Introduction

In October 2024, TD Bank agreed to a $3.09 billion penalty for BSA/AML failures—the largest in U.S. banking history. The bank failed to monitor 92% of its transaction volume, allowing $670 million in money laundering to go unchecked.

Just months earlier, UK challenger banks Starling and Metro faced combined fines exceeding £45 million for weak financial crime controls.

These aren't outliers. In banking, compliance failures don't just result in fines—they destroy sponsor relationships, block funding rounds, and collapse reputations. For legacy banks, fintechs, and embedded finance companies alike, GRC is foundational to staying operational.

This guide covers what GRC means specifically in banking, the three core pillars, the risk categories institutions must manage, the regulatory frameworks governing U.S., UK, and EU markets, and practical steps for building a GRC program—whether you're a community bank, fintech startup, or crypto firm navigating sponsor bank due diligence.

Key Takeaways

- GRC integrates governance, risk management, and compliance to protect banks from operational, financial, legal, and reputational harm

- The three pillars must work in concert—not in silos—to prevent control gaps and diffused accountability

- Banks face seven core risk types: credit, market, operational, liquidity, legal, reputational, and strategic risk

- Regulatory obligations span the U.S. (Fed, OCC, FDIC, CFPB), UK (PRA, FCA), and EU (ECB)—each with distinct frameworks, from BSA/AML and Dodd-Frank to GDPR

- Strong GRC requires board-level ownership and experienced leadership—fractional compliance models provide that expertise without the cost of a full-time hire

What is GRC in Banking?

GRC—Governance, Risk, and Compliance—is a structured framework that aligns a bank's operations with strategic objectives, manages exposure to threats, and ensures adherence to laws, regulations, and ethical standards. Banking GRC differs from general corporate GRC in regulatory density and systemic economic role. Banks hold customer deposits, facilitate payments, extend credit, and interconnect with entire economies, and failures ripple well beyond individual institutions.

The 2023 collapses of Silicon Valley Bank, Signature Bank, and First Republic Bank demonstrated this. The Federal Reserve's post-mortem on SVB called it a "textbook case of mismanagement." Senior leadership failed to manage basic interest rate and liquidity risk. The board failed to oversee them. The result: a $212 billion institution collapsed in 48 hours, triggering contagion across regional banking.

The Silo Problem

GRC exists to solve a structural flaw: when governance, risk, and compliance operate separately, gaps emerge. Information doesn't flow. Controls overlap or contradict. Accountability diffuses.

A compliance team might flag rising AML alerts while risk management focuses on credit metrics and governance reviews capital adequacy, all without coordinated escalation to the board.

An integrated GRC approach creates a unified view of obligations, threats, and exposures. It connects:

- Capital adequacy (Basel requirements)

- Consumer protection (UDAAP, fair lending)

- Data privacy (GDPR, CCPA)

- AML/KYC (BSA, FATF standards)

- Fraud prevention (transaction monitoring, identity verification)

- Corporate governance (board oversight, executive accountability)

Each domain carries distinct regulatory frameworks and supervisory bodies. A bank operating across U.S. and UK jurisdictions must simultaneously satisfy Federal Reserve supervisory expectations, FCA conduct rules, and FATF anti-money laundering standards—coordination that demands centralized GRC orchestration.

The Strategic Benefit

Beyond compliance, mature GRC programs build trust with regulators, customers, and sponsor banks. For fintechs and embedded finance companies seeking banking partnerships, a documented GRC framework is often the difference between onboarding approval and rejection. Sponsor banks scrutinize AML policies, governance structures, and risk management maturity during due diligence; material gaps in any of these areas typically end the due diligence process before a term sheet is issued.

The Three Pillars of GRC in Banking

Governance

Governance in banking is the system of rules, processes, policies, and structures directing how an institution is managed and controlled. It encompasses board oversight, executive accountability, ethical standards, and decision-making transparency. Strong governance sets the "tone at the top" that cascades through all organizational levels.

Core Components:

- Board of Directors oversight: Sets strategic direction, approves risk appetite, and monitors regulatory compliance

- Clear lines of authority: Defines who owns decisions, escalations, and control failures

- Internal audit functions: Provides independent assurance on control effectiveness

- Whistleblower policies: Enables reporting of misconduct without retaliation

- Regular governance reviews: Assesses whether structures still fit the institution's size and complexity

Governance Failures in Practice:

Wells Fargo's 2018 Federal Reserve enforcement action imposed an unprecedented asset cap after finding the firm lacked an effective firm-wide risk management framework. The board failed to meet supervisory expectations, preventing proper escalation of compliance breakdowns tied to sales practices misconduct. The result: growth restriction still in effect years later.

