KYC remediation is the periodic process of reviewing, updating, and correcting existing customer due diligence records to ensure they remain accurate and compliant with current regulatory requirements. It matters to fintechs, crypto firms, banks, money transmitters, and embedded finance companies operating in the US, UK, Canada, and EU — anywhere that stale or incomplete customer data can attract enforcement action.

This article covers what KYC remediation is, what triggers it, how the process works step by step, what affects its scope, and where teams most commonly go wrong.

Key Takeaways

- KYC remediation is a structured review and correction of existing customer records — not a substitute for ongoing monitoring, which tracks behavior but doesn't fix stale or deficient records.

- Triggers include regulatory enforcement actions, internal audit findings, framework changes, M&A activity, and data discrepancies — each requiring a different response scope.

- Effective remediation follows a fixed sequence: scope → risk-tier prioritization → data collection → re-verification → documentation and monitoring feedback.

- The most costly mistake is documenting outcomes without documenting methodology — regulators will ask how you decided what to review, not just what you found.

What Is KYC Remediation?

KYC remediation is the systematic audit and re-verification of an existing customer base, conducted when prior verification is incomplete, outdated, or non-compliant with current standards. Unlike initial onboarding KYC, which screens a customer before they're admitted, remediation is retrospective.

It looks backward at records already in the system and brings them into alignment with what regulators require today.

The goal is concrete: close the gap between what regulators now require and what the firm's records actually contain.

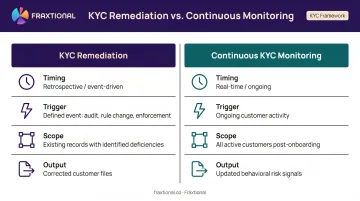

How it differs from continuous KYC monitoring:

| KYC Remediation | Continuous KYC Monitoring | |

|---|---|---|

| Timing | Retrospective, event-driven | Real-time, ongoing |

| Trigger | Defined event (audit, rule change, enforcement) | Ongoing customer activity |

| Scope | Existing records with identified deficiencies | All active customers post-onboarding |

| Output | Corrected customer files | Updated behavioral risk signals |

Continuous monitoring catches anomalies in customer behavior. It does not correct deficiencies in identity records, risk classifications, or source-of-funds documentation. Both serve a role — understanding which applies to your situation is where remediation planning begins.

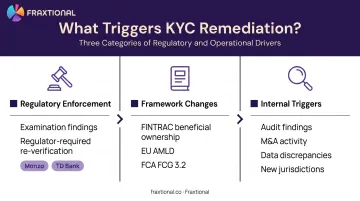

What Triggers KYC Remediation?

Three categories of triggers drive most remediation programs.

Regulatory Enforcement

The clearest trigger: a regulator identifies KYC deficiencies during an examination and requires the institution to conduct systematic re-verification.

The Monzo FCA Final Notice (July 2025) is one of the clearest recent examples. The FCA found that Monzo's CDD processes failed to incorporate reviews of existing customer records and lacked defined standards for when EDD documentation needed to be recorded. The remedy included a Skilled Person review, quality assurance over impacted customer files, and a mandatory back-book remediation exercise.

In the US, TD Bank's 2024 OCC consent order required a SAR look-back consultant specifically to facilitate updating due diligence information for existing moderate- and high-risk customers. Both cases illustrate what enforcement-triggered remediation looks like in practice.

Regulatory Framework Changes

When rules evolve, existing records that met the previous standard may fall short of the new one. Key examples:

- FINTRAC beneficial ownership (effective October 1, 2025): Reporting entities must now consult Corporations Canada's database for CBCA corporations and keep beneficial ownership records current.

- EU AMLD framework: Requires CDD to be applied to existing customers at appropriate times on a risk-sensitive basis, including when relevant circumstances change.

- FCA FCG 3.2: Firms must keep CDD documents up to date and demonstrate EDD measures commensurate with risk.

Internal Triggers

Not all remediation originates from a regulator. Internal grounds include:

- Internal audits or risk assessments surfacing data gaps

- M&A activity, where an acquiring firm re-verifies the acquired customer base

- Discovered data discrepancies — for example, a customer's second account shows different identifying information from the first

- A firm expanding into a new jurisdiction and finding existing records don't meet the new regulatory requirements

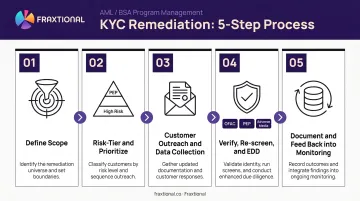

The KYC Remediation Process: Step by Step

Remediation follows a structured, sequential flow. Skipping or compressing any stage creates the risk of incomplete remediation , and incomplete remediation can itself become a regulatory finding.

