Introduction

According to the UNODC, between $800 billion and $2 trillion is laundered globally each year — roughly 2% to 5% of global GDP. Most of it goes undetected.

The cost of missing AML red flags is no longer abstract. In October 2024, FinCEN assessed a record $1.3 billion penalty against TD Bank for willful BSA violations — the largest ever against a US depository institution. That same year, the FCA fined Starling Bank £28,959,426 for failures in financial crime systems and controls, including sanctions screening.

For compliance teams, the challenge isn't awareness — it's catching the signals before they compound into enforcement action.

This article covers the top 10 AML red flags across client behavior, transactions, identity, geography, and virtual assets. It explains why each matters, how it applies across the US, UK, and Canada, and what your team should do when one surfaces.

Key Takeaways

- AML red flags are behavioral, transactional, or identity-based warning signs that a customer or transaction may be linked to money laundering or terrorist financing.

- No single red flag confirms criminal activity — SAR or STR filing decisions turn on the combined weight of indicators, context, and facts.

- The top 10 indicators cover identity and ownership red flags, transaction anomalies, geographic risk, PEP and sanctions exposure, adverse media, and virtual asset activity.

- Each indicator maps to KYC, CDD, EDD, or transaction monitoring controls — where detection must happen before suspicious activity escalates.

What Is an AML Red Flag?

An AML red flag is a potential indicator — rooted in client behavior, transaction patterns, or contextual factors — that something is unusual and warrants further review. A red flag alone is not proof of money laundering. It signals that a deeper assessment is needed before proceeding.

FATF's guidance organizes red flag indicators into several broad categories. For virtual assets specifically, FATF's 2020 red flag report identifies six:

- Transaction indicators

- Transaction patterns

- Anonymity

- Sender/recipient characteristics

- Source of funds or wealth

- Geographic risk

FINTRAC describes ML/TF indicators as potential red flags that "may initiate suspicion or indicate that something is unusual without a reasonable explanation."

The 10 indicators below are drawn from FATF guidance, FINTRAC in Canada, the FFIEC BSA/AML Manual in the US, and FCA expectations in the UK, making them applicable across all three jurisdictions.

The Top 10 AML Red Flags and Indicators

Red Flag #1: Overly Secretive Clients Who Refuse to Provide Information

Clients who are evasive about their identity, the purpose of a transaction, the source of funds, or the identity of beneficial owners trigger mandatory CDD review under both FATF and FINTRAC guidance. KYC requirements exist precisely to surface this behavior at onboarding.

Specific behaviors to watch for:

- Refusing to complete identity verification

- Providing vague or inconsistent answers about business purpose

- Altering or canceling a transaction after being asked for identification

- Displaying hostility or nervousness when questioned about standard compliance requirements

- Insisting on using an intermediary to avoid direct contact

Red Flag #2: Suspicious or Inconsistent Personal Information

Inconsistencies in identity documents are strong indicators that a client may be attempting to conceal their true identity. FATF and Egmont guidance identifies false names, fraudulent identification, and customers whose information does not align with their stated activity as behavioral red flags.

Watch for:

- Mismatched names, addresses, or dates of birth across documents

- Use of aliases or multiple identities

- Documents that appear altered, expired, or unverifiable

- A stated address that is inconsistent with the customer's described business activity

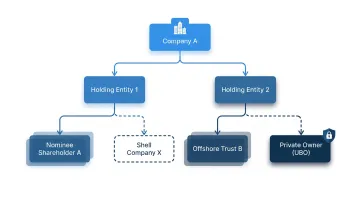

Red Flag #3: Unclear or Opaque Beneficial Ownership (UBO)

Using complex ownership structures (shell companies, nominee arrangements, layered holding entities) to obscure who ultimately owns or controls a business is one of the most documented money laundering techniques. FATF's 2023 beneficial ownership guidance identifies these structures as mechanisms launderers use to conceal true control.

Under FinCEN's CDD Final Rule, covered financial institutions must identify and verify beneficial owners of legal entity customers, including individuals owning 25% or more and one designated control person. When a beneficial owner cannot be clearly identified, Enhanced Due Diligence (EDD) is required.

Red Flag #4: Questionable or Unexplained Source of Funds

Funds arriving without a credible economic explanation are a major concern regardless of the amount. This red flag applies across all sectors and jurisdictions.

Common examples:

- Third-party funding with no apparent connection to the client

- Large cash deposits lacking a plausible income source

- Funds originating from high-risk jurisdictions with no documented business relationship

- Wire transfers from unrelated entities with no supporting documentation

FATF's virtual asset red flag guidance flags source-of-funds inconsistencies as a high-risk indicator — particularly when the stated source of wealth doesn't match the client's profile or transaction behavior.

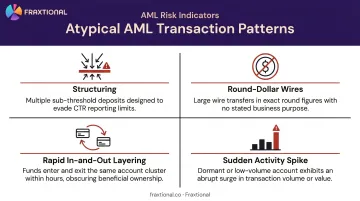

Red Flag #5: Atypical Transaction Patterns

Structuring (breaking large transactions into smaller amounts to stay below reporting thresholds) is explicitly prohibited under 31 U.S.C. § 5324. The US Currency Transaction Report (CTR) threshold is over $10,000, and FFIEC Appendix G clarifies that structuring can occur even when no single transaction crosses that threshold at any one institution on any single day.