Credit Suisse's 2023 collapse analysis by FINMA identified deficient corporate governance as a root cause: responsibilities weren't clearly defined, management culture was flawed, "tone from the top" was weak, and risk culture was poor. Governance failures compounded strategic missteps until the institution became unsalvageable.

Risk Management

Governance failures rarely exist in isolation — they almost always surface through breakdowns in the second pillar: risk management. This is the systematic process of identifying, assessing, prioritizing, and mitigating threats to financial health, operations, and reputation. Where governance sets the rules, risk management tests whether those rules hold up against reality.

The Risk Management Lifecycle:

- Identify threats through scenario analysis, stress testing, and risk registers

- Assess each threat by evaluating both its likelihood and potential financial impact

- Mitigate through controls, hedging strategies, lending standards, and operational safeguards

- Monitor continuously using Key Risk Indicators (KRIs) tracked against defined thresholds

The Chief Risk Officer (CRO) and Operational Risk Manager execute this process, reporting directly to the board. The OCC's Corporate and Risk Governance handbook emphasizes that the board must oversee development and review of risk appetite, hold senior management accountable, and maintain effective internal controls.

Forward-Looking Risk Management:

Banks use stress testing to model losses under adverse scenarios: recession, interest rate spikes, sudden liquidity withdrawals. SVB and First Republic failed because they didn't adequately stress-test interest rate risk exposure. When rates rose sharply in 2022-2023, their bond portfolios cratered and depositors fled. Both outcomes were predictable with proper scenario analysis in place.

Compliance

Compliance ensures the institution adheres to all applicable laws, regulations, standards, and internal policies. This spans AML/BSA, KYC, consumer protection (UDAAP), data privacy (GDPR, CCPA), Reg E (electronic funds transfer), and fair lending regulations. New rules, updated guidance, and enforcement priorities mean compliance programs need continuous maintenance — not just a one-time build.

Elements of a Robust Compliance Program:

- Written policies and procedures reflecting current regulatory requirements

- Designated compliance officers: CCO, BSA Officer, CAMLO/MLRO for international operations

- Transaction monitoring systems detecting suspicious activity in real time

- Staff training and awareness programs embedding compliance into daily decision-making

- Regulatory change tracking ensuring policies update as rules evolve

- Regular internal audits testing control effectiveness

The Cost of Non-Compliance:

Starling Bank's £28.9 million FCA fine in 2024 came after the bank opened 54,359 accounts for high-risk customers in direct breach of a regulatory requirement. The FCA found systemic financial crime control failures and weak sanctions screening. The penalty represented only one consequence — the reputational damage and regulatory scrutiny will persist for years.

Metro Bank's £16.6 million fine stemmed from failing to adequately monitor over 60 million transactions for money laundering risks. In both cases, the compliance program didn't scale alongside the business — and regulators noticed before the institutions did.

Key Risk Types Banks Must Manage

Banking institutions face a broad, interconnected risk universe. Categorizing risk types enables targeted controls—credit risk demands different mitigation than cyber risk. The Basel Framework recognizes multiple distinct categories requiring separate management strategies.

Financial Risks

Credit Risk: The potential that a borrower or counterparty fails to meet obligations. Banks mitigate credit risk through:

- Underwriting standards and credit scoring models

- Collateral requirements

- Capital reserves tied to Basel exposure calculations

Market Risk: When SVB collapsed, rising interest rates had devalued its securities portfolio by $15 billion — erasing capital and triggering depositor panic. That's market risk in its most visible form: losses driven by movements in interest rates, foreign exchange, or asset prices.

Liquidity Risk: Inability to meet short-term obligations without incurring unacceptable losses. First Republic's failure resulted from rapid growth, overreliance on uninsured deposits, and failure to sufficiently mitigate interest rate risk—when deposits fled, the bank couldn't replace funding fast enough.

Operational, Legal, and Compliance Risks

Operational Risk: Losses from failed internal processes, systems, or human error—including fraud and cyber incidents. The Basel III framework defines operational risk as excluding strategic and reputational risk but including legal risk.

Legal Risk: Exposure to lawsuits, contract disputes, or regulatory enforcement actions. Deutsche Bank's $186 million Federal Reserve fine for deficient AML internal controls relating to Danske Bank's Estonian branch illustrates legal risk materialization.

Compliance Risk: The Basel Committee defines this as the risk of legal or regulatory sanctions, financial loss, or reputational damage from failing to comply with laws, regulations, and standards of good practice. In banking, BSA/AML failures are the most common trigger — resulting in consent orders, civil money penalties, and enhanced supervisory scrutiny.

Reputational and Strategic Risks

Reputational Risk: Damage to brand trust from misconduct, data breaches, or regulatory failures. A World Economic Forum study found that reputation accounts for over 25% of a company's market value. Research on data breaches shows cumulative abnormal returns of -0.6% on announcement day.

