Many firms already understand the concept of outsourcing. The harder question is whether it actually improves compliance outcomes — or simply moves the problem to a different address.

According to FinCEN's FY2024 Year in Review, U.S. financial institutions filed 4.7 million SARs in 2024, averaging nearly 12,900 per day. AML is not a periodic task. It's a continuous operational function that demands consistent capacity, expertise, and oversight.

This article breaks down the specific, measurable advantages AML outsourcing delivers in practice — and identifies where those advantages matter most.

Key Takeaways

- AML outsourcing spans transaction monitoring and KYC operations through fractional BSA Officers, CAMLOs, and MLROs

- The three core advantages — cost efficiency, specialized expertise, and operational scalability — each map to measurable compliance outcomes

- Under-resourced internal teams face higher error rates, regulatory exposure, and compounding costs over time

- Legal accountability stays with the institution regardless of outsourcing arrangement; governance oversight cannot be delegated

- Early-stage fintechs and crypto firms benefit most, though the priority advantage shifts by stage and risk profile

What Is AML Outsourcing?

AML outsourcing means engaging external providers to perform some or all anti-money laundering compliance functions on behalf of a financial institution. The scope can range from day-to-day operations to senior leadership — and most firms land somewhere in between.

On the operational side, outsourced functions typically include:

- Transaction monitoring alert review and disposition

- KYC/CDD onboarding and periodic reviews

- SAR drafting, review, and filing

- Case management and escalation workflows

At the leadership level, it extends to fractional compliance executives: experienced BSA Officers, CAMLOs, and MLROs who embed directly with the client team on a part-time or project basis.

Firms like Fraxtional operate across that full spectrum. Their fractional model places named compliance officers who take direct ownership of BSA/AML obligations — attending regulatory examinations, responding to sponsor bank inquiries, and managing SAR workflows. That's a different arrangement than hiring an outside consultant who advises from a distance.

AML outsourcing is a means to an outcome: consistent, defensible compliance. Cost reduction matters, but it isn't the point — and outsourcing is not a substitute for internal governance.

Key Advantages of AML Outsourcing Solutions

The advantages below focus on operational impact: cost, quality, risk, and scalability. These are the metrics compliance leaders and business executives actively track, and where outsourcing creates the clearest measurable difference.

Advantage 1: Cost Efficiency and Predictable Compliance Spending

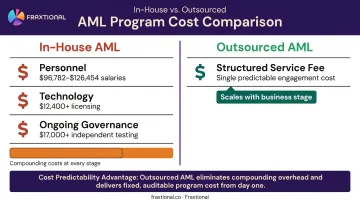

Building an AML program in-house requires simultaneous investment across three cost drivers:

- Personnel — CAMS-certified analysts, investigators, and a designated compliance officer

- Technology — KYC platforms, transaction monitoring systems, case management tools, and OFAC screening software

- Ongoing governance — independent testing, board reporting, policy updates, and training programs

These costs compound as the business grows. FinCEN's 2024 investment adviser AML/CFT rule estimates recurring compliance costs for covered advisers at approximately $17,000 per year for independent testing and $12,400 annually for specialized AML/CFT software licensing — and those are conservative baseline figures for smaller institutions.

Salary expectations add significantly more. Glassdoor data as of April 2025 puts the average U.S. AML Compliance Analyst at $96,782, with BSA Officers averaging $126,454 — figures that don't include benefits, onboarding, or replacement costs when staff leave.

Outsourcing converts these variable, often unpredictable internal expenses into structured service agreements with more transparent pricing. That shift matters most for:

- Seed-stage and Series A fintechs where full-time compliance headcount isn't yet justified

- Crypto firms facing new compliance obligations without established programs

- RIAs entering AML compliance for the first time under new FinCEN rules

- Institutions expanding into new product lines or jurisdictions that increase AML scope

The objective isn't to avoid investing in compliance. It's to align spending with actual risk volume and business stage rather than maintaining fixed overhead that's either underutilized or overwhelmed.

KPIs impacted: Total annual compliance spend, cost per SAR filed, technology licensing costs avoided, headcount cost versus service fee benchmarks

Advantage 2: Access to Specialized Expertise Across Regulations and Risk Types

Senior AML expertise is in short supply. The regulatory landscape — BSA, EU AML Directives, FATF, UK FCA requirements — has grown complex enough that generalist compliance experience isn't sufficient during regulatory exams or enforcement actions.

