Introduction

Fintech companies, crypto platforms, and money transmitters expanding into new states must navigate 50+ unique licensing frameworks with no federal standard to simplify the process. Every state draws its own regulatory line—different definitions of what triggers a license, different capital thresholds, different renewal timelines, different enforcement approaches.

That fragmentation shapes where you can operate, when you can launch, and whether your sponsor bank partnership holds up under due diligence.

The operational costs compound quickly. Common failure points include:

- Missed renewal deadlines that suspend your license mid-quarter

- Separate compliance frameworks required for each state (California's requirements bear little resemblance to Montana's)

- Enforcement actions triggered when a product crosses a threshold you didn't know existed

- Legislative changes that redefine your obligations overnight across multiple jurisdictions

For companies without a full-time compliance team, tracking staggered deadlines across dozens of states while monitoring regulatory shifts is a constant drain.

This guide covers the license types that matter most for financial services companies, the compliance pitfalls that trigger enforcement actions, the consequences of operating unlicensed (including retroactive disgorgement), and the practical steps to stay current across every state where you do business.

TLDR:

- Most U.S. states require separate money transmitter licenses (MTLs) for payment services, with Montana being the explicit exception

- FinCEN MSB registration is mandatory but does not replace state MTLs—you need both

- Anchor states like California, New York, and Texas impose high capital and bonding requirements ($250,000–$7,000,000 bonds)

- Crypto firms face dual obligations: standard MTLs plus state-specific virtual currency licenses like New York's BitLicense and California's DFAL

- Operating unlicensed triggers cease-and-desist orders, civil penalties, and retroactive disgorgement of all fees collected during the unlicensed period

What Multi-State License Compliance Means for Financial Services Companies

Multi-state license compliance is the obligation for fintechs, money transmitters, lenders, crypto firms, and embedded finance companies to obtain, maintain, and renew the correct state-level licenses in every jurisdiction where they conduct regulated activity—separate from federal registrations like FinCEN MSB registration.

Unlike healthcare's interstate compacts, financial services licensing is a state-by-state process with no meaningful uniformity. Each state's banking department or financial regulator sets its own definitions of what triggers a licensing requirement, what the application entails, what ongoing reporting is required, and what constitutes a violation.

The divergence is significant in practice. California's Department of Financial Protection and Innovation (DFPI), Texas's Department of Banking (DOB), and New York's Department of Financial Services (DFS) each define money transmission differently—meaning the same product can require three separate license types, three separate applications, and three separate compliance programs.

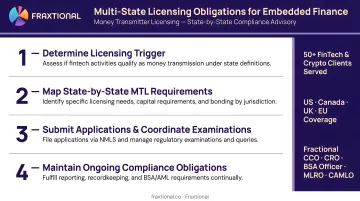

When Licensing Obligations Trigger

A company becomes subject to multi-state licensing when it processes transactions for customers in a given state, offers lending, issues stored value, or facilitates payment services to residents of that state—even if the company is headquartered elsewhere. New York explicitly states that serving New York residents creates a licensing nexus regardless of physical presence.

The nexus standard varies considerably across states and is one of the most common sources of compliance gaps:

- Some states require a license after a single transaction with a resident

- Others set transaction volume or dollar thresholds before licensing kicks in

- A handful apply nexus based on solicitation alone, regardless of completed transactions

Mapping these triggers before entering a new state matters. Operating unlicensed during even a brief pilot can expose a company to retroactive liability once regulators identify the gap.

Key License Types Financial Companies Must Manage Across States

Money Transmitter Licenses (MTLs)

Almost all U.S. jurisdictions require a state-level MTL for entities transmitting funds, with Montana being the explicit outlier stating it "does not regulate money transmitters." Requirements differ drastically across states:

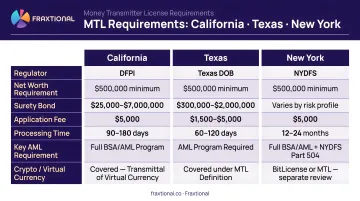

| State | Application Fee | Surety Bond Requirement | Net Worth / Capital Threshold |

|---|---|---|---|

| California (DFPI) | $5,000 | $250,000 to $7,000,000 for receiving money for transmission | Minimum tangible shareholders' equity of $500,000 |

| Texas (DOB) | $10,000 | $100,000 to $500,000 based on average daily money transmission liability | Tiered based on total assets (e.g., greater of $100,000 or 3% of assets for entities under $100M) |

| New York (NYDFS) | $3,000 | Minimum $500,000 determined case-by-case by the superintendent | Case-by-case determination |

New York, California, and Texas are commonly cited as having the most onerous MTL requirements, with rigorous application processes, substantial capital requirements, and intensive ongoing examination expectations.

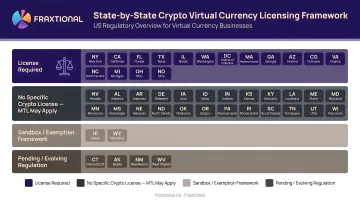

Cryptocurrency and Virtual Currency Licenses

On top of MTLs, crypto firms must navigate state-specific virtual currency licensing. New York's BitLicense (23 NYCRR Part 200) is the most stringent and widely referenced example, requiring a $5,000 application fee, case-by-case capital determinations, and examinations at least every two calendar years.

California's Digital Financial Assets Law (DFAL) requires entities engaging in digital financial asset business activity to be licensed by July 1, 2026, and imposes specific limits on crypto kiosks (capping transactions at $1,000 per day per customer). Other states have enacted dedicated frameworks including Louisiana's Virtual Currency Business Act and Illinois's Digital Assets and Consumer Protection Act.

States without specific crypto licenses may still require a standard MTL for crypto activities involving sovereign currency exchange — creating regulatory ambiguity that demands jurisdiction-specific legal analysis before operating.

FinCEN MSB Registration vs. State MTLs

FinCEN requires each MSB to register within 180 days of establishment, but this federal registration does not authorize a business to operate or exempt it from state money transmitter licensing. Companies registered as Money Services Businesses with FinCEN still must obtain individual state MTLs where required. Operating an unregistered MSB carries civil penalties of up to $5,000 per day.

NMLS and Multistate Licensing for Lending and Mortgage

The Nationwide Multistate Licensing System (NMLS) is the closest thing financial services has to a centralized multi-state licensing framework. As of December 31, 2024, 49 states, the District of Columbia, and Puerto Rico managed MSB licenses on NMLS.

NMLS provides a unified application platform and standardized reporting workflows — but it stops there. It does not supersede state laws, rules, regulations, or guidance related to seeking or maintaining licensure. State-specific fees, capital requirements, surety bonds, and continuing obligations remain fully intact.

Banking-Adjacent and Embedded Finance Licenses

Embedded finance companies and BaaS (Banking as a Service) platforms operating through sponsor bank partnerships may still require their own state licenses depending on the products offered and the degree of control they exercise over the financial product.

The Conference of State Bank Supervisors (CSBS) has consistently emphasized that a sponsor bank relationship does not transfer the bank's own charter privileges to the fintech partner — meaning embedded finance companies must independently assess their licensing exposure in each state where they operate or serve customers.