Introduction

Most compliance teams in financial services find out about regulatory changes the same way — after the fact. A new rule takes effect, an enforcement action lands, or a sponsor bank raises a concern, and suddenly the scramble begins. This reactive pattern is exactly what horizon scanning is designed to prevent.

Thomson Reuters Regulatory Intelligence tracked 61,228 regulatory events in 2022 — roughly 234 alerts per working day — across 1,374 regulators in 190 countries. For compliance teams at fintechs, banks, and crypto firms, that volume makes passive monitoring untenable.

If you're a CCO, MLRO, BSA Officer, or fintech founder operating in the UK, US, Canada, or EU, this guide covers what horizon scanning is, how it works in practice, and what distinguishes teams that do it well from those that treat it as an afterthought.

Key Takeaways

- Horizon scanning is the continuous process of identifying and assessing regulatory changes before they become binding requirements.

- It differs from regulatory change management — scanning is the early-warning function; change management is the response.

- Three core stages drive the process: monitoring authoritative sources, filtering for relevance, and escalating assessed business impact.

- Running it as a quarterly review instead of an ongoing function is where most compliance teams fall short.

- Without a named owner — especially in lean fintech teams — horizon scanning simply won't happen.

What Is Horizon Scanning in Regulatory Compliance?

Horizon scanning is the continuous, structured practice of identifying emerging laws, regulatory guidance, consultation papers, and enforcement trends before they become binding obligations. The goal is straightforward: give compliance teams enough lead time to assess impact, update policies and controls, train staff, and avoid enforcement action.

The Bank of England defines it as "systematically exploring and understanding fundamental change, risks and opportunities that have the potential to reshape the challenges faced" by an organization.

The Basel Committee on Banking Supervision published its own horizon scanning report in 2025, focused on banks' interconnections with non-bank financial intermediaries. That regulators themselves use the concept as a forward-looking supervisory tool should tell you something about how seriously it needs to be taken.

Horizon Scanning vs. Regulatory Change Management

These two functions are often conflated, but they are sequential rather than interchangeable:

| Function | What it does | When it happens |

|---|---|---|

| Horizon scanning | Identifies incoming regulatory changes | Before requirements become binding |

| Regulatory change management | Implements the firm's response | After changes are identified and assessed |

Think of horizon scanning as the early-warning system and regulatory change management as the response protocol. Without the first, the second always begins from a reactive position — and in fast-moving areas like crypto regulation or BaaS oversight, that lag has real consequences.

Why Compliance Teams in Financial Services Can't Afford to Skip It

The pace of regulatory output alone makes the case. 73% of compliance professionals expected regulatory activity to increase in 2023, and bank compliance employee time rose 61% between 2016 and 2023 — compared to just 20% growth in total employee hours. The compliance function is carrying a disproportionate and growing load.

The Cost of Missing a Regulatory Window

Three FCA enforcement actions in 2024 illustrate what happens when monitoring and control updates fall behind:

- Starling Bank — fined £28.96 million for financial crime systems and controls failings, including opening 54,359 accounts for high-risk customers and screening against only a fraction of the Consolidated Sanctions List. The FCA cited inadequate financial sanctions policies that required updating.

- CB Payments Limited (Coinbase Group) — fined £3.50 million after onboarding 13,416 high-risk customers in breach of a regulatory requirement, with monitoring failures leaving the breach undiscovered for nearly two years.

- Metro Bank — fined £16.68 million for failing to monitor over 60 million transactions worth more than £51 billion, and for failing to maintain risk-sensitive ongoing monitoring procedures.

Each reflected a failure to translate regulatory obligations into updated, functioning controls — exactly the outcome horizon scanning is designed to prevent.

Implementation Windows Are Finite

Regulators typically signal major changes well in advance. The question is whether firms are paying attention:

- FinCEN BOI Reporting Rule — published September 2022, effective January 2024 (15-month window)

- FCA Consumer Duty — final rules published July 2022, core implementation July 2023

- MiCA — entered force June 2023, stablecoin provisions from June 2024, broader CASP regime from December 2024

These windows exist. Firms that miss them do so not because regulators moved without warning, but because no one was watching the pipeline.