Strategic Risk: Failure to adapt to market disruptions—fintech competition, digital banking shifts, crypto asset classes. Wells Fargo's prolonged asset cap represents strategic risk materialization: the underlying governance failure occurred years ago, yet the asset cap limiting its growth persists.

The Regulatory Compliance Landscape for Banks

Regulatory Bodies

Banks operating across borders manage multi-jurisdictional compliance obligations simultaneously:

United States:

- Federal Reserve: Promotes safety and soundness of individual institutions and monitors systemic impact

- OCC: Charters, regulates, and supervises national banks and federal savings associations

- FDIC: Insures deposits, examines institutions, resolves failed banks

- CFPB: Protects consumers from unfair, deceptive, or abusive practices

United Kingdom:

- PRA: Prudential regulation and supervision of banks, insurers, major investment firms

- FCA: Financial conduct regulator focused on consumer protection, market integrity, competition

European Union:

- ECB (SSM): Single Supervisory Mechanism setting supervisory priorities for European banking

Global:

- FATF: Sets international standards for anti-money laundering, terrorist financing, proliferation financing

Key Regulatory Frameworks

BSA/AML: Bank Secrecy Act and anti-money laundering requirements mandate transaction monitoring, suspicious activity reporting (SARs), and KYC/Customer Due Diligence. FinCEN's national AML/CFT priorities include corruption, cybercrime, terrorist financing, fraud, transnational crime, drug trafficking, human trafficking, and proliferation financing.

KYC/CDD: Know Your Customer and Customer Due Diligence requirements force banks to verify customer identities, understand business relationships, and assess money laundering risk before onboarding.

Dodd-Frank Act: U.S. financial reform legislation following 2008, establishing stricter capital requirements, stress testing, and consumer protection rules.

UDAAP: Unfair, Deceptive, or Abusive Acts or Practices—CFPB authority to penalize banks for practices that harm consumers.

Reg E: Electronic Fund Transfer Act regulation protecting consumers in electronic banking transactions.

GDPR/Data Privacy: EU General Data Protection Regulation and equivalents (CCPA in California) governing personal data handling.

The Escalating Compliance Burden

PwC's Global Compliance Survey 2025 found 85% of respondents stated compliance requirements have become more complex in the last three years, and nearly 90% reported breadth of compliance responsibilities has increased.

The global cost of financial crime compliance reached $206.1 billion in 2023. Deloitte reports that operating costs spent on compliance have increased over 60% compared to pre-financial crisis levels.

Smaller banks and fintechs face disproportionate exposure. As regulations multiply and enforcement intensifies, institutions lacking dedicated compliance infrastructure struggle. This gap becomes critical during sponsor bank due diligence reviews, where banking partners require evidence of mature AML programs, designated BSA Officers, and board-level governance before approving partnerships.

Best Practices for Building an Effective GRC Framework

Foundational Implementation Steps

Conduct a comprehensive risk and compliance assessment to understand current gaps. Map existing controls against regulatory requirements (BSA/AML, UDAAP, data privacy), identify where controls don't exist or function poorly, and prioritize remediation by severity and regulatory exposure.

Define a GRC governance structure with clear ownership:

- Board: Sets risk appetite, approves policies, monitors performance

- C-suite: Executes strategy, allocates resources, escalates material issues

- Operational management: Implements controls, trains staff, conducts first-line monitoring

- First-line staff: Executes controls daily, reports exceptions

Align the GRC framework to strategic objectives rather than treating it as a checkbox exercise. GRC should enable business goals — faster sponsor bank onboarding, investor confidence, regulatory credibility — not just satisfy auditors.

Establish a cross-functional GRC committee with representation across risk, legal, compliance, operations, and technology. This breaks down silos and ensures coordinated responses to emerging threats.

Operational Best Practices

Develop written policies and procedures reflecting current regulatory requirements. Policies must be specific — generic templates fail sponsor bank reviews. Include transaction monitoring thresholds, SAR escalation workflows, KYC documentation standards, and data retention rules.

Establish regular internal audit cycles and control testing. Audit annually at minimum; high-risk areas like AML and fraud require quarterly reviews. Document findings, assign remediation owners, and track completion.

Implement ongoing staff training programs. Annual compliance training isn't sufficient. Embed compliance into daily decision-making through scenario-based learning, phishing simulations, transaction monitoring case studies, and escalation drills.

