FinCEN's 2024 record $1.3 billion penalty against TD Bank — the largest ever against a US depository institution — included a mandatory SAR lookback requirement. TD had failed to monitor over $18 trillion in transaction activity from 2014 to 2023. That is not a monitoring gap. That is a monitoring absence.

The instinct is to treat a lookback as a burden. A better way to frame it: a lookback is one of the few compliance exercises that tells you what your program actually missed, not just what it detected. Institutions that treat it as a diagnostic tool come out stronger. Those that treat it as a checkbox come out vulnerable.

This article explains what AML lookbacks are, what triggers them, and how to approach them in a way that produces lasting compliance value rather than a one-time paperwork exercise.

Key Takeaways

- An AML lookback is a retrospective review of transactions to identify suspicious activity missed during routine monitoring

- Triggers include regulatory enforcement actions, system failures, internal audit findings, mergers, and proactive compliance reviews

- Well-executed lookbacks close monitoring gaps and reduce future enforcement exposure

- Ignored or poorly managed lookbacks compound into SAR backlogs, escalated penalties, and repeat findings

- Without director-level AML leadership, lookbacks rarely satisfy examiner scrutiny — whether that's in-house or fractional

What Is an AML Lookback?

An AML lookback is a backward-looking review of a financial institution's historical transaction data — typically spanning months to years — conducted to identify suspicious activity, KYC failures, or monitoring gaps that were not flagged during routine oversight.

Lookbacks apply across a wide range of regulated entities:

- Banks and credit unions

- Fintechs and embedded finance companies

- Money transmitters and payment processors

- Crypto exchanges and digital asset firms

- Correspondent banks and insurance companies

- BaaS providers and their fintech partners

The scope can include wire transfers, currency exchanges, fund deposits, high-risk account activity, and any transaction type covered by the institution's monitoring obligations.

A lookback functions as a diagnostic tool. It answers one question: did the AML program actually work? Not whether controls were documented, but whether they caught what they were supposed to catch. When a system is misconfigured, a rule set is outdated, or a product line is added without corresponding monitoring updates, transactions slip through.

A lookback finds them.

For many fintechs and crypto firms, the first lookback is also the first honest assessment of whether their monitoring program functioned as designed: or whether it just existed on paper.

Key Advantages of Conducting AML Lookbacks

Uncovering Missed Suspicious Activity Before Regulators Do

The primary function of a lookback is detection: finding transactions, patterns, and behaviors that slipped through existing monitoring. Common causes include misconfigured alert rules, suppressed transaction codes, incomplete customer data, and monitoring logic that predates emerging typologies.

In practice, the process involves defining scope, extracting historical data, applying detection logic to the relevant population, and investigating flagged items for SAR filing consideration. It often surfaces activity that predates a specific system failure or rule gap — not just isolated transactions, but patterns that should have generated alerts months or years earlier.

Why this matters: Institutions that identify and file missed SARs proactively signal good faith to regulators. FinCEN's enforcement policy explicitly considers the quality and extent of cooperation — including timely and voluntary disclosure — when evaluating enforcement outcomes. The difference between self-identifying a gap and having a regulator find it first is often the difference between a manageable remediation and a consent order.

The Coinbase Europe case illustrates what happens when missed filings accumulate. The Central Bank of Ireland found that monitoring failures resulted in 2,708 late STRs tied to over 30 million unmonitored transactions worth more than €176 billion — a backlog that took nearly three years to work through, alongside a €21.46 million penalty.

KPIs directly affected:

- SAR filing completeness

- Alert disposition accuracy

- Suspicious activity detection rate

- Enforcement action severity

Most relevant when: A monitoring system has been offline, misconfigured, or newly implemented; when emerging typologies like crypto-related layering weren't covered by existing rules; or when entering new product lines or geographies.

Strengthening the AML Monitoring Program Itself

A lookback doesn't just surface missed transactions — it exposes the reasons they were missed. That distinction matters. Finding a missed SAR is a remediation task. Understanding why the rule didn't fire is a program improvement.

The 2024 OCC cease-and-desist order against Bank of America required both a Transaction Monitoring System Validation and Look-Back and a Negotiable Instruments Look-Back, explicitly tied to systemic failures including misconfigured alert thresholds, insufficient investigative resources, and SAR filing deficiencies. The lookback wasn't just about finding missed activity — it was the mechanism for identifying what needed to change in the monitoring program itself.