Other atypical patterns to flag:

- Round-dollar wire transfers with no stated purpose

- Rapid in-and-out movement of funds (same-day or next-day layering)

- Sudden spikes in account activity inconsistent with the customer's established profile

- Transactions with no apparent business rationale

Automated transaction monitoring systems detect these patterns, but the SAR decision hinges on whether a reasonable explanation exists — not the pattern alone.

Red Flag #6: Geographic Inconsistencies and High-Risk Jurisdictions

Transactions involving FATF-identified high-risk jurisdictions, countries with weak AML enforcement, or regions with known sanctions exposure require heightened scrutiny. FATF publishes its black and grey lists three times per year; treat them as live references updated each Plenary cycle.

Geographic risk also applies when a customer's location makes no logical sense relative to their chosen financial institution. A retail client in a high-risk country routing funds through a small US community bank with no apparent connection to that jurisdiction is a textbook example.

Red Flag #7: Politically Exposed Persons (PEPs) and Their Associates

A PEP is any individual who holds or has held a prominent public function: heads of state, senior politicians, military officers, judges, or executives of state-owned enterprises. That access to public funds creates elevated corruption and money laundering risk regardless of jurisdiction.

FATF Recommendation 12 requires financial institutions to:

- Apply risk management systems to identify PEP relationships

- Obtain senior management approval before establishing PEP relationships

- Conduct source-of-wealth and source-of-funds verification

- Apply enhanced ongoing monitoring

PEP risk extends to immediate family members and close associates (RCAs). Enhanced measures are mandatory for foreign PEPs; for domestic PEPs and international organization PEPs, FATF requires a risk-based assessment with enhanced measures where warranted.

Red Flag #8: Presence on Sanctions Lists

Firms must screen customers against global sanctions lists at onboarding — and continuously thereafter, because designations change. A customer clean at onboarding can be added to a sanctions list weeks later.

| Jurisdiction | Primary Sanctions List |

|---|---|

| United States | OFAC SDN and Consolidated Lists |

| United Nations | UN Security Council Consolidated List |

| United Kingdom | UK Sanctions List |

| European Union | EU Consolidated Financial Sanctions List |

Failure to catch a sanctioned counterparty carries some of the harshest penalties in financial compliance. OFAC's 2023 settlement with Binance totaled $968,618,825 — largely for sanctions violations through inadequate screening on a virtual asset platform.

Red Flag #9: Adverse Media Coverage

Negative news linking a client to financial crime, fraud, corruption, or organized crime constitutes an AML red flag under CDD and EDD frameworks. The FCA's 2025 CDD review treats adverse media screening as a core component of customer due diligence. FATF/Egmont guidance notes that media reporting can help identify potential corruption and higher-risk beneficial ownership situations.

Adverse media screening must cover:

- Traditional news sources and financial press

- Law enforcement reports and court records

- International organization databases

- Non-English language sources across multiple regions

Minimal online presence is not inherently suspicious. Undiscovered fraud allegations in a foreign-language publication, on the other hand, represent a clear screening failure that regulators will find before you do.

Red Flag #10: Unmonitored Virtual Asset Activity

Crypto transactions are not inherently suspicious. Specific behaviors are.

FATF's virtual asset red flag indicators include:

- Use of mixing or tumbling services to obscure transaction origin

- Transactions using privacy coins or anonymity-enhanced cryptocurrencies

- Structuring crypto transactions below reporting or recordkeeping thresholds

- Using exchanges or VASPs in high-risk jurisdictions without adequate KYC

- Repeatedly exchanging fiat to crypto without clear purpose

The Travel Rule — FATF Recommendation 16, updated at the June 2025 FATF Plenary — governs information-sharing obligations for virtual asset transfers above threshold. FINTRAC's Travel Rule obligations apply to Canadian reporting entities, and FinCEN's proposed rulemaking extends similar requirements to US VASPs.

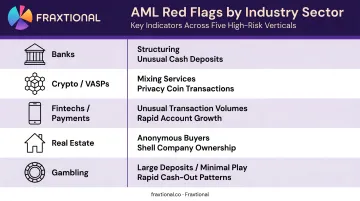

How AML Red Flags Vary by Industry and Jurisdiction

The same transaction behavior can be routine in one industry and a clear warning sign in another. Context is what separates a legitimate pattern from a suspicious one — which is why sector-specific red flag typologies matter alongside universal indicators.

| Sector | Key Red Flags |

|---|---|

| Banks | Structuring, placement patterns, cash-intensive deposits |

| Crypto / VASPs | Mixing services, privacy coins, unhosted wallet activity |

| Fintechs / Payments | Unusual transaction volumes, onboarding anomalies, rapid account growth |

| Real Estate | Anonymous buyers, shell company purchases, all-cash transactions |

| Gambling | Large deposits with minimal play followed by cash-outs |

Sector-specific patterns also intersect with where your firm operates. The underlying red flag categories may be consistent globally, but your reporting obligation — when and to whom you file — depends entirely on jurisdiction.

