Introduction

According to the UNODC, an estimated $800 billion to $2 trillion moves through illicit channels globally each year — roughly 2% to 5% of global GDP. That money doesn't disappear into a vacuum. It flows through banks, money services businesses, crypto exchanges, and fintech platforms, often hiding in plain sight.

For any company operating within the U.S. financial system, understanding FinCEN isn't optional. The compliance gaps that routinely sink early-stage companies include:

- Missed SAR filings that trigger regulatory scrutiny

- Weak KYC programs that expose the business to enforcement action

- Undocumented AML frameworks that fracture banking relationships

Each gap, on its own, can invite investigations, civil penalties, or a severed sponsor bank partnership.

What follows is a practical breakdown of FinCEN's purpose, its legal authority, and what compliance actually demands from financial institutions operating in the U.S. today.

Key Takeaways

- FinCEN is a U.S. Treasury bureau established in 1990 to protect the financial system from money laundering, terrorist financing, and related crimes

- Its authority flows from the Bank Secrecy Act, the USA PATRIOT Act, and the Anti-Money Laundering Act of 2020

- Financial institutions must maintain KYC/CDD programs, file SARs and CTRs, and operate structured AML programs — or face serious penalties

- FinCEN operates within a global network of 182 FIUs (Egmont Group), with direct counterparts including Canada's FINTRAC and the UK's NCA/FCA

What Is FinCEN and Is It a Real Government Agency?

Yes — FinCEN is a fully official bureau of the U.S. Department of the Treasury, not a private body or advisory organization.

Its legal foundation developed in three steps:

- 1990: Established under Treasury Order 105-08 on April 25, 1990

- 2001: Section 361 of the USA PATRIOT Act formally defined its duties and powers

- 2002: Treasury Order 180-01 (September 26) re-established it as an official bureau under 31 U.S.C. 310

Where FinCEN Sits in Government

FinCEN's Director reports directly to the Treasury Under Secretary for Terrorism and Financial Intelligence. Andrea Gacki was appointed Director on July 13, 2023. She leads a bureau that sits at the intersection of national security and financial regulation.

What FinCEN Does Not Do

FinCEN does not make arrests, prosecute cases, or conduct field investigations. Its role is to collect, analyze, and disseminate financial intelligence. It works with three primary constituencies:

- Law enforcement agencies (FBI, IRS Criminal Investigation, Homeland Security Investigations, and 432 other federal, state, and local agencies)

- Regulators who supervise financial institutions

- The financial services industry, which is required to report suspicious and high-value transactions

Enforcement authority — arrests, prosecutions, asset seizures — stays with those partner agencies. FinCEN's power lies in the intelligence it generates and shares.

What Does FinCEN Actually Do?

Collecting and Analyzing Financial Intelligence

FinCEN is the U.S. Financial Intelligence Unit (FIU). Its core function is receiving mandatory reports from financial institutions (primarily Currency Transaction Reports (CTRs) and Suspicious Activity Reports (SARs)) and analyzing them to identify patterns of money laundering, terrorist financing, and other financial crime.

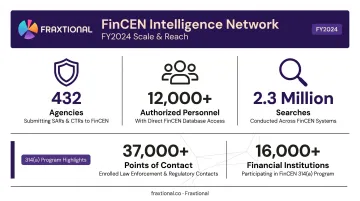

In FY2024, 432 federal, state, and local agencies had access to BSA data, with over 12,000 authorized personnel running more than 2.3 million searches.

FinCEN's 314(a) program, operating under the USA PATRIOT Act, allows law enforcement to simultaneously query financial accounts across more than 37,000 points of contact at over 16,000 financial institutions. As of May 2026, FinCEN had processed 8,976 total 314(a) requests — 936 related to terrorism financing and 8,040 related to money laundering.

A concrete example: in December 2025, FinCEN announced a data-driven border operation targeting more than 100 U.S. money services businesses along the southwest border. The operation resulted in six notices of investigation, over 50 compliance outreach letters, and dozens of IRS examination referrals.

That intelligence-gathering capacity doesn't exist in isolation — it directly shapes how FinCEN writes and enforces the rules that financial institutions must follow.