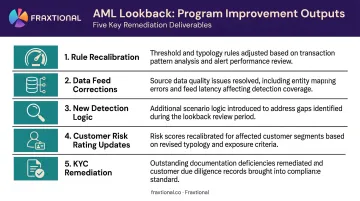

A well-scoped lookback feeds directly into:

- Rule recalibration — adjusting alert thresholds that were set too high or too low

- Data feed corrections — fixing source system errors that caused gaps in transaction populations

- New detection logic — adding rules for typologies the program wasn't designed to catch

- Customer risk rating updates — revising profiles based on activity patterns revealed during review

- KYC remediation — identifying accounts where documentation was incomplete or outdated

Fixing these gaps proactively is far cheaper than responding to the next enforcement cycle or conducting a second lookback because the first one was too narrow.

What this improves:

- False negative rate

- Alert volume per analyst

- System coverage rate

- Rule effectiveness score

- Customer risk rating accuracy

Most relevant when: Following system upgrades or platform migrations; after M&A where inherited AML infrastructure is untested; when expanding into higher-risk product categories.

Demonstrating Regulatory Credibility and Institutional Good Faith

Improving your monitoring program is only half the equation. Regulators — whether FinCEN, the FCA, FINTRAC, or EU national competent authorities — also evaluate how an institution responds once gaps are discovered, not just whether violations occurred.

FinCEN's enforcement statement and the OCC's revised civil money penalties policy (effective January 2023) both treat self-identification, timely disclosure, and quality of remediation as mitigating factors. FINTRAC actively encourages voluntary self-declarations of non-compliance, having reviewed 287 such declarations in 2024–25.

The FCA gave Santander UK a 30% penalty reduction for early settlement cooperation, reducing its fine from £153.99 million to £107.79 million.

Independence is a recurring requirement in consent orders. The Anchorage Digital Bank, TD Bank, Binance, and Bank of America orders all required independent consultants or monitors for SAR lookback and transaction monitoring review processes.

A lookback without demonstrable independence is unlikely to satisfy regulatory expectations, regardless of technical quality.

For fintechs and crypto firms, this extends beyond enforcement. Sponsor banks and institutional investors evaluate AML posture directly. Demonstrating that your program has been pressure-tested — with gaps identified and addressed proactively — changes the conversation in due diligence.

One fintech that worked with Fraxtional noted their sponsor bank required a named BSA Officer and an AML framework review before onboarding; having fractional leadership in place accelerated the process considerably.

KPIs directly affected:

- Regulatory examination outcomes

- Consent order resolution timelines

- Banking partner retention rate

- License application success rate

What Triggers an AML Lookback?

Lookbacks arise from three distinct categories of triggers — and which category applies shapes both the urgency and the scope of the review.

Regulatory triggers are the most common and least flexible:

- Enforcement actions and consent orders issued by FinCEN, OCC, FCA, or FINTRAC

- SAR-related investigations that reveal systemic monitoring failures

- Examination findings where monitoring gaps are formally documented

Real examples include M.Y. Safra Bank (2020), Anchorage Digital Bank (2022), Binance (2023), TD Bank (2024), Bank of America (2024), and Patriot Bank (2025) — all with explicitly mandated lookback requirements tied to BSA/AML program deficiencies.

Business-driven triggers are equally common in high-growth environments and include:

- Discovery of transaction monitoring system failures or configuration errors

- Mergers and acquisitions requiring assessment of the acquired entity's compliance history

- Expansion into new products, services, or higher-risk geographies

- Sponsor bank onboarding requirements that surface historical monitoring questions

Fraxtional has been engaged specifically for sponsor bank onboarding scenarios where banks required a credible historical compliance review before approving a partnership. This is a pattern common among early-stage fintechs that scaled quickly before formalizing their AML infrastructure.

Internal triggers can also initiate a review:

- Whistleblower reports or internal ethics disclosures

- Internal audit findings identifying monitoring or reporting gaps

- Proactive compliance reviews initiated by leadership

Voluntary lookbacks initiated before regulatory intervention are viewed more favorably. FINTRAC's voluntary self-declaration program exists precisely because regulators prefer institutions that surface problems themselves.

What Happens When Lookbacks Are Ignored or Mismanaged

The consequences fall into three categories, each compounding the others.

Each category creates direct, measurable exposure:

- Regulatory: A poorly scoped, underdocumented, or non-independent lookback doesn't satisfy the original order — it creates a new one. Regulators revisit lookback quality in subsequent examinations, and enforcement action can escalate accordingly.

- Operational: Without a lookback following a monitoring failure, the institution keeps operating with the same blind spots. SAR obligations accumulate unfiled, customer risk profiles go uncorrected, and missed activity stays missed.

- Financial: Reactive, disorganized lookbacks take longer and consume more resources. The absence of a documented remediation plan at the end is itself a red flag — it signals the institution understood what it found but chose not to act on it.