Track Key Risk Indicators (KRIs) and Key Performance Indicators (KPIs) consistently. Dashboards should give board-level visibility into GRC program health. Metrics worth monitoring include:

- SAR filing volume and escalation timelines

- Control test failure rates

- Regulatory exam findings and remediation status

- Customer complaint trends

- Cyber incident frequency

Compliance Culture from Leadership Down

Compliance culture lives or dies at the top. Strong governance requires:

- Board and senior executives modeling ethical behavior

- Empowering compliance staff to escalate concerns without retaliation

- Allocating adequate resources to GRC functions — budget, headcount, technology

- Engaging experienced fractional compliance leadership when a full-time CCO or CRO hire isn't feasible

For fintechs and embedded finance companies, this last point is often the most practical path forward. Firms like Fraxtional provide director-level GRC expertise on flexible engagement terms — giving emerging institutions experienced compliance leadership that satisfies sponsor bank requirements and builds investor confidence, without the cost of a full-time executive hire.

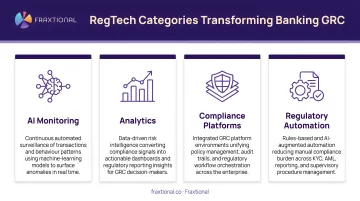

Technology and Expert Leadership in Banking GRC

How Technology Transforms GRC Execution

Four categories of technology are reshaping how banks and fintechs execute GRC programs:

- AI-powered transaction monitoring detects suspicious activity in real time. HSBC cut monitoring alerts by 60% while finding 2-4x more confirmed suspicious activity. McKinsey reports agentic AI for KYC and transaction monitoring can yield productivity gains of 200% to 2,000%.

- Automated regulatory change management tracks evolving requirements and maps them to internal controls—pushing Federal Register updates, FCA policy statements, and ECB supervisory expectations directly to compliance teams with implementation guidance.

- GRC platforms provide centralized dashboards of risk exposure, compliance status, and audit trails. Gartner projects effective AI governance tools could reduce regulatory expenses by 20%.

- Predictive analytics let institutions model risk scenarios before they materialize—stress testing interest rate shocks, deposit flight, or cyber breaches to help boards allocate capital accordingly.

The RegTech Market

Grand View Research estimates the global RegTech market will grow from $24.34 billion in 2025 to $112.10 billion by 2033, at a 21.1% CAGR. The primary drivers are AI and machine learning capabilities—specifically automated monitoring, real-time anomaly detection, and reduced manual review overhead.

That market growth reflects genuine demand—but scaling RegTech investment only pays off when experienced people are directing it.

The Critical Role of Experienced Compliance Leadership

Technology amplifies effectiveness. It doesn't replace judgment, regulatory relationships, or enforcement navigation.

Deloitte notes AI-based contract review tools can save 360,000 hours annually—equivalent to 170+ legal or compliance FTEs—but someone must still design controls, interpret alerts, and engage regulators.

Fractional compliance leadership—such as fractional CCO, CRO, BSA Officer, CAMLO, or MLRO services offered by firms like Fraxtional—provides access to director-level GRC expertise on flexible engagement models. For emerging institutions, that means:

- Meet compliance obligations without full-time executive cost

- Satisfy sponsor bank due diligence requirements

- Build investor confidence with credible governance

- Navigate pre-deal compliance reviews with experienced representation

For institutions undergoing sponsor bank onboarding or seeking banking partnerships, having a named, experienced BSA Officer or CCO representing the organization often makes the difference between approval and rejection.

Frequently Asked Questions

What is governance, risk, and compliance in banking?

GRC in banking is a structured framework integrating governance (how a bank is directed and controlled), risk management (identifying and mitigating threats), and compliance (adhering to laws and regulations). Together, they protect financial stability, customer interests, and institutional integrity.

What are the 4 components of GRC?

The three core pillars are Governance, Risk Management, and Compliance. A fourth component many programs include is Integration — the cross-functional approach that connects all three elements into a single coordinated program rather than siloed functions.

What is risk governance in banking?

Risk governance is the framework of policies, structures, and accountability mechanisms through which a bank defines its risk appetite and sets management objectives. Oversight responsibility typically falls to the Board and CRO, who monitor risk performance against defined thresholds.

What are the 7 types of risk in banking?

The commonly recognized types are credit risk, market risk, operational risk, liquidity risk, legal/compliance risk, reputational risk, and strategic risk. Each requires distinct monitoring tools and mitigation strategies within the bank's GRC framework.

What are the compliance risks in banking?

Compliance risks cover exposure to penalties across key regulatory areas: AML/BSA, KYC/CDD, UDAAP, data privacy, and fair lending. Failures in any of these areas can result in fines, license revocation, or lasting reputational damage.

What are the 5 key areas of compliance in banking?

The five most commonly cited areas are Anti-Money Laundering (AML) and Bank Secrecy Act compliance, Consumer Protection (including UDAAP and fair lending), Data Privacy and Cybersecurity, Capital and Prudential Standards, and Regulatory Reporting and Disclosure. Requirements apply across U.S. federal frameworks as well as international standards such as GDPR and FATF guidelines, depending on where the institution operates.