Introduction

Financial crime risk assessment is cited in virtually every AML and compliance framework — FATF, FFIEC, FCA, EBA — yet the actual methodology behind it remains poorly understood at an operational level. Many firms have a risk assessment. Far fewer have one that would survive examiner scrutiny.

This article is written for compliance officers, BSA/AML teams, founders, and risk functions at fintech companies, banks, crypto firms, money transmitters, and embedded finance providers.

Whether you're building a methodology from scratch or defending an existing one, what follows is a clear, operational breakdown of how the process works: from inherent risk identification through residual risk calculation.

The stakes are real. FinCEN's 2022 consent order against USAA Federal Savings Bank included a $140 million civil penalty, with findings centered on a flawed customer risk score model that omitted expected activity as a risk factor. That outcome traced directly to methodology failure.

Key Takeaways

- A financial crime risk assessment methodology is how a firm identifies, scores, and manages exposure to money laundering, fraud, terrorist financing, and sanctions.

- The standard flow covers three phases: inherent risk → control assessment → residual risk.

- Risk is assessed across four categories: customer, geographic, product/transaction, and sector/delivery channel.

- FATF, FFIEC, and the FCA all require a documented, risk-based approach; firms without one face examination criticism and enforcement action.

- Treat it as a living document, not a one-time filing — it must stay current as the business evolves.

What Is Financial Crime Risk Assessment Methodology?

A financial crime risk assessment methodology is the documented, repeatable process a firm uses to:

- Identify its specific exposure to financial crime risks

- Evaluate the controls in place to mitigate those risks

- Determine what level of risk remains after those controls are applied

The output is a defensible, quantified view of the firm's inherent risk profile, its control environment, and its residual risk. That output then drives the compliance decisions that follow: resource allocation, enhanced due diligence thresholds, transaction monitoring calibration, and more.

It's also worth being clear about what the methodology is not:

- Compliance audit: An audit tests whether existing controls operate correctly. The methodology asks a prior question — whether the right controls exist at all.

- General enterprise risk assessment: Enterprise risk covers operational, strategic, and financial exposures well beyond financial crime scope.

- KYC process: KYC applies risk outputs to individual customers. The methodology builds the framework those outputs come from.

Firms that conflate these end up with controls calibrated to audit logic rather than actual risk exposure — passing reviews without managing the risks that matter.

Why Financial Services Firms Use This Methodology

The Regulatory Mandate

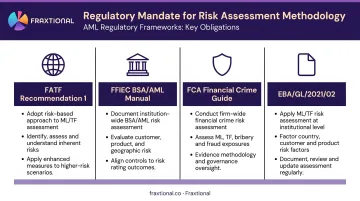

The obligation to maintain a documented, risk-based methodology isn't optional — it's woven into the foundational standards governing AML globally.

- FATF Recommendation 1 requires countries and financial institutions to identify, assess, understand, and mitigate ML/TF/PF risks — forming the basis for proportionate controls

- FFIEC BSA/AML Manual — with examiner guidance updated through 2026 — states that written documentation of the risk assessment is a sound practice, and examiners review whether institutions have adequately identified their illicit finance risks

- FCA Financial Crime Guide requires risk assessments to be comprehensive, continuous, proportionate, and regularly reviewed

- EBA/GL/2021/02 requires both business-wide and individual ML/TF risk assessments, with defined risk-factor categories

The enforcement record confirms this isn't theoretical. The FCA's 2023 Final Notice against Guaranty Trust Bank UK resulted in a £7.67 million fine, citing formulaic risk assessments, missing documented rationale, and default high-risk ratings applied without analysis. Starling Bank's 2024 fine of £28.95 million included findings that its financial sanctions risk assessment failed to consider high-risk factors such as payments from crypto-related platforms.

What Happens Without One

Without a sound methodology, firms tend to apply controls uniformly — wasting resources in low-risk areas while leaving genuine exposures underserved. More acutely, they can't demonstrate to examiners, sponsor banks, or investors how compliance decisions were made.

For early-stage fintechs, crypto firms, and money transmitters, the gap usually isn't awareness of why the methodology matters. It's access to experienced compliance leadership who can build and own it.

Fraxtional's fractional BSA Officer and MLRO services place named, director-level compliance executives into client organizations for 3–9 month engagements. They take full accountability for methodology development, SAR workflows, and sponsor bank interactions — without the overhead of a permanent executive hire.

How the Financial Crime Risk Assessment Methodology Works

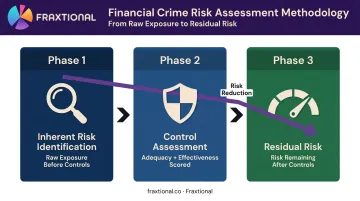

The methodology flows through three sequential phases. Each builds on the last.