Crowe LLP's 2025 enforcement analysis puts numbers to this: in 2024 alone—

- 21 enforcement actions flagged concerns about AML team staffing

- 23 actions cited failures tied specifically to the BSA Officer role

- 28 of 42 enforcement actions identified deficiencies in suspicious activity monitoring systems

These weren't technology failures. Every one traces back to a gap in human expertise.

Regulators don't just evaluate whether compliance processes exist. They evaluate whether the people overseeing those processes demonstrate genuine expertise. Gaps in compliance leadership — particularly around SAR quality, risk assessments, and examiner interactions — are where regulatory findings most often originate.

Fraxtional, for example, places directors holding CAMS, CFE, CCA, and ACAMS FCI certifications across traditional finance, fintech, and digital assets. The team includes professionals with direct prior regulatory experience at the CFPB and U.S. Departments of Justice and Treasury — credentials that carry weight when an examiner is sitting across the table.

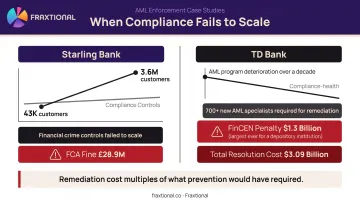

The Starling Bank case illustrates the cost of that gap. The FCA's final notice found that senior management lacked necessary AML skills and that the financial crime function was under-resourced and lacked key AML experience — a deficiency that contributed to a £28.9 million fine. A fractional director provides that depth of leadership without the hiring cycle, onboarding timeline, or retention risk of a full-time executive search.

KPIs impacted: Regulatory exam outcomes and findings, SAR filing accuracy, risk assessment quality, audit readiness, sponsor bank approval timelines

When this matters most: Regulatory examinations, sponsor bank due diligence, market expansion into new jurisdictions, and for crypto or embedded finance firms where general compliance experience is insufficient

Advantage 3: Scalability and Agility Without Proportional Headcount Growth

Internal AML teams scale one-for-one with headcount. As transaction volumes grow, new products launch, or new markets open, the institution must hire, train, and integrate additional staff. That process takes months — during which compliance coverage is thin and regulatory risk is elevated.

Juniper Research projects that spending on third-party AML systems will grow 121% by 2030, from $33.9 billion in 2025 to over $75 billion. That trajectory reflects a structural reality: the market is building capacity because internal-only programs can't scale fast enough.

Outsourced AML solutions are designed to adjust. Providers increase analyst capacity, expand monitoring coverage, and modify leadership involvement based on volume changes, new risk typologies, or regulatory updates — without the institution managing that scaling internally.

Fraxtional's engagement model reflects this directly. Clients can scale director involvement from advisory to fully embedded leadership, adjust weekly or monthly retainer scope, and access same-week onboarding when situations demand it. For crypto exchanges or fintechs hitting rapid growth phases, that speed matters.

Outsourced coverage also addresses continuity gaps that internal programs routinely struggle with:

- Staff attrition — When a BSA Officer leaves, outsourced providers don't create a vacancy

- Alert volume spikes — High transaction periods don't create backlogs when capacity scales with volume

- Regulatory changes — New requirements don't wait for hiring cycles to catch up

KPIs impacted: Time-to-compliance for new products or markets, alert backlog size and resolution rate, false positive rates, investigation turnaround time, staff turnover impact on compliance continuity

What Happens When AML Outsourcing Is Ignored or Delayed

The consequences of under-resourced internal AML programs follow a predictable pattern. Alert backlogs grow, investigation quality declines, and false positive rates — already reported at 95% or higher by many institutions according to LexisNexis Risk Solutions — consume whatever capacity the team has left. And when regulators arrive, the damage extends well beyond fines: licensing, sponsor bank relationships, and market access are all on the table.

Two recent cases illustrate the full cost of delayed action:

- Starling Bank grew from 43,000 customers in 2017 to 3.6 million by 2023 — but financial crime controls didn't keep pace. The FCA fined the bank £28.9 million for systemic failings in financial crime systems and controls.