Beyond Compliance: Strategic Value

Firms that identify regulatory shifts early can also act on them strategically — adapting product roadmaps, pursuing new licences, or positioning ahead of competitors still reacting. For crypto firms tracking MiCA's phased rollout, those that completed readiness assessments before the June 2024 stablecoin deadline were able to launch compliant products while competitors were still scoping what the rules required.

How the Horizon Scanning Process Works Step by Step

Three steps separate firms that catch regulatory changes early from those that get blindsided: knowing what to watch, filtering out the noise, and making sure findings actually drive action.

Step 1: Define Scope and Establish Monitoring Channels

Before you can monitor anything effectively, you need to define what you're monitoring. That means identifying:

- Which regulators are relevant (e.g., FCA, PRA, FinCEN, CFPB, OSFI, EBA, ESMA)

- Which jurisdictions the firm operates in or plans to enter

- Which regulatory topic areas apply to the business model (AML/BSA, consumer protection, data privacy, crypto assets, etc.)

Primary authoritative sources by jurisdiction:

| Regulator | What to monitor |

|---|---|

| FCA (UK) | Consultations, policy statements, supervisory statements, enforcement notices |

| FinCEN (US) | BSA guidance, advisories, bulletins, pending rulemakings |

| CFPB (US) | Final rules, rules under development, regulatory agenda |

| OSFI (Canada) | Guidelines, advisories, regulatory guidance documents |

| EBA (EU) | RTS/ITS, guidelines, consultations, Single Rulebook updates |

The FCA's Regulatory Initiatives Grid (10th Edition, May 2026) is particularly useful — it lists 135 live initiatives across a 24-month forward pipeline. That's a structured, publicly available horizon view that many firms simply aren't using.

Beyond official sources, industry association bulletins and subscription-based regulatory intelligence platforms fill gaps that manual monitoring misses.

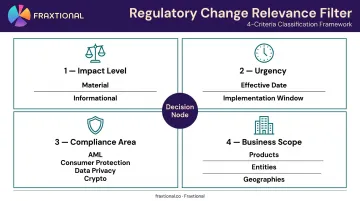

Step 2: Filter, Classify, and Assess Relevance

Raw regulatory output must be screened for applicability. Not every FCA consultation affects every firm — the filtering step is where relevance is determined.

Each potentially relevant change should be classified by:

- Impact level — material change to obligations, or informational update

- Urgency — effective date and implementation window

- Compliance area — AML/sanctions, consumer protection, data privacy, crypto assets, etc.

- Business scope — which products, entities, or geographies are affected

This is also where most teams fail. Poor filtering wastes time on irrelevant material or — worse — misses critical changes because the screening criteria aren't fit for purpose.

Step 3: Escalate Findings and Integrate into the Compliance Program

Assessed findings need to move somewhere. Firms that stop at monitoring and never convert findings into program changes are still exposed — they just have paperwork to show for it.

Findings should be:

- Escalated to the CCO, legal counsel, or board when the impact is material

- Converted into action plans with named owners and realistic implementation timelines

- Embedded into policy reviews, control updates, and staff training cycles

This is where a fractional CCO, BSA Officer, MLRO, or CAMLO earns their place — not just flagging what's changing, but driving the response across the compliance program. Fraxtional's fractional leaders handle exactly this function as part of their ongoing engagement.

Key Factors That Shape Horizon Scanning Effectiveness

Jurisdictional Complexity

Firms operating across the UK, US, Canada, and EU face a monitoring task that is larger and more fragmented than single-jurisdiction businesses. KPMG's 2025 mid-year regulatory report flagged growing regulatory divergence and fragmentation as a defining trend — meaning overlapping or conflicting requirements across borders are increasing, not decreasing.

Scope must be defined deliberately. A firm that monitors only US federal regulators while operating a UK-regulated entity has a structural blind spot, regardless of how well it monitors within each jurisdiction.

Seniority and Regulatory Depth of the Compliance Function

Horizon scanning requires someone who can distinguish a material change from a minor update, interpret consultation papers accurately, and translate findings into concrete actions. That's not a task for a junior analyst working from a newsletter.

For fintech startups and early-stage crypto firms without a full-time CCO, this function is frequently unassigned or handed to someone without the regulatory background to run it properly. Regulatory depth in this context means:

- Recognizing when a consultation paper signals a likely rule change versus routine guidance

- Mapping an FCA supervisory update or OSFI guidance revision to the firm's specific obligations

- Distinguishing BSA/AML program implications from crypto-specific regime changes

A fractional compliance officer with that depth changes the outcome. Fraxtional's fractional CCO and MLRO engagements explicitly include monitoring regulatory changes and applying them to the client's business — which is how horizon scanning gets embedded in the compliance function without a full-time hire.