Setting and Enforcing AML Regulations

FinCEN writes and enforces the AML/CFT regulatory framework. It creates binding rules under the BSA requiring banks, fintechs, money services businesses, mutual funds, and others to maintain AML programs and file required reports.

Violations carry real consequences:

- Notices of investigation

- IRS examination referrals

- Civil money penalties

- Civil injunctive actions

- Criminal referrals for willful violations

FinCEN treats non-compliance as a national security risk, not an administrative oversight.

Sharing Intelligence Domestically and Internationally

FinCEN serves as the U.S. representative in the Egmont Group, an international network of 182 Financial Intelligence Units. This membership allows FinCEN to trace transnational financial crime networks — including drug trafficking, terrorism financing, and sanctions evasion — across borders.

On the domestic side, BSA data flows directly to IRS Criminal Investigation, the FBI, Homeland Security Investigations, and hundreds of other agencies actively working financial crime cases.

The Laws That Give FinCEN Its Authority

FinCEN's power isn't self-generated. It derives from specific statutes passed by Congress. Each law defines real compliance obligations for financial institutions.

The Bank Secrecy Act (BSA)

The BSA (1970), formally the Currency and Foreign Transactions Reporting Act, is the foundation of U.S. AML compliance. Codified at 31 U.S.C. 5311 et seq., it requires financial institutions to:

- Maintain records of cash purchases of monetary instruments

- File CTRs for currency transactions exceeding $10,000 (within 15 days)

- File SARs for activity suggesting money laundering, tax evasion, or financial crime

FinCEN administers and enforces the BSA.

The USA PATRIOT Act

The 2001 PATRIOT Act significantly expanded FinCEN's authority. Title III — the International Money Laundering Abatement and Anti-Terrorist Financing Act — formally established FinCEN's bureau status and created requirements for:

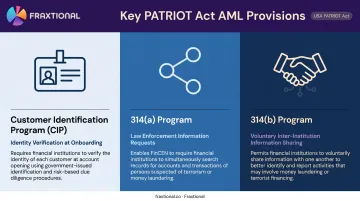

- Customer Identification Programs (CIP) at financial institutions

- The 314(a) program enabling law enforcement to query financial institutions simultaneously

- The 314(b) program allowing voluntary information sharing between financial institutions

The AML Act of 2020 and the Corporate Transparency Act

The Anti-Money Laundering Act of 2020, enacted as part of the National Defense Authorization Act (Public Law 116-283), modernized the AML framework after decades without major updates.

Its most significant provision: the Corporate Transparency Act (CTA), which requires certain business entities to report Beneficial Ownership Information (BOI) to FinCEN: names, addresses, dates of birth, and ID numbers of individuals who ultimately own or control a company.

Important caveat: The BOI landscape shifted in 2025. FinCEN's March 21, 2025 release removed BOI reporting requirements for U.S. companies and U.S. persons.

Foreign reporting companies remain subject to narrowed deadlines unless exempt, and 23 categories of entities are exempt entirely. Treat CTA obligations as legally evolving — verify current requirements before acting.

What FinCEN Compliance Requires from Financial Institutions

Whether you're a bank, fintech, crypto exchange, or money transmitter, these are legal obligations with real penalties for failure.

KYC and Customer Due Diligence

Know Your Customer (KYC) and Customer Due Diligence (CDD) form the foundation of any FinCEN-compliant program.

- KYC verifies a customer's identity before they access financial services

- CDD goes further: confirm that personal information matches the account controller, then monitor that relationship over time

- Enhanced Due Diligence (EDD) applies to higher-risk customers — including Politically Exposed Persons (PEPs) and sanctions-flagged individuals — requiring deeper review of source of funds and business relationships

FinCEN's CDD final rule, published in May 2016 and effective from May 2018, added explicit CDD and ongoing monitoring requirements for covered financial institutions.

Filing SARs and CTRs

Two core reporting obligations:

| Report | Trigger | Deadline |

|---|---|---|

| SAR | Suspected money laundering, fraud, or financial crime | 30 calendar days after initial detection (extendable to 60 days if no suspect identified) |

| CTR | Any cash transaction exceeding $10,000 in a single business day | 15 days after the transaction |

These filings are how financial institutions actively feed intelligence into FinCEN's surveillance network. Failure to file — or filing incorrectly — is itself a violation.