- TD Bank let its AML program deteriorate for over a decade. The result: a $1.3 billion FinCEN penalty (the largest ever assessed against a depository institution), total resolution costs of approximately $3.09 billion, and a remediation program requiring 700+ new AML specialists.

In both cases, the cost of remediation after regulatory findings dwarfed what preventive investment would have required. The pattern is consistent: institutions wait until a finding forces their hand, then spend multiples of what a proactive program would have cost. Outsourcing works best when it's a strategic decision, not a crisis response.

How to Get the Most Value from AML Outsourcing

Outsourcing AML functions only delivers its full benefit when the institution maintains clear governance and active oversight. FinCEN, the OCC, and the EBA are consistent on this: legal accountability for AML obligations remains with the institution, regardless of whether execution is handled by a third party.

That accountability can't be outsourced. What can be outsourced is the execution capacity and expertise needed to fulfill it.

Three practices separate high-performing outsourced AML programs from arrangements that underdeliver:

- Measure outcomes, not activity. Track SARs filed, alerts resolved, risk assessments completed, and exam readiness. Hours logged tell you nothing about program health.

- Treat the provider as integrated, not external. Share business strategy, product changes, and risk appetite so the outsourced team can give proactive guidance rather than just processing cases reactively.

- Set review cadences before the engagement begins. Regular outcome reviews create accountability and surface issues before regulators do.

These practices work best when the provider is structured to support them from day one. Fraxtional's director-led model is built around this. Named compliance officers take full personal accountability for BSA/AML programs, representing clients before regulators, auditors, and sponsor banks, while clients retain governance oversight at the board level. Comprehensive documentation, SAR escalation workflows, and board reporting are part of every engagement by default.

Conclusion

The advantages of AML outsourcing — faster exam outcomes, specialized expertise, and operational scalability — compound over time and translate into measurable outcomes: cleaner exam results, faster time-to-compliance for new products, more accurate SAR filings, and compliance programs that hold up under scrutiny.

Those advantages are clearest for institutions that engage the right partners early, maintain active oversight, and review outcomes against defined metrics. Outsourcing triggered by regulatory findings costs more and delivers less than outsourcing built into the compliance strategy from the start.

That shift is already underway. Fintechs, crypto firms, and financial institutions that need credentialed AML compliance leadership — without the cost or lag of a full-time hire — are choosing experienced, director-led providers as the practical starting point for building programs that regulators and investors take seriously.

Frequently Asked Questions

Can you outsource AML compliance?

Yes. AML functions — including transaction monitoring, KYC/CDD, SAR filing, and compliance leadership roles like BSA Officers and MLROs — can be outsourced to qualified third-party providers. Legal accountability for AML obligations remains with the institution regardless, so active governance and oversight of the provider remain regulatory requirements, not optional practices.

What are the 4 pillars of AML?

Per the FFIEC BSA/AML Examination Manual, the four pillars are: a designated BSA compliance officer, a system of internal controls, independent testing, and training for appropriate personnel. Outsourced AML solutions can directly support or deliver all four, particularly for institutions that lack in-house capacity to sustain them independently.

What is the difference between AML outsourcing and hiring a fractional BSA Officer?

AML outsourcing is a broad category covering everything from operational managed services to compliance leadership roles. A fractional BSA Officer is a specific model within that spectrum: a senior compliance executive engaged on a part-time or project basis, providing director-level oversight without the full-time salary and benefits cost.

Who is legally responsible if an outsourced AML provider makes a compliance error?

The financial institution remains legally liable for any breach of AML obligations, even when those functions are performed by an external provider. Selecting credentialed providers, maintaining active oversight, and documenting the outsourcing arrangement clearly are all regulatory requirements.

How much does AML outsourcing cost compared to building in-house?

In-house programs require simultaneous investment in personnel (BSA Officers average $126,454 annually), technology, independent testing, and ongoing governance. Outsourcing converts these into structured service fees that scale with business needs. For early-stage and growth-stage firms, the cost comparison consistently favors outsourcing.

What types of companies benefit most from AML outsourcing solutions?

AML outsourcing delivers the clearest value for:

- Early-stage fintechs and crypto firms building compliance programs from scratch

- Growth-stage companies scaling AML coverage without adding proportional headcount

- Institutions entering new markets that require specialized regulatory expertise they don't yet have in-house