Step 1: Identifying Inherent Risk

Inherent risk is the firm's raw exposure to financial crime before any controls exist. It's derived by examining the firm's activities across the four risk categories (covered below) and scoring each based on the nature and extent of exposure.

Common scoring approaches:

- Binary: Is this risk factor present or not?

- Quantitative: What percentage of customers or transactions involve this factor?

- Qualitative: What are the characteristics of the risk, even where precise data isn't available?

One critical principle: "unknown" is treated as highest risk. The absence of information is itself a risk signal, not a neutral baseline. Firms that can't accurately report on their customer base composition, transaction flows, or geographic exposure will produce unreliable inherent risk scores — regardless of how sophisticated the scoring model is.

Step 2: Assessing Controls

Once inherent risks are scored, the firm maps its existing controls against each risk and evaluates them on two dimensions:

| Dimension | Question |

|---|---|

| Adequacy | Is the control properly designed to address this risk? |

| Effectiveness | Is the control actually operating as intended? |

Both are typically scored as percentages. Combined, they produce a control efficacy figure for each risk area.

Common controls include:

- KYC, CDD, and EDD procedures

- Transaction monitoring

- Sanctions screening

- PEP and adverse media screening

- SAR filing processes

- Independent testing

Each control must be mapped to a specific risk. A policy document that lists controls without tying them to risk categories won't satisfy examiners or sponsor bank reviewers.

Step 3: Deriving Residual Risk

Residual risk is what remains after controls are applied. A few key rules govern this calculation:

- Residual risk is capped at the inherent risk level — controls can only reduce risk, not create new exposure

- A well-functioning control environment should produce meaningful reduction from the inherent risk score (for example, a high inherent score moving to medium residual after strong KYC and monitoring controls)

- Individual scores aggregate by category into a business-wide rating

- Customer, geographic, product, and transaction risk areas typically carry higher weighting per regulatory guidance

The gap between inherent and residual risk is what examiners, board members, and sponsor banks actually scrutinize. A narrow gap signals an underdeveloped control environment. A meaningful gap — backed by documented, tested controls — demonstrates that your compliance program is doing its job.

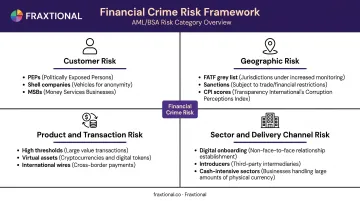

The Four Categories of Financial Crime Risk

While FATF, FFIEC, EBA, JMLSG, and the Wolfsberg Group use slightly different taxonomies, most converge on four primary categories. The depth of analysis within each should be proportionate to the firm's complexity.

Customer Risk

Customer risk reflects the likelihood that the firm's customers or beneficial owners are involved in or susceptible to financial crime.

High-risk customer types include:

- Politically Exposed Persons (PEPs) and their associates

- High-net-worth individuals with unclear source of wealth

- Shell companies or entities with opaque ownership structures

- Non-residents and cross-border customers

- Money services businesses, virtual asset service providers, and cash-intensive businesses

Red flags such as contradictory information at onboarding, prior SARs, or adverse media hits elevate customer risk regardless of their baseline risk score.

Data to capture: customer type by segment, percentage of high-risk customer types, beneficial ownership completeness rates, adverse media and SAR history.

Geographic Risk

Geographic risk operates in three directions, each requiring its own scoring approach:

- Operational geography — where the firm is licensed and operates

- Customer geography — where customers reside

- Transaction geography — where funds are sent or received

Key inputs for scoring include FATF's updated high-risk and grey-list jurisdictions (as of February 2026: DPRK, Iran, and Myanmar are subject to a call for action, with 22 jurisdictions under increased monitoring), the Transparency International Corruption Perceptions Index, national risk assessments, and sanctions designations.

Geographic risk scores must be updated whenever FATF or CPI data changes — not only during the annual review cycle.

Product and Transaction Risk

Products and transactions are scored based on their susceptibility to misuse.

High-risk indicators include:

- High or unlimited transaction thresholds

- Cash-intensive operations

- Non-face-to-face account origination

- International funds transfers and correspondent banking services

- Virtual asset transactions and VASP relationships

- Products used by or on behalf of unknown third parties

Transaction-level red flags — structured transactions, rapid in/out velocity, smurfing patterns, and incomplete originator or beneficiary data — should inform both the inherent risk assessment and transaction monitoring calibration. These patterns also signal where sector and delivery channel controls may need tightening.