Step 1: Identify the Triggering Event and Define Scope

Start by documenting what triggered the remediation and use that to define which customer segments are in scope. Automated database queries are essential here — filtering by account type, risk tier, jurisdiction, onboarding date, or missing data fields allows teams to identify impacted accounts at scale rather than manually reviewing records one by one.

The scope definition should be specific enough to defend to a regulator. Vague scope ("all customers") often leads to under-resourcing and extended timelines. Tight, justified scope ("all business accounts onboarded before the beneficial ownership rule change, in jurisdictions X, Y, Z") allows for realistic resourcing.

Step 2: Risk-Tier and Prioritize Affected Accounts

Not all customers require the same urgency or depth. The risk-based approach:

- Prioritize PEPs, customers in high-risk jurisdictions, and complex ownership structures first — these require Enhanced Due Diligence

- Re-verify standard-risk customers with a document refresh

- Apply simplified updates for low-risk customers where rules permit

Regulators expect a documented prioritization rationale. Stating that high-risk customers were addressed first — and explaining the criteria used to classify them — is part of the audit trail, not an optional extra.

Step 3: Customer Outreach and Data Collection

Firms typically notify affected customers via email, in-app notification, or formal letter. What's requested depends on the deficiency:

- Updated proof of identity or address

- Source of funds or source of wealth documentation

- Beneficial ownership information for corporate entities

- Confirmation of business purpose or relationship nature

Set clear deadlines with stated consequences. Customers who don't respond within the timeframe should face defined escalation — typically account restriction, followed by closure. Digital self-service collection tools reduce manual burden and improve completion rates, particularly for retail customers.

Step 4: Verification, Risk Reassessment, and EDD Where Required

Once documents are received, verify them against authoritative sources and re-screen each customer against:

- Sanctions lists (OFAC, OFSI, EU consolidated list)

- PEP databases

- Adverse media

Then reassess each customer's risk rating based on the updated profile. For higher-risk customers, this step often involves fuller EDD.

If remediation uncovers previously unidentified red flags, standard SAR/STR filing obligations apply. FinCEN requires filing within 30 calendar days of initial detection; FINTRAC requires submission "as soon as practicable" after reasonable grounds to suspect are established.

Step 5: Documentation, Record Updates, and Ongoing Monitoring

Regulators scrutinize this step — and enforcement records confirm the cost of getting it wrong. The Barclays FCA Final Notice (July 2025, £39.31 million) specifically cited KYC-file evidence gaps — the file didn't document the outcomes of further information requests.

Documentation requirements:

- Record what was requested, when, and what was received

- Document the methodology used for prioritization and re-verification

- Record what happened to non-responsive accounts (restrictions, closures, and rationale)

- Retain records in line with applicable rules — BSA and FINTRAC generally require five years from account closure; EU AMLD requires five years from relationship end

For dormant or closed accounts, deletion decisions require care. GDPR and UK GDPR erasure rights are real, but Article 17(3)(b) limits erasure where processing is necessary to comply with a legal obligation. AML retention obligations often supply that basis.

Finally, feed remediation outcomes back into ongoing monitoring. Updated risk profiles should inform transaction monitoring thresholds and periodic review schedules going forward.

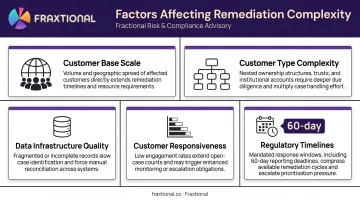

Key Factors That Affect KYC Remediation

Several variables determine how complex and resource-intensive a remediation program will be:

- Scale of the customer base: Larger, more geographically diverse customer books take longer and require more resources. Cross-border operations face layered jurisdictional requirements running simultaneously.

- Complexity of customer types: Individual retail customers are straightforward to remediate. Corporate entities with layered beneficial ownership, trusts, or shell structures require verification at each layer — each one its own workstream.

- Quality of existing data infrastructure: Firms without centralized, structured customer data face significant additional effort just to scope the impacted population before remediation can begin.

- Regulatory timelines: Regulator-mandated remediation comes with defined deadlines. Customers Bank, for example, had 60 days to submit a revised BSA/AML program to the Federal Reserve following its 2024 written agreement — firms need to honestly assess whether internal capacity can meet that deadline.