Building a Complete AML Compliance Program

FinCEN doesn't just expect individual filings. It expects a structured, written program. The four regulatory pillars for banks under 31 CFR 1020.210 are:

- Internal controls — written policies and procedures

- Independent testing — third-party or internal audit of the program

- Designated compliance officer — a named BSA Officer with real ownership

- Ongoing employee training — not just onboarding, but regular updates

A fifth pillar — CDD — was added through FinCEN's 2016 final rule.

For early-stage fintechs, crypto firms, and money transmitters building these programs from scratch, the hardest part is often standing up this structure without a dedicated compliance team in place.

Fractional compliance leadership addresses that gap directly. Fraxtional, for example, places named BSA Officers and CCOs — Directors who own daily monitoring, SAR/CTR workflows, and regulatory inquiries — without the cost of a full-time hire. Their team includes ACAMS-certified professionals with examination experience across OCC, FDIC, and NCUA supervised institutions, and Directors who have held BSA Officer roles at fintechs, crypto firms, and community banks.

FinCEN and Its Global Counterparts

FinCEN is U.S.-specific, but the AML/CFT framework it enforces is part of a coordinated global architecture. Companies operating cross-border need to understand both FinCEN and the equivalent bodies in their jurisdictions.

| Jurisdiction | Regulatory Body | Primary Function |

|---|---|---|

| United States | FinCEN | FIU, BSA/AML regulation enforcement |

| Canada | FINTRAC | FIU, AML/ATF compliance supervision |

| United Kingdom | NCA (UKFIU) | Receives and analyzes SARs |

| United Kingdom | FCA | AML compliance regulation for financial firms |

| International | FATF | Standard-setter, 40 member jurisdictions |

The Financial Action Task Force (FATF) underpins all of the above. Its 40 Recommendations define the baseline for AML/CFT compliance across member countries including the U.S., UK, Canada, and EU member states.

For companies with cross-border operations, the compliance obligations don't stop at FinCEN. Fraxtional places fractional compliance leaders — including MLROs for the UK, CAMLOs for Canada, and CCOs for EU-facing operations — giving multi-jurisdiction firms a named, accountable compliance officer in each regulatory environment without separate full-time hires.

Frequently Asked Questions

What is the purpose of FinCEN?

FinCEN's purpose is to protect the U.S. financial system from illicit activity. It collects and analyzes financial data from institutions, enforces AML/CFT regulations under the BSA, and shares intelligence with domestic law enforcement and international FIU partners to counter money laundering and terrorist financing.

Is FinCEN a real government agency?

Yes. FinCEN is an official bureau of the U.S. Department of the Treasury, established by Treasury Order 105-08 on April 25, 1990, and re-established as a bureau on September 26, 2002. Congress granted its authority through statutes including the Bank Secrecy Act and the USA PATRIOT Act.

What is the UK equivalent of FinCEN?

The UK has no direct equivalent. The National Crime Agency's UK Financial Intelligence Unit (UKFIU) receives and analyzes Suspicious Activity Reports, while the FCA regulates AML compliance obligations for financial firms. Canada's direct equivalent is FINTRAC.

What is the difference between FinCEN and OFAC?

Both are U.S. Treasury bureaus, but with distinct mandates. FinCEN enforces AML/CFT laws and collects financial intelligence under the BSA. OFAC administers and enforces economic and trade sanctions, maintaining lists of sanctioned individuals, entities, and countries. Sanctions screening and AML compliance are related but separate obligations.

Who must comply with FinCEN regulations?

Compliance obligations apply to any entity defined as a "financial institution" under the BSA — including banks, credit unions, money services businesses, broker-dealers, fintech companies, and crypto exchanges. Certain business entities also have obligations under the Corporate Transparency Act, though U.S. domestic reporting requirements were narrowed in 2025.

What are the penalties for non-compliance with FinCEN?

Penalties include civil money penalties, notices of investigation, IRS examination referrals, civil injunctive actions, and criminal referrals for willful violations. Beyond formal penalties, compliance failures can cost early-stage financial companies their banking relationships and investor confidence — consequences that can end a business outright.