoretical. Recent penalties across key jurisdictions illustrate the range of exposure:

| Regulator | Year | Entity | Penalty | Core Issue |

|---|---|---|---|---|

| FinCEN | 2023 | Binance | $3.4B | AML program failures, MSB registration, SAR filing |

| FinCEN | 2022 | Bittrex | $29.3M | AML program and suspicious activity reporting failures |

| FCA | 2024 | CB Payments | £3.5M | Onboarding 13,416 high-risk customers in violation of requirements |

| FINTRAC | 2024 | Binance | CAD $6M | Foreign MSB non-registration, 5,902 unreported transactions |

Penalties range from regulatory fines to license suspension, cease-and-desist orders, and multi-year monitorships. The companies that faced the largest consequences weren't ignoring compliance entirely — many had programs that simply weren't sufficient for their scale or risk profile.

The Business Case Beyond Penalties

A structured compliance and risk posture delivers value well beyond avoiding fines:

- Shortens sponsor bank and payment partner onboarding timelines

- Reduces internal inefficiencies from unclear ownership and reactive fire-fighting

- Builds credibility with investors during fundraising

- Creates a foundation for scaling into new products and geographies without rebuilding compliance from scratch

How to Build a GRC Program from Scratch

Building a GRC program starts with a structured foundation — you refine it over time, not before you begin.

Step 1: Assess Your Current State

Document what already exists — policies, risk processes, compliance activities, assigned roles. Most early-stage fintechs find they have fragments: a privacy policy, an AML document started during bank onboarding, a vendor list somewhere. The goal at this stage is an honest inventory of what's in place and what isn't.

Common gaps Fraxtional identifies when engaging seed-to-Series B clients include:

- Fragmented documentation that hasn't been connected into a program

- No named compliance owner with regulatory accountability

- AML policies that exist on paper but haven't been operationalized

- Risk assessments that are outdated or never completed

Step 2: Map Your Regulatory Obligations

Your obligation set depends on your business model, license type, and where you operate. A US-registered payments company faces different requirements than a crypto exchange with UK customers. List every regulator that governs your activities and the specific requirements each imposes — that map becomes the input for your prioritization exercise.

Step 3: Prioritize by Risk Severity

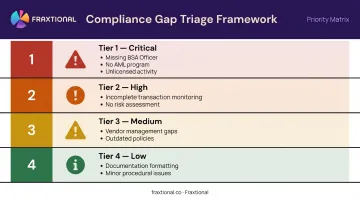

Not all gaps carry the same weight. Missing BSA Officer designation or lacking an AML program creates immediate sponsor bank and regulatory exposure. An incomplete vendor management policy is a gap — but a lower-urgency one. Address high-severity items first, before touching anything else.

A simple triage framework helps here:

- Critical: Missing BSA Officer, no AML program, unlicensed activity

- High: Incomplete transaction monitoring, no risk assessment on file

- Medium: Vendor management gaps, outdated policies

- Low: Documentation formatting, minor procedural inconsistencies

Step 4: Assign Ownership

Name the accountable executive for each GRC pillar. Without a named owner, programs stall. At early-stage companies, these roles are often combined or covered fractionally. Someone specific must be accountable, credentialed, and reachable by regulators and bank partners.

Step 5: Build in Review Cadences

GRC programs are living systems. Set quarterly policy reviews, annual risk assessments, and ongoing compliance monitoring from the start. FINTRAC requires an effectiveness review at least every two years. The FFIEC expects banks and their fintech partners to maintain ongoing monitoring throughout the relationship lifecycle.

Build that discipline in from day one. Retrofitting review cadences into an operating program is significantly harder than establishing them at the start.

GRC Roles and Responsibilities: Who Owns What?

Core GRC Leadership Roles

| Role | Primary Responsibility |

|---|---|

| Chief Compliance Officer (CCO) | Compliance program design, regulatory relationships, policy ownership |

| Chief Risk Officer (CRO) | Enterprise risk framework, risk appetite, cross-functional risk oversight |

| BSA Officer | AML program management, SAR/CTR filing, FinCEN obligations |

| CAMLO | Canadian AML obligations, FINTRAC compliance program |

| MLRO | UK AML obligations, FCA regulatory reporting, suspicious activity oversight |

These roles interact constantly within a functioning GRC structure. The BSA Officer surfaces AML risk findings to the CRO. The CRO's risk framework informs the CCO's compliance priorities. None of them operate effectively in a vacuum.

The Startup Reality

Most seed-to-Series B fintechs cannot justify five separate executive hires. But regulators and sponsor banks still expect the functions to be covered — and they expect named individuals, not just department references in a policy document.

Fractional compliance leadership addresses this gap directly. Fraxtional provides director-led CCO, CRO, BSA Officer, CAMLO, and MLRO services under a monthly retainer, with named title use so clients can list the assigned Director in filings, regulatory submissions, and investor documentation.

The director-led model sets this apart from typical advisory arrangements:

- Directors hold CAMS, ACAMS FCI, ABA CERP, and CFE credentials — what regulators and sponsor banks expect to see

- Clients work directly with the named Director, not an account manager or junior associate

- Directors embed with the team, attend bank reviews, and own audit and regulatory interactions

GRC Belongs to the Whole Organization

Compliance teams don't own GRC alone. Product managers who build customer-facing features, engineers who handle transaction data, and operations leads who manage vendor relationships all carry GRC responsibilities. Successful programs embed accountability across the organization so that risks get flagged before they become violations — not after.

Frequently Asked Questions

What is governance, risk, and compliance (GRC)?

GRC is an integrated framework combining governance (oversight and accountability), risk management (identifying and controlling threats), and compliance (meeting regulatory and legal obligations). The value of GRC lies in treating these three functions as connected. When they're managed in silos, gaps accumulate and exposures go undetected until they become problems.

What are the three pillars of GRC?

The three pillars are Governance (leadership structures and decision-making rules), Risk Management (identifying, assessing, and mitigating threats), and Compliance (adhering to regulations and internal policies). Each pillar depends on the others — remove one and the remaining two lose effectiveness and coherence.

What is the difference between GRC and compliance?

Compliance is one component of GRC focused on meeting external laws and internal policies. GRC is the broader system that also includes governance structures and risk management processes. Running compliance without the other two pillars means you're responding to requirements rather than anticipating and managing them strategically.

Who is responsible for GRC in an organization?

GRC responsibility is shared across the CCO, CRO, and BSA Officer or MLRO at the leadership level, with board-level oversight. In smaller or early-stage companies, these responsibilities are often consolidated or covered through fractional leadership arrangements where a named Director holds the designated title and accountability.

What happens if a fintech doesn't have a GRC framework?

The consequences are practical and immediate: failed sponsor bank partnerships, regulatory enforcement exposure (fines, license issues, monitorships), weakened investor confidence, and undetected risk accumulation. For early-stage companies without the capital or reputation buffer to absorb them, each of these can be decisive.

When should a fintech start building its GRC program?

Before it processes customer funds, pursues a banking license, or engages a sponsor bank. Waiting until a regulatory examination or investor due diligence request arrives is too late — GRC programs require time to demonstrate consistent operation, and regulators and banks both evaluate program maturity, not just policy documents.