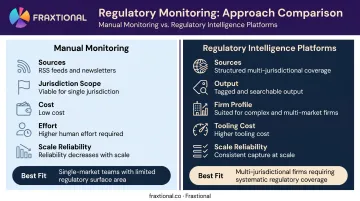

Tooling and Source Coverage

The right approach depends on firm size, jurisdictional footprint, and risk profile:

- Manual monitoring (regulator RSS feeds, newsletters, industry alerts) — viable for narrow-scope, single-jurisdiction firms; becomes unreliable as jurisdictional coverage grows

- Regulatory intelligence platforms — provide structured, tagged, multi-jurisdictional coverage; appropriate for firms with complex or multi-market exposure

The tool determines what gets captured. Who reviews it determines whether the firm actually responds.

Common Misconceptions About Regulatory Horizon Scanning

"Monitoring is the same as horizon scanning"

Subscribing to regulator newsletters is the first step, not the whole process. Monitoring provides the raw input; it only becomes horizon scanning when it's followed by structured relevance filtering and impact assessment that feeds into the compliance program. Many teams tick the monitoring box and stop there.

"A quarterly review is sufficient"

Regulation doesn't follow a quarterly calendar. FinCEN can release guidance on a Tuesday; the FCA publishes consultation papers on a rolling basis; ESMA issued MiCA technical standards in phases across 18 months. A periodic cadence creates gaps where material changes are missed entirely. Horizon scanning should be continuous, with regular reporting intervals built in — not a once-a-quarter exercise that feels like an annual audit.

"This only matters once we're at scale"

Enforcement data tells a consistent story. Recent actions span business models and geographies:

- The CFPB ordered Chime Financial — a fintech, not a traditional bank — to pay a $3.25 million civil penalty in 2024

- The FCA fined CB Payments (Coinbase Group) £3.5 million

- Enforcement actions against MoneyLion, money transmitters, and crypto exchanges reinforce the same point: business model and company size do not create a compliance exemption

Early-stage fintechs and crypto startups that deprioritize horizon scanning often assume it's a large-firm concern. It isn't. Establishing the process early — even in a lightweight form — is far less disruptive than retrofitting it after a regulatory event, an investor due diligence review, or a sponsor bank audit.

Miss a material regulatory change at Series A and you're not just fixing a compliance gap — you're explaining it to your sponsor bank and your next lead investor.

Frequently Asked Questions

What is horizon scanning in compliance?

Horizon scanning in compliance is the structured, ongoing process of identifying and assessing emerging regulatory changes before they take effect. It gives organisations time to prepare, update controls, and train staff — rather than responding to enforcement after the fact.

What is horizon scanning in the context of the FCA?

In the FCA context, horizon scanning means tracking the FCA's pipeline of consultation papers, policy statements, supervisory expectations, and enforcement trends. The FCA's Regulatory Initiatives Grid currently lists 135 live initiatives across a 24-month forward window. Firms that monitor this pipeline can respond before requirements become binding.

How does horizon scanning differ from regulatory change management?

Horizon scanning identifies what regulatory changes are coming; regulatory change management implements the firm's response. The two are sequential and complementary — scanning provides the early warning, change management acts on it. Both functions are necessary: one without the other leaves a firm either unprepared or without direction.

Who is responsible for horizon scanning in a fintech company?

Horizon scanning is typically owned by the CCO or a senior compliance function. In lean fintech or crypto teams without a full-time CCO, a fractional compliance officer usually takes the lead — bringing the regulatory expertise to assess materiality and translate findings into action plans.

How often should regulatory horizon scanning be conducted?

It should be continuous, not periodic. A practical structure is weekly monitoring of regulatory sources, monthly briefings to relevant stakeholders, and quarterly reviews of the horizon scanning scope and process itself. Regulatory changes can be released at any time, and a periodic-only cadence creates gaps.

What is the difference between horizon scanning and a compliance audit?

A compliance audit assesses whether current controls meet existing requirements. Horizon scanning looks forward — it identifies what requirements are coming before they apply. Both are necessary, but they serve different purposes in a compliance program.