- Customer responsiveness: Response rates vary significantly by segment. Low engagement extends timelines and requires structured escalation protocols to avoid the program stalling.

For early-stage fintechs and crypto firms without a full-time CCO or BSA Officer, the regulatory timeline factor is particularly acute. Outside help is often the only realistic path to meeting a regulator's deadline without pulling resources from core operations.

Fractional compliance leadership addresses this directly. Fraxtional's Fractional CCO, BSA Officer, and CAMLO services give firms director-level oversight to design, manage, and document a remediation program — without the cost of a permanent hire.

Common Mistakes in KYC Remediation

Treating It as a One-Time Clean-Up

The most common misconception: that once the immediate trigger is addressed, remediation is done. A remediation program requires ongoing structure to stick. Without it, the same deficiencies tend to re-emerge — and the next examination finds the same gaps.

A defensible program needs at minimum:

- Governance and ownership (who is accountable for outcomes)

- Escalation paths for unresolved or non-responsive accounts

- Quality assurance reviews throughout (not just at close)

- A feedback loop that updates the ongoing KYC framework

Applying a Uniform Process Regardless of Risk

Moving quickly through a large customer base by applying the same lightweight re-verification to every account is a documented failure pattern. Regulators specifically examine whether remediation applied appropriate risk differentiation.

High-risk accounts — PEPs, complex corporate structures, customers in higher-risk jurisdictions — require materially more intensive EDD. A fast, uniform process that treats a retail customer and a corporate PEP the same will draw scrutiny.

Documenting Outcomes but Not Process

Compliance teams often focus on completing the data updates and overlook the audit trail behind how decisions were made. Monzo's FCA notice explicitly faulted the lack of clear EDD documentation standards. Barclays' notice cited KYC files that didn't evidence what happened after further information was requested.

If a regulator examines the remediation, they will ask:

- How were accounts prioritized?

- What methodology was used for re-verification?

- What happened to accounts whose owners didn't respond?

- Why were certain risk ratings assigned?

A well-executed remediation with poor documentation can still produce adverse findings. Treat the audit trail as a core deliverable — not something assembled after the fact.

Conclusion

KYC remediation is a structured, event-driven process that corrects historical gaps in customer due diligence records. Executed properly, it reduces enforcement risk and gives regulators evidence that compliance is actively managed — not just reactive. Treated as a one-time data-cleaning exercise without governance or documentation, it creates its own regulatory exposure.

For fintechs, crypto firms, and financial institutions building or scaling their compliance programs, Fraxtional's fractional CCO, BSA Officer, and CAMLO services provide the director-level expertise to design and execute KYC remediation programs end to end.

The engagement doesn't require a full-time hire. Fraxtional's directors embed with client teams, take direct ownership of the workstream, and deliver audit-ready documentation that holds up under regulatory scrutiny.

Frequently Asked Questions

What does KYC remediation mean?

KYC remediation is the process of reviewing and updating existing customer due diligence records to correct gaps, outdated information, or non-compliance with current regulatory standards. Unlike the initial onboarding KYC process, remediation is retrospective — it addresses deficiencies in records already in the system.

What are the 5 stages of KYC?

The core KYC lifecycle stages are: (1) customer identification and verification, (2) customer due diligence (CDD), (3) enhanced due diligence (EDD) for higher-risk customers, (4) ongoing monitoring, and (5) periodic review and remediation. Remediation sits within that final stage, triggered when existing records no longer meet current standards.

What triggers KYC remediation?

The main triggers are regulatory findings or enforcement actions, changes in AML/KYC regulations that raise verification standards, internal audit discoveries, business changes such as M&A activity, and identified discrepancies in existing customer data.

How long does KYC remediation typically take?

Timelines vary widely based on scope and complexity. Simple documentation updates for a small customer base may be completed in weeks. Comprehensive re-verification of a large or complex book — particularly when regulator-mandated — can run for several months to over a year.

What is the difference between KYC remediation and continuous KYC monitoring?

Continuous KYC monitoring is an embedded, real-time process tracking customer behavior and transactions after onboarding. KYC remediation is a retrospective, event-driven program that corrects historical deficiencies in existing customer records. Both are necessary, but monitoring cannot substitute for remediation. Monitoring flags behavioral anomalies; it does not fix underlying record gaps.

Can customers refuse to participate in KYC remediation?

Financial institutions generally have both contractual and regulatory grounds to require updated KYC information. Customers who don't respond within the required timeframe typically face account restrictions or closure. Firms should document the full escalation process — deadlines communicated, notices sent, and actions taken for non-responsive accounts.