TD Bank illustrates the operational cost directly. Its monitoring failures spanned nearly a decade; three separate money laundering networks moved over $670 million through its accounts during that period.

The pattern is consistent across TD Bank, Coinbase Europe, Santander UK, and Bank of America: in every case, delayed or incomplete remediation of monitoring failures drove up both the financial penalty and the breadth of required corrective action.

How to Get the Most Value from an AML Lookback

A lookback executed well produces more than SAR filings. It produces a clearer AML program. A few principles that separate effective lookbacks from ineffective ones:

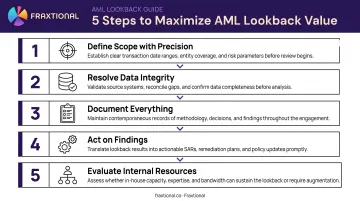

1. Define scope with precision. Scope that is too narrow misses the actual gap; too broad generates unmanageable data volumes. Tie scope to the specific trigger, make it risk-based, and agree on it with regulators before analysis begins. Anchorage's 2022 OCC order made scope and timeframe subject to regulator approval — a reminder that these conversations happen first, not after.

2. Resolve data integrity before analysis starts. Confirm that transaction monitoring systems, KYC records, case management platforms, and customer risk ratings are all accessible and complete. Data gaps found mid-lookback cause delays and re-work — and unreliable output that can undermine the entire exercise.

3. Document everything in a regulator-auditable format. Scope definition, data extraction methodology, alert logic, investigation decisions, and SAR/no-SAR determinations all need a paper trail a regulator can follow. A technically sound lookback without documentation is still a failed one.

4. Act on the findings, not just the report. The output of a lookback should directly feed into monitoring rule updates, policy revisions, and staff training. Institutions that file the report and move on without implementing changes are likely to see the same findings in their next examination cycle.

5. Evaluate whether internal resources are sufficient. Many fintechs, crypto firms, and early-stage institutions don't have a dedicated BSA Officer or MLRO-level resource to lead a credible lookback. For a first-time or regulator-mandated review, a senior named officer who can own scope, manage regulator communication, and produce audit-ready documentation isn't optional — it's what determines whether the outcome holds up to scrutiny. Firms like Fraxtional provide that director-level AML leadership on a fractional basis, serving as named BSA Officer, MLRO, or CAMLO without a full-time hire.

Done right, a lookback closes the gap that triggered it and positions the AML program to withstand the next examination cycle.

Conclusion

An AML lookback is one of the most revealing compliance exercises an institution can undertake. It exposes what routine monitoring actually missed: gaps in alert logic, KYC deficiencies, unmonitored transaction populations, and SAR filing failures that accumulated over time.

The value compounds when findings are acted upon. Institutions that treat a lookback as a one-time event miss the monitoring improvements it unlocks.

Those that embed lookback insights into ongoing program management build progressively stronger defenses. Over time, that discipline shows up in audit results, regulatory examinations, and the credibility of the compliance program itself — not just in a remediation file that gets closed and forgotten.

Frequently Asked Questions

What is a lookback in AML?

An AML lookback is a retrospective review of historical transaction data conducted to identify suspicious activity, KYC failures, or monitoring gaps that were not detected during routine oversight. It is typically triggered by regulators, internal audits, or system failures, and can span months to years of historical data.

What triggers an AML lookback review?

Common triggers include:

- Regulatory enforcement actions or consent orders

- Transaction monitoring system failures

- Internal audit findings

- Mergers and acquisitions

- Voluntary proactive compliance reviews

Sponsor bank onboarding requirements can also prompt historical compliance reviews for early-stage firms.

How far back do AML lookback reviews typically go?

The review window is determined by when the compliance gap began and when it was resolved — there is no universal fixed period. In practice, this has ranged from several months to nearly a decade. TD Bank's lookback obligation, for example, covered failures spanning 2014 to 2023.

Does an AML lookback require an independent third party?

Regulators consistently require or strongly prefer that mandated lookbacks be conducted or overseen by an independent third party. Institutions may conduct voluntary internal lookbacks, but regulator-mandated reviews almost always require demonstrated independence from those being reviewed.

What are the expected outcomes of a successful AML lookback?

Key deliverables include:

- Identification and filing of previously missed SARs

- A documented findings report

- A remediation plan addressing monitoring and control gaps

- Specific improvements to the AML program

Regulators expect findings to result in measurable program changes, not just documentation.

How does an AML lookback differ from routine transaction monitoring?

Routine transaction monitoring is prospective — it flags activity as it occurs. A lookback is retrospective, analyzing historical data to find what monitoring failed to catch. They are complementary rather than substitutes, and a well-executed lookback typically informs improvements to the ongoing monitoring program.