Reporting Obligations by Jurisdiction

- US: File a SAR with FinCEN under BSA rules (standard: "knows, suspects, or has reason to suspect")

- Canada: File an STR with FINTRAC under PCMLTFA (standard: "reasonable grounds to suspect")

- UK: Submit a SAR to the National Crime Agency under the Proceeds of Crime Act 2002

Firms operating cross-border must satisfy all applicable regimes simultaneously. A single transaction involving a US fintech with Canadian customers and a UK banking partner can trigger obligations in all three jurisdictions.

No single red flag automatically triggers a filing obligation. The decision turns on the full picture — the combination of facts, customer context, transaction history, and indicators that together meet the applicable suspicion threshold in your jurisdiction.

What to Do When You Spot an AML Red Flag

The Four-Step Response

- Flag — Document the red flag immediately and open an internal review case

- Investigate — Review transaction history, gather contextual facts, and assess whether a reasonable explanation exists

- Report — File a SAR (US/UK) or STR (Canada) with the relevant authority if reasonable grounds to suspect ML/TF are established

- Remediate — Strengthen controls to reduce the likelihood of recurrence

Critical: Tipping off the subject of a SAR or STR is prohibited in all three jurisdictions. In the US under 31 U.S.C. § 5318(g)(2), in Canada under PCMLTFA section 8, and in the UK under POCA 2002 section 333A.

Building the Infrastructure to Catch Red Flags

Effective detection requires layered controls, not just a checklist:

- KYC/CDD at onboarding — identity verification, risk classification, beneficial ownership collection

- Automated transaction monitoring — calibrated thresholds and alerts scaled to your transaction volume

- EDD protocols — triggered by PEP status, high-risk jurisdiction connections, or accumulation of multiple flags

- Regular staff training — human judgment must complement automated alerts, not replace them

Where Fractional Compliance Leadership Fits

For early-stage fintechs, crypto firms, and payment companies, building this infrastructure from scratch is often the hardest part. Hiring a full-time BSA Officer, MLRO, or CAMLO is expensive (typically $25,000+ per month for a senior executive) — and unnecessary at early stages.

Fraxtional's fractional compliance model gives growing firms direct access to director-level AML expertise without the full-time cost. That includes designing red flag detection frameworks, building SAR/STR filing workflows, calibrating transaction monitoring rules, implementing PEP and OFAC screening, and preparing for regulatory examinations.

The named BSA Officer, MLRO, or CAMLO role is recognized by regulators and sponsor banks — with full use of name and title for regulatory filings.

Detecting AML red flags is only as effective as the compliance program behind it. A well-built program doesn't just catch suspicious activity — it keeps your sponsor bank relationships intact and your operating license off the regulator's radar.

Frequently Asked Questions

What are the five red flags in AML?

Five of the most commonly cited AML red flags are: secretive or evasive clients, questionable source of funds, atypical transaction patterns (including structuring), geographic risk from high-risk jurisdictions, and PEP or sanctions exposure. These categories appear consistently across FATF guidance, FINTRAC indicators, and FFIEC BSA/AML examination standards.

What are the 10 red flag symptoms of money laundering?

The 10 indicators covered in this article are: overly secretive clients, suspicious or inconsistent personal information, opaque beneficial ownership, unexplained source of funds, atypical transaction patterns, geographic inconsistencies, PEP exposure, presence on sanctions lists, adverse media coverage, and unmonitored virtual asset activity. No single indicator is conclusive — context determines the response.

Is one AML red flag enough to file a Suspicious Activity Report (SAR)?

No. A single anomaly warrants investigation, not an automatic report. US, Canadian, and UK regulators require a combination of facts, context, and indicators — "knows, suspects, or has reason to suspect" under FinCEN rules, and "reasonable grounds to suspect" under FINTRAC — before a SAR or STR must be filed.

How do AML red flags vary by industry?

The core categories apply universally, but specific indicators differ by sector. Structuring is a primary concern in banking; mixing services and privacy coins are crypto red flags; unusual onboarding velocity is a fintech indicator; and large deposits followed by minimal play and a cash-out request are characteristic of gambling sector typologies.

What is the difference between CDD and EDD when responding to red flags?

CDD is the standard identity verification and risk classification applied to all customers at onboarding. EDD is a deeper, ongoing review triggered by elevated risk factors — PEP status, high-risk jurisdiction connections, or multiple red flags — requiring additional source of funds verification and more frequent monitoring.

How can fintechs and startups build an effective AML red flag detection process?

Four foundations matter most: automated transaction monitoring, a documented KYC/CDD framework, a SAR/STR filing procedure, and regular staff training. Many early-stage firms cover the expertise gap through fractional compliance models — a fractional BSA Officer or CAMLO — rather than a full-time executive hire before scale justifies it.