Sector and Delivery Channel Risk

Sector risk covers the inherent vulnerability of industries the firm operates in or serves. Sectors with high government involvement, limited regulation, or endemic corruption carry elevated exposure.

Delivery channel risk turns on how accounts are opened and serviced:

- Face-to-face channels carry lower inherent risk due to direct identity verification

- Fully digital or intermediary-introduced channels carry higher risk

- Introducer or broker relationships require particular scrutiny, as the firm may have limited direct contact with the underlying customer

Key Factors and Common Mistakes in Applying the Methodology

Factors That Affect Methodology Quality

Data quality is the foundation. If a firm can't accurately report on its customer composition, transaction volumes, or geographic exposure, even a well-designed scoring model will produce unreliable output. Practical data to capture per category:

- Customer: segment breakdown, high-risk type percentages, beneficial ownership completeness

- Geographic: country distribution of customers and transaction flows, sanctions hit rates

- Product/Transaction: transaction type volumes, international wire percentages, virtual asset activity

- Delivery Channel: onboarding channel breakdown, introducer relationships

Business model velocity matters. Firms launching new products, entering new geographies, or scaling customer bases rapidly need to revisit the methodology more frequently than those with static models. The assessment must reflect the current business, not last year's.

Jurisdictional demands vary. Firms operating across the US, UK, and EU must ensure their methodology satisfies the most demanding applicable standard. What the FFIEC expects from a BSA Officer and what the FCA expects from an MLRO aren't identical — particularly around documentation depth and periodic review requirements.

Common Misconceptions and Mistakes

Treating the assessment as a static document. The JMLSG explicitly frames ML/TF risk assessment as dynamic. The FCA expects assessments to remain current. A stale risk assessment can be cited as a control deficiency in its own right — separate from the underlying risk it was meant to address.

Conflating inherent and residual risk. Presenting a single "risk rating" without demonstrating what controls reduced the raw exposure is a common examiner criticism. The methodology needs to show the full journey — not just the conclusion.

Over-relying on generic templates. This is especially common for crypto firms, BaaS arrangements, and cross-border payment services. Standard templates may not capture typology-specific risks like Travel Rule compliance gaps, VASP-to-VASP transaction flows, or embedded finance third-party risk chains.

The ADMISI 2023 FCA enforcement action shows what happens when template-based thinking meets non-negotiable risk indicators. The firm had no firm-wide financial crime risk assessment until July 2016. When it finally had one, the methodology allowed PEPs to be rated medium risk if they scored low on other factors — a structural flaw that let mandatory escalation triggers be offset rather than applied.

For firms that need to close a gap like this before an exam or investor review, Fraxtional's risk assessment engagements are scoped to the actual operating model — no generic templates, documentation tied to specific controls, and findings prioritized by severity with clear remediation steps. Most assessments complete in 2–4 weeks.

Frequently Asked Questions

What is a financial crime risk assessment?

A financial crime risk assessment is how a firm systematically identifies and documents its exposure to money laundering, fraud, terrorist financing, and sanctions violations. The output drives proportionate compliance controls and demonstrates a risk-based approach to regulators.

What are the five main steps of a risk assessment?

The core steps are:

- Identify risk categories relevant to the business

- Score inherent risk within each category

- Map and evaluate existing controls for adequacy and effectiveness

- Calculate residual risk

- Document findings and integrate outputs into the compliance program

Some frameworks consolidate these into three broader phases.

What are the four categories of financial crime risk?

Customer risk, geographic/country risk, product and transaction risk, and sector or delivery channel risk. These four categories are used across major frameworks including FATF, FFIEC, EBA, and the Wolfsberg Group, though the specific weighting and factor detail varies by jurisdiction and business model.

What is the difference between inherent risk and residual risk?

Inherent risk is a firm's raw exposure to financial crime before any controls are applied. Residual risk is what remains after accounting for the adequacy and effectiveness of those controls. The gap between the two demonstrates how much mitigation value the compliance program actually provides.

How often should a financial crime risk assessment be updated?

No universal frequency is prescribed, but reviews are expected whenever material changes occur, such as new products, geographies, customer segments, or regulatory shifts. Annual reviews are widely considered best practice, with higher-risk models typically requiring more frequent updates.

Who is responsible for conducting a financial crime risk assessment?

Responsibility sits with the designated AML compliance officer (the BSA Officer in the US, MLRO in the UK, or CAMLO in Canada), with oversight from senior management and the board. For firms without a full-time compliance officer, a fractional compliance leader can fulfill this function and serve as a named officer on regulatory filings.