Introduction

Since the IRS classified cryptocurrency as property in 2014, a critical question has gone unanswered: do FATCA (Form 8938) or FBAR (FinCEN Form 114) reporting obligations apply to crypto held on foreign exchanges? No definitive guidance exists, leaving U.S. taxpayers, crypto firms operating internationally, and compliance professionals in a genuine regulatory gray zone.

That property classification is the root of the problem. FATCA and FBAR were built around conventional financial assets and foreign accounts — frameworks that don't map cleanly onto decentralized digital assets, creating real ambiguity about what must be reported and when.

This article breaks down both frameworks, explains what's currently required, what remains uncertain, and what steps U.S. taxpayers and crypto firms should take now to manage risk and maintain compliance.

Key Takeaways

- The IRS classifies cryptocurrency as property, leaving both FATCA and FBAR obligations unclear for crypto holders

- FATCA (Form 8938) likely applies to foreign crypto holdings above thresholds—no explicit IRS guidance exists, so report proactively

- FBAR currently excludes crypto-only foreign accounts (FinCEN Notice 2020-2), but hybrid accounts holding both crypto and fiat likely trigger filing

- FinCEN has signaled intent to amend FBAR rules to cover virtual currency—proactive compliance now reduces future exposure

- Penalties are steep: FATCA violations start at $10,000 (up to $50,000); willful FBAR violations reach $165,353 or 50% of account value

How the IRS Classifies Cryptocurrency for Tax Purposes

The IRS established in Notice 2014-21 that cryptocurrency is treated as property for federal income tax purposes—not as currency. This classification directly shapes how FATCA and FBAR rules apply to digital assets.

Because crypto is "property," it does not neatly fit the definitions of "financial accounts" or "specified foreign financial assets" that FATCA and FBAR were designed to capture—leaving neither framework with clear jurisdiction over virtual currency holdings.

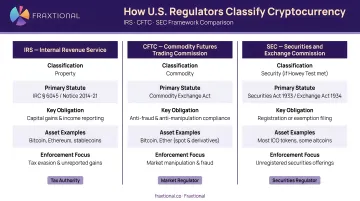

How three agencies currently classify cryptocurrency:

- IRS: Property (Notice 2014-21)

- CFTC: Commodity under the Commodity Exchange Act

- SEC: Securities when meeting the Howey investment-contract test

FATCA and FBAR use definitions anchored in tax law that don't clearly align with any of these classifications. For crypto firms and their compliance teams, that misalignment creates real exposure—reporting obligations remain unsettled even as enforcement activity increases.

Does FATCA Apply to Cryptocurrency?

Understanding FATCA's Scope

FATCA (Foreign Account Tax Compliance Act), enacted in 2010, requires U.S. taxpayers to report "specified foreign financial assets" on Form 8938 when aggregate values exceed applicable thresholds.

Current FATCA filing thresholds:

| Filer Status & Location | End of Year Threshold | Anytime During Year Threshold |

|---|---|---|

| Single / Married Filing Separately (U.S. residents) | $50,000 | $75,000 |

| Married Filing Jointly (U.S. residents) | $100,000 | $150,000 |

| Single / Married Filing Separately (living abroad) | $200,000 | $300,000 |

| Married Filing Jointly (living abroad) | $400,000 | $600,000 |

Source: IRS Form 8938 Instructions

The Definition Problem

IRC §6038D defines "specified foreign financial assets" as:

- Financial accounts maintained by a foreign financial institution

- Non-account foreign investment assets (foreign stocks, securities, contracts with non-U.S. persons, interests in foreign entities)

Virtual currency and cryptocurrency appear neither explicitly included nor explicitly excluded in these statutory definitions.

The FFI Question

The key unresolved issue: does a personal account on a foreign crypto exchange qualify as a "financial account" maintained by a "foreign financial institution" (FFI)?

Under 26 CFR §1.1471-5, FFIs fall into three categories: custodial institutions (holding financial assets for others), investment entities (conducting investment activities as a business), and depository institutions (accepting deposits in the ordinary course of banking). Centralized crypto exchanges could potentially qualify as custodial institutions — but only if cryptocurrency itself is deemed a "financial asset," which remains unsettled.

The Financial Asset Ambiguity

Under FATCA regulations, "financial assets" reference securities and commodities defined under IRC §475. The problem:

- Actively traded crypto could qualify as a commodity given established futures markets

- Bitcoin and Ether likely do not qualify as securities under current SEC guidance

- The IRS has not issued any ruling connecting IRC §475 definitions to FATCA's "specified foreign financial asset" framework

The Conservative Approach

Given that this legal ambiguity cuts both ways — crypto might be reportable, or it might not — the practical question for U.S. holders is where to set their default.

Tax professionals widely recommend erring on the side of disclosure: if you hold crypto on a foreign exchange and the value meets FATCA thresholds, file Form 8938. The AICPA reinforced this position in a 2018 comment letter, stating that virtual currencies should aggregate with fiat currencies for both FBAR and FATCA reporting when thresholds are met.

The cost of over-reporting is minimal. The cost of under-reporting — penalties that can reach $10,000 per violation or more — is not.

Does FBAR Apply to Cryptocurrency?

Current Legal Position

FBAR (Foreign Bank Account Reporting), filed via FinCEN Form 114, requires U.S. persons to report foreign financial accounts with an aggregate value exceeding $10,000 at any point during the calendar year. FBAR is administered by FinCEN (not the IRS) and is due by October 15 of the following year.

FinCEN Notice 2020-2 confirmed the current position clearly: existing FBAR regulations do not define a foreign account holding only virtual currency as a type of reportable account. This means a crypto-only foreign account is technically not required to be reported under current rules.

The Hybrid Account Exception

There is one important exception: if a foreign crypto account also holds fiat currency (USD, EUR, GBP, etc.) or other reportable assets alongside cryptocurrency, the entire account may already be reportable under FBAR. The presence of any traditional currency in the account likely triggers the reporting requirement.

Coming Regulatory Change

FinCEN Notice 2020-2 explicitly stated the agency intends to propose an amendment to include virtual currency as a reportable account type. While this rulemaking has not yet been finalized as of April 2026, rules could change with little warning.

Until the amendment takes effect, the current exclusion for crypto-only accounts remains. Taxpayers should monitor FinCEN announcements closely for updates.

Non-Custodial Wallets and DEXs

Non-custodial wallets and decentralized exchanges work differently under FBAR. The key distinctions:

- Non-custodial wallets: User holds private keys directly — no intermediary "account" exists, so FBAR likely does not apply

- Decentralized exchanges (DEXs): No third-party custodian means no reportable account under current rules

- Custodial foreign accounts: A third-party exchange holds the crypto on your behalf — this is where FBAR exposure actually lies

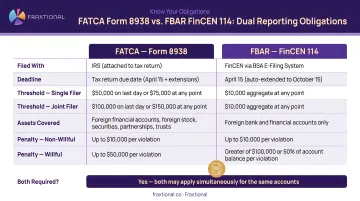

FATCA vs. FBAR: Key Differences Crypto Holders Must Know

| Feature | FATCA (Form 8938) | FBAR (FinCEN Form 114) |

|---|---|---|

| Administering Agency | IRS | FinCEN |

| Filing Method | Attached to annual tax return (Form 1040) | Filed separately via FinCEN BSA E-Filing System |

| Reporting Threshold (U.S. residents) | Starts at $50,000 (single filers) | $10,000 aggregate |

| Scope of Coverage | Broader: covers non-account foreign assets held for investment | Narrower: focuses on foreign financial accounts |

| Crypto-Only Accounts | Uncertain; conservative approach recommended | Currently not reportable per FinCEN Notice 2020-2 |

| Hybrid Accounts (crypto + fiat) | Likely reportable if thresholds met | Likely reportable |

These obligations are not mutually exclusive. The IRS explicitly states that filing Form 8938 does not relieve you of the requirement to file FBAR, and vice versa. Both may apply simultaneously to the same foreign crypto holdings.

Even when FBAR technically excludes a crypto-only account today, FATCA's broader "foreign financial asset" framework may still trigger a separate reporting obligation—which is why crypto holders need to evaluate both frameworks independently, not treat one exclusion as clearing them on all fronts.

Penalties, Risks, and What Crypto Holders and Firms Should Do Next

FATCA Penalties

Failure to file Form 8938 (IRC §6038D):

- Initial penalty: $10,000 upon IRS notification

- Escalation: Additional $10,000 for each 30-day period after 90 days, up to $50,000 maximum

- Statute of limitations: Failure to file keeps the statute open indefinitely until 3 years after the information is furnished

- Accuracy-related penalties: Increase from 20% to 40% for unreported foreign assets

Criminal exposure: Willful failure to file can trigger criminal penalties under 26 U.S.C. §7201 (tax evasion) and §7206 (fraud and false statements), carrying potential imprisonment.

FBAR Penalties

Civil penalties (31 U.S.C. §5321):

- Non-willful violations: Up to $16,536 per violation (2025 inflation-adjusted amount)

- Willful violations: Up to the greater of $165,353 or 50% of account value per violation

Criminal penalties (31 U.S.C. §5322):

- Willful violations: Up to $250,000 fine and 5 years imprisonment

- Pattern of illegal activity exceeding $100,000 in 12 months: Up to $500,000 and 10 years imprisonment

Recent enforcement: In December 2025, FinCEN assessed a $3.5 million penalty against Paxful, a peer-to-peer crypto platform, for willful BSA violations—a signal that FinCEN is treating crypto businesses with the same scrutiny as traditional financial institutions.

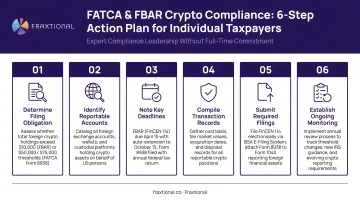

Action Steps for Individual Crypto Holders

- Identify every foreign exchange or custodial wallet where you hold crypto

- Determine whether any accounts are "hybrid" (holding fiat alongside crypto)

- Calculate aggregate maximum values during the tax year

- Apply the relevant FATCA and FBAR thresholds to determine reporting obligations

- File Form 8938 and/or FinCEN Form 114 conservatively when in doubt

- Consult a qualified tax professional for prior-year exposure and remediation options

Remediation programs available:

- Streamlined Filing Compliance Procedures: For non-willful failures

- IRS Criminal Investigation Voluntary Disclosure Practice: For willful failures seeking protection from prosecution

What Crypto Firms Need to Understand

Foreign crypto exchanges and custodial wallet providers may themselves qualify as FFIs under FATCA—creating their own reporting, withholding, and KYC/due diligence obligations toward U.S. account holders.

Compliance obligations for foreign crypto platforms:

- FATCA registration and reporting requirements

- Withholding tax obligations on U.S.-source payments

- Enhanced KYC and due diligence for U.S. account holders

- Potential classification as financial institutions under multiple jurisdictions

Managing these obligations across multiple jurisdictions is resource-intensive—particularly for growth-stage firms that don't yet need a full-time compliance executive. Fraxtional provides fractional BSA Officer, CCO, and CAMLO services, giving crypto firms and fintechs access to experienced compliance leadership on cross-border regulatory requirements, sponsor bank relationships, and evolving digital asset frameworks across the U.S., Canada, UK, and EU.

Frequently Asked Questions

What are the IRS rules for cryptocurrency?

The IRS classifies cryptocurrency as property under Notice 2014-21. Three core rules follow from that classification:

- Capital gains rules apply to sales and exchanges

- Ordinary income rules apply to crypto received as payment or mining rewards

- All taxable transactions must be reported on federal returns, even without a 1099

How long do I need to hold crypto to avoid higher taxes?

Crypto held more than one year qualifies for long-term capital gains rates, which are generally lower than ordinary income rates. Assets held one year or less are taxed as ordinary income at short-term rates. The holding period starts the day after acquisition.

What is the 30 day rule in crypto?

As of April 2026, the IRS wash-sale rule (which prohibits claiming a loss on a security sold and repurchased within 30 days) does not officially apply to cryptocurrency since crypto is classified as property, not a security. However, proposed legislation has sought to extend this rule to digital assets and you should confirm the current rule before filing.

Do I need to report cryptocurrency held on a foreign exchange on FBAR?

Under current FinCEN guidance (Notice 2020-2), a foreign account holding only cryptocurrency is not yet explicitly required to be reported on FBAR. However, hybrid accounts holding fiat currency alongside crypto likely are reportable, and FinCEN has signaled it intends to change this rule.

What is Form 8938 and when does it apply to crypto?

Form 8938 (FATCA reporting) is filed with your tax return to disclose specified foreign financial assets exceeding threshold values. While the IRS has not issued explicit guidance on foreign crypto accounts, the conservative approach is to report if thresholds are met — the cost of over-disclosure is far lower than the penalty risk of under-reporting.

What is a "hybrid" crypto account and why does it matter for FBAR?

A hybrid account is a foreign exchange account that holds both cryptocurrency and traditional fiat currency (USD, EUR, GBP, etc.). Because the fiat component qualifies as a reportable financial account, the entire account's value likely triggers FBAR obligations if the $10,000 aggregate threshold